US Opening News: USD gains whilst Kiwi slips post-RBNZ, XAU passes USD 4,000 ahead of FOMC Minutes

08 Oct 2025, 11:40 by Newsquawk Desk

- EU sees new US trade demands hollowing out deal struck by US President Trump, according to Bloomberg citing sources.

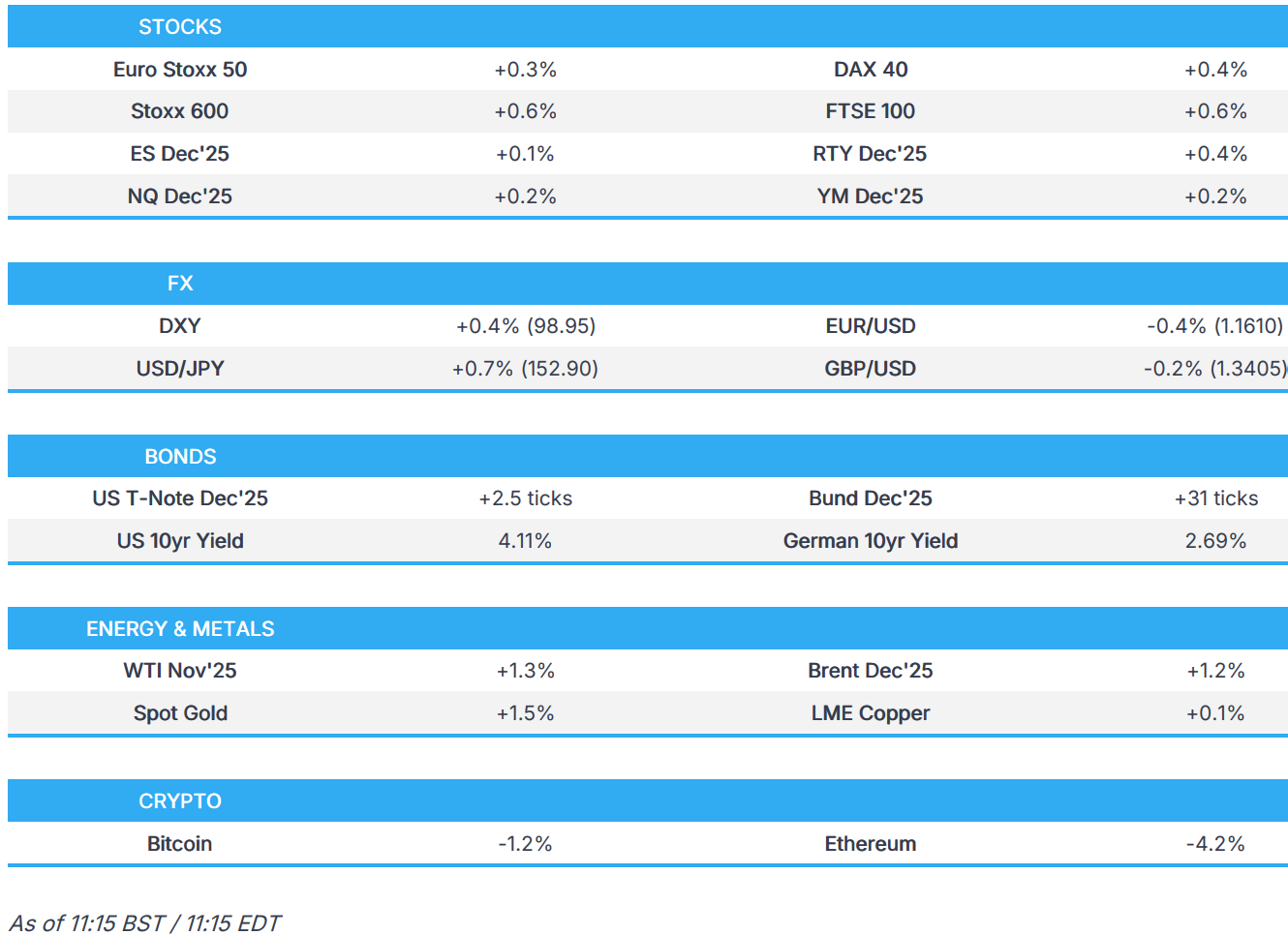

- European bourses are broadly firmer but with ASML (-1.7%) weighing on the AEX; US equity futures are modestly higher.

- USD continues to rally, boosted by a weak JPY and NZD; the Kiwi is the clear underperformer after the RBNZ delivered a jumbo 50bps cut and left the door open for more rate reductions.

- Global paper moves higher, OATs outperform, awaiting French PM Lecornu later.

- XAU topped the USD 4,000/oz mark, crude is continuing to rebound as China is set to re-enter the market tomorrow.

- Looking ahead, NBP Policy Announcements, FOMC Minutes (Sep), Speakers including BoE’s Pill, ECB’s Elderson & Lagarde, Fed’s Musalem, Barr, Goolsbee & Kashkari, NVIDIA CEO Huang, French PM Lecornu, Supply from US.

TARIFFS/TRADE

- EU sees new US trade demands hollowing out deal struck by US President Trump, according to Bloomberg citing sources. Earlier in the month, Trump admin reportedly sent the EU a fresh proposal for implementing “reciprocal, fair and balanced” trade.

EUROPEAN TRADE

EQUITIES

- European bourses (STOXX 600 +0.6%) have opened largely firmer (FTSE 100 +0.3%, CAC 40 +0.6%, DAX 40 +0.2% and Euro Stoxx +0.3%), with the only downside being the AEX (-0.39%), largely due to pressure in ASML (-2.5%). A combination of recent reporting suggesting financial pressure on Oracle in the previous session and after the US House committee called for broader bans on its chips to China.

- European sectors have opened mostly in the green. The biggest winner is Basic Resources (+1.0%), following broker upgrades for some of the biggest companies in the industry like Rio Tinto (+0.9%), Anglo American (+1.7%) and Antofagasta (+2.5%), driving up their share prices and therefore lifting the basic resource sector. Eyes also on gold miners after the yellow metal topped USD 4,000/oz to the upside. Autos is towards the foot of the pile, pressured by losses in BMW (-4.5%) after it cut 2025 guidance.

- US futures are slightly firmer (ES +0.1% NQ +0.2% RTY +0.4%). Futures are in a holding pattern after stocks were sold on Tuesday following reports via The Information that internal data shows the financial challenge of renting out NVIDIA (NVDA) chips and its impact on margins.

- Click for the sessions European pre-market equity newsflow

- Click for the additional news

- Click for a detailed summary

FX

- DXY is up for a third session in a row with WTD gains thus far of 1.1%. It remains the case that the price action is not being driven by outright bullish calls on the USD but more a case of weakness elsewhere, mainly JPY and EUR, with NZD the latest of its major counterparts to take a stumble. If anything, the macro narrative surrounding the US remains a downbeat one as the government shutdown continues to drag on, delaying economic data releases and threatening a hit to domestic growth. DXY has ventured as high as 98.97 with focus on a test of the 99.0 mark; not breached since 5th August.

- EUR remains pressured vs. the USD and is just about holding onto a 1.16 handle after delving as low as 1.1607. French political turmoil remains a key part of the Eurozone macro narrative with PM Lecornu (also due to speak @ 19:00BST) set to meet with socialists, greens and communists in an attempt to form a coalition government. The likely price for Macron will be a left-wing PM, which could make the parliamentary arithmetic easier for passing a budget, given that the Socialist Party holds the most seats in the National Assembly. Aside from France, Germany saw further woeful data earlier in the session with German Industrial Orders falling well short of consensus and subsequently stoking concerns over a contraction in the domestic economy. In terms of price action, if 1.16 gives way in EUR/USD the next target comes via the 27th August low at 1.1573.

- JPY remains very much on the backfoot against the USD with USD/JPY having risen five handles since Takaichi's victory in the LDP leadership race. The move has been relentless this week given the market's view that the fallout of Takaichi will leader to a mix of looser monetary and fiscal policy. Subsequently, markets only assign a circa 25% chance of a cut this month vs. roughly 70% last week. Further reason for caution in expecting additional tightening from the BoJ was presented overnight via the August real cash earnings data, which printed a deeper-than-expected contraction. USD/JPY has climbed as high as 152.96 with focus now on a test of 153; not breached since February. If the pair begins to approach 155, given the velocity of the move, expectations of potential intervention will likely increase.

- GBP is a touch weaker vs. the USD but stronger vs. the EUR. At the risk of sounding like a broken record, in the absence of any tier 1 UK data, the macro narrative has failed to evolve beyond ongoing angst ahead of the November 26th Budget. BoE Chief Economist Pill is due to give remarks at 16:00BST. GBP/USD briefly tripped below Tuesday's low at 1.3391 before returning to a 1.34 handle.

- NZD is the laggard across the majors after the RBNZ's decision to opt for a deeper 50bps rate cut (views heading into the meeting were split between 25bps and 50bps). Additionally, the committee noted that it remains open to additional reductions. The minutes stated that the case for reducing the OCR by 50 basis points emphasised prolonged spare capacity and the associated downside risk to medium-term activity and inflation. Subsequently, has extended its descent on a 0.57 handle and hit its lowest level since April 11th.

- Click for a detailed summary

- Click for NY OpEx Details

FIXED INCOME

- USTs are trading firmer by a few ticks, following the positivity seen across global peers. Currently trading at the upper end of a 112-19+ to 112-25+ range. Nothing really driving sentiment today from a US perspective, but upside, which comes after the safe-haven related upside seen in the prior session. Now traders await a 10yr outing; as a reminder, the last sale was strong, receiving strong demand and a 1.3bps stop-through. FOMC Minutes (Sept) and a slew of Fed speakers will also be in focus, in a day which is void of key US data.

- Bunds are firmer today, in-fitting with the upside seen across peers. Upside today began into German data, before taking another leg higher on the release itself – an upward bias which has held throughout the morning thus far. To recap that German data in brief, Industrial Output printed well below expectations at -4.5% (exp. -1%), though the accompanying release highlighted some caveats; "The marked decrease may be explained, at least in part, by the combination of annual plant closures for holidays and production changeovers”. The upswing seen earlier in the year looks increasingly associated with US-tariff related front loading – following the data, ING suggests that there is now an increasing likelihood of another quarter of contraction for the German economy. Thereafter, the German auction was poor, but ultimately had little follow-through to price action.

- OATs are the relative outperformer today, as outgoing PM Lecornu aims to hold last-minute talks with opposition parties. To recap the situation in France, President Macron asked the PM to hold talks with the opposition parties, giving him a deadline until Wednesday evening. In a presser today, Lecornu said he will present his findings to Macron later this evening; overall, his comments leaned more positively, suggesting that the talks so far show a willingness to get this budget through by year-end. Moreover, Lecornu has suggested suspending President Macron’s pension reforms, which would be welcomed by those on the left. The outgoing PM will be speaking again at 19:00 BST. On the presser itself, some very marginal upticks were in OATs; the OAT-Bund 10yr spread has tightened from recent highs, currently trading around 83.6bps vs previous close at 86.15bps.

- Gilts are in the green alongside peers. Currently trading in a 90.69 to 90.83 range. UK press remains heavily focused on the looming Autumn Budget; most recently, the FT reported that Pimco and BlackRock have called Chancellor Reeves to build a larger buffer in the UK public finances in the November Budget to avoid years of uncertainty over tax and spending decisions. However, a factor boosting sentiment is the ONS revising down UK Government borrowing by GBP 2bln after a recent data error - which may alleviate some of the borrowing-related pressure the Chancellor faces. Today a strong 2029 auction, which saw a b/c of 2.92x had little impact on prices.

- UK sells GBP 5bln 4.00% 2029 Gilt: b/c 2.92x, avg. yield 4.095%, tail 0.8bps.

- Germany sells EUR 0.733bln vs exp. EUR 1bln 2.60% 2041 Bund and EUR 0.853bln vs exp. EUR 1bln 3.25% 2042 Bund.

- Click for a detailed summary

COMMODITIES

- Crude benchmarks are trading slightly higher, extending on the prior day's high, despite worries of oversupply in the market with OPEC+ hiked production at its last meeting (albeit by a smaller than expected magnitude) and amid forecasts in the US that point to a record domestic oil output. WTI and Brent continued the late bid from yesterday’s session to form a peak at USD 62.45/bbl and USD 66.15/bbl, respectively, at the time of writing, before a dip towards USD 62.12/bbl and USD 65.88/bbl, respectively, as commentary from the Egypt talks remains positive. Note: EIA is continuing normal publication schedules and data collection.

- Spot gold has broken the USD 4k/oz mark, extending to a peak of USD 4039/oz and thus far remaining near ATHs. The surge in precious metals also comes as investors look to safe havens away from the dollar to protect against rising government debt burdens, geopolitical tensions and expectations of the dollar to continue lower.

- Base metals remain rangebound as China re-enters the market tomorrow. 3M LME Copper dipped to a trough of USD 10.68k/t before reversing to a peak of USD 10.78k/t as copper consolidates after a record weekly gain. Amid copper consolidation, there continues to be a growing consensus that copper still has further to go, with forecasts being revised higher towards USD 11.5-12k/t by the first half of next year due to supply disruptions and a continuing weaker dollar.

- US Private Energy Inventories Data (bbls) Crude +2.8mln (exp. +1.9mln), Distillate -1.8mln (exp. -1.2mln), Gasoline -1.2mln (exp. -0.9mln), Cushing -1.2mln.

- Click for a detailed summary

NOTABLE DATA RECAP

- Swedish CPIF Flash MM (Sep) 0.2% (Prev. -0.2%); CPI YY Flash (Sep) 0.9% (Prev. 1.1%); CPIF Flash YY (Sep) 3.1% (Prev. 3.2%); CPIF Ex Energy Flash MM (Sep) 0.1% (Prev. -0.5%); CPIF Ex Energy Flash YY (Sep) 2.7% (Prev. 2.9%)

NOTABLE EUROPEAN HEADLINES

- French PM Lecornu to speak again at 19:00 BST

- French PM Lecornu said will present his findings to President Macron later this evening; said France must get a budget by year-end; talks so far showing a willingness to get this budget through by year-end. Sees possibility of dissolution of parliament as becoming more remote.

- French Socialist Leader Faure says the party cannot back the current budget plan, no guarantee that pension reforms will be suspended.

- UK ONS said there's an error in public finances data between Jan-Aug, citing HMRC error; VAT data error means public sector net borrowing in current and prior FY is a combined GBP 3bln lower. UK borrowing in the past five months of FY was GBP 2bln lower than previously thought.

- ECB's Rehn has warned there is a risk that inflation slows below the ECB's 2% inflation target, according to Bloomberg, citing the Karon Grilli podcast. There are downside inflation risks in sight over the next couple of years; cites EUR strength, stabilisation of wages and services inflation.

- ECB's Nagel said current monetary policy is appropriate; euro zone inflation close to 2% target, via Greek newspaper.

- ECB's Escriva said he cannot pre-empt direction of future policy move; inflation expectations are very much anchored ECB needs to be cautious. Outlook remains uncertain going forward. Wouldn't overemphasise a strong euro as a risk factor, European economy showing great deal of resilience. Trade disruptions from US are potentially inflationary. Inflation risks are very much balanced. Spanish housing supply lagging very much.

- BoE FPC Minutes: FPC decided to maintain the UK countercyclical capital buffer (CCyB) rate at 2% Risks associated with geopolitical tensions, global fragmentation of trade and financial markets, and pressures on sovereign debt markets remain elevated. Despite persistent material uncertainty around the global macroeconomic outlook, risky asset valuations have increased and credit spreads have compressed. There have been some notable credit defaults in the US automotive sector since the last meeting. A sudden or significant change in perceptions of Federal Reserve credibility could result in a sharp re-pricing of US dollar assets, including in US sovereign debt markets, with the potential for increased volatility, risk premia, and global spillovers.

NOTABLE US HEADLINES

- US President Trump's administration has pushed back its plans to roll out economic support for farmers this week due to the government shutdown, according to four people familiar with the talks cited by POLITICO. Furthermore, officials were said to have readied nearly USD 13bln from an internal USDA fund, although there is no final decision on how much will be used for farm aid, or when.

- US Senate leaders were reportedly trying to lock in votes on Tuesday evening with a variety of options, including the noms bloc, privileged resolutions (maybe Canada tariff disapproval), and the duelling CRs again, according to Punchbowl.

GEOPOLITICS

MIDDLE EAST

- "There are outstanding issues among the negotiators in Egypt", according to Al Arabiya sources.

- Hamas said group positivity is needed to reach a deal, said list of hostages' names exchanged on Wednesday according to agreed numbers, according to a statement.

- "An Israeli security source told Sky News Arabia: Israel insists on not accepting any ideas outside the Trump plan", according to Sky News Arabia

- The atmosphere in the Sharm el-Sheikh negotiations appears to be "very positive", according to a correspondent at Sky News Arabia.

- Hamas leader tells AFP: "Optimism" dominates Gaza talks, via Sky News Arabia.

- Iran's Foreign Minister Araghchi denies reports that he's been in direct contact with US Envoy Witkoff including secret meetings in Doha or Muscat.

RUSSIA-UKRAINE

- Russian Foreign Minister says maintaining Russia's obligations under the plutonium agreement with the US is no longer acceptable, via Tass.

CRYPTO

- Bitcoin is on the backfoot and slips back towards USD 122k whilst Ethereum underperforms and edges back below USD 4.5k.

APAC TRADE

- APAC stocks traded mixed with demand hampered following the negative handover from the US, where stocks snapped a 7-day win streak as small caps underperformed and with sentiment weighed on by AI-profitability concerns.

- ASX 200 was rangebound as gains in healthcare and the top-weighted financial industry were offset by underperformance in Tech and Consumer sectors.

- Nikkei 225 lacked conviction and oscillated around the 48,000 level amid a weaker currency and soft wages data.

- Hang Seng retreated on return from the holiday closure with tech stocks heavily represented in the list of worst performers, while mainland participants were still away but are set to return from the National Day Golden Week celebrations tomorrow.

NOTABLE ASIA-PAC HEADLINES

- RBNZ cut the OCR by 50bps to 2.50% vs mixed views between a 25bps and 50bps cut, while the committee remains open to further reductions in the OCR as required for inflation to settle sustainably near the 2% target mid-point in the medium term. RBNZ said higher near-term inflation could prove to be more persistent and that with spare capacity in the economy, inflation is expected to return to around the 2% target mid-point over the first half of 2026, but noted upside and downside risks to the inflation outlook. RBNZ Minutes revealed that the committee discussed the options of reducing the OCR by 25bps or by 50bps at the meeting, while it stated that the case for reducing the OCR by 50 basis points emphasised prolonged spare capacity and the associated downside risk to medium-term activity and inflation.

- Oxford Economics has brought forward their timing of the next BoJ 25bps rate hike to December from next year and have added another 25bps hike in mid-2026.

- Japanese Economy Minister Akazawa is expected to depart from his position, according to local reports via Mainichi newspaper.

DATA RECAP

- Japanese Overall Labour Cash Earnings (Aug) 1.5% vs. Exp. 2.6% (Prev. 4.1%, Rev. 3.4%)

- Japanese Real Cash Earnings YY (Aug) -1.4% vs Exp. -0.5% (Prev. 0.5%, Rev. -0.2%)