US Opening News: Trade in focus as China cracks down on NVIDIA's AI chips

10 Oct 2025, 11:03 by Newsquawk Desk

- China reportedly launched a customs crackdown on NVIDIA (NVDA) AI chips, according to FT; US President Trump said maybe they will have to stop importing massive amounts from China.

- China's Transport Ministry announces plans to impose special port fees on US vessels; fees effective from 14th October.

- BLS is preparing to release a September US CPI report despite the shutdown, according to the NYT. Bloomberg sources suggested staff have been recalled for the preparation of the publication by the end of the month.

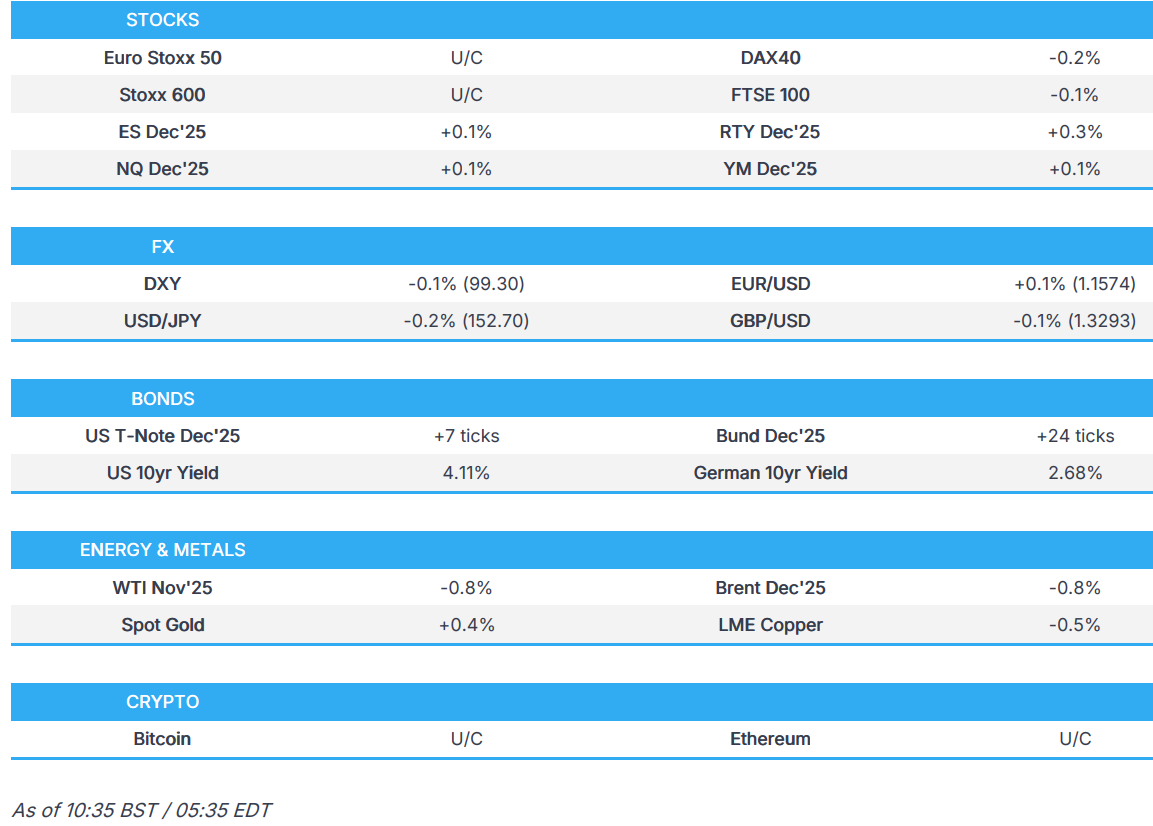

- European bourses are mixed and now generally hold a negative bias, US equity futures are slightly higher.

- DXY eases after four days of gains whilst JPY sees volatility on the 26-year-old coalition collapse.

- USTs gain whilst OATs lead, awaiting the French PM announcement.

- WTI/Brent are on the backfoot as the Gaza ceasefire plan; XAU is marginally higher.

- Looking ahead, Canadian Employment Report (Sep), US Uni. of Michigan Prelim. (Oct), Chinese M2/New Yuan Loans (Sep), Speakers including Fed’s Daly, Goolsbee & Musalem.

TARIFFS/TRADE

- China reportedly launched a customs crackdown on NVIDIA (NVDA) AI chips, according to FT, which reported that China stepped up enforcement of its controls on chip imports, as Beijing seeks to wean the country’s tech companies away from US products such as NVIDIA's AI processors.

- US Treasury Secretary Bessent said he believes the Chinese will come back at the end of the season and buy soybeans, while Bessent said India is going to start rebalancing over the next few weeks and months, in favour of US oil and will buy less Russian oil.

- US President Trump's administration said the US and Saudi Arabia are making progress on an agreement to allow US chip companies to export semiconductors to Saudi Arabia and could finalise a deal soon, according to WSJ.

- Japan's government said tariff negotiator Akazawa spoke with US Commerce Secretary Lutnick by phone, and they confirmed to smooth the implementation of the trade agreement to further strengthen ties.

- Indian PM Modi said he spoke with US President Trump and reviewed the good progress achieved in trade negotiations, while they agreed to stay in close touch over the coming weeks.

- China's Transport Ministry announces plans to impose special port fees on US vessels; fees effective from 14th October.

EUROPEAN TRADE

EQUITIES

- European bourses (STOXX 600 U/C) opened mixed and have traded with a slight negative bias throughout the session.

- European sectors are also mixed; Autos & Parts takes the top spot, boosted by strength in Ferrari (+1.5%) and Mercedes Benz (+3%). The Italian automaker attempts to pare back some of the pressure seen in the prior session, after its guidance disappointed investors. As for Mercedes, shares gain following a pre-close call in the prior session, where analysts highlighted that cash flow guidance remained unchanged, differing from the likes of BMW which recently downgraded its outlook.

- US equity futures (ES +0.1% NQ +0.1% RTY +0.3%) are broadly on a firmer footing today, with slight outperformance in the RTY. Focus this morning has been on a report via the FT, which suggested that China launched a customs crackdown on NVIDIA (+0.5% pre-market) AI chips.

- China says Qualcomm (QCOM) is suspected of violating China's antitrust law, via CCTV Securities Times. Adds that during Qualcomm's acquisition of Autotalks they failed to declare the concentration of operators as required and thus are suspected of violating anti-monopoly laws.

- Click for the sessions European pre-market equity newsflow

- Click for the additional news

- Click for a detailed summary

FX

- Subdued morning for the DXY thus far, with the recent modest losses in part a function of the JPY. Newsflow has been light this morning, with no path forward in the ongoing US government shutdown as it stands. On that note, the US Bureau of Labor Statistics is reportedly preparing to release the September CPI report despite the shutdown, according to the NYT. Bloomberg sources suggested staff have been recalled for the preparation of the publication of the report by the end of the month. The US CPI was scheduled to be released on October 15th. DXY remains above 99.00 and closer to the top end of yesterday's 98.70-99.56 range, with today's current parameter between 99.21-99.43.

- EUR is taking a breather following the prior day's losses, which saw a convincing breach under the 100 DMA (1.1634) amid Thursday's dollar strength. - In French politics, President Macron has invited all parties, except RN and LFI, to talks on Friday at 13:30BST, with the new Prime Minister set to be announced today. Analysts at ING posit "there is a general feeling that the political backing remains weak. The market-appeasing pledge by outgoing PM Lecornu about delivering on budget obligations is hardly enough to price out French risk". EUR/USD trades in a current 1.1553-1.1589 range

- The JPY resides as one of the better performers vs the USD, with strength in the Japanese currency seen as Japan's Komeito leader Saito met with LDP Leader Takaichi and conveyed his intention to withdraw from the 26-year-old coalition, citing the lack of sufficient answers on issues of politics and money. Japan's Komeito leader Saito says the party cannot vote for LDP leader Takaichi's premiership in parliament. The decision saw a net strength in the JPY but with two-way action seen amid dual implications: 1) strength, on the back of hurdles for Takaichi to pass dovish policies. 2) weakness, on renewed political instability. USD/JPY eclipsed yesterday's peak (153.23) to reach a high of 153.27 before falling to a 152.38 low on the Komeito coalition exit.

- GBP is flat uneventful trade following earlier weakness, with some traders suggesting technical GBP/USD eventually found support at yesterday's low (1.3280), and with GBP/EUR breaching 1.1500 to the downside more convincingly. GBP/USD has printed on either side of 1.3300 and sees the next downside level at the 5th of August low at 1.3260.

- Initially flat trade across the antipodeans amid tentative newsflow for the currencies and amid mixed sentiment in Europe. Kiwi later saw an opportunity to pare back some post-RBNZ losses amid light catalysts. Aussie traders next week look ahead to the RBA minutes, commentary from RBA governor Bullock, Assistant Governor Kent, and then the September Employment figures, whilst New Zealand sees few notable releases.

- Click for a detailed summary

- Click for NY OpEx Details

FIXED INCOME

- USTs are firmer, in-fitting with the above. At a 112-23 peak, a tick+ shy of yesterday’s 112-24+ best and by extension the 112-27 WTD high. Thus far, specifics light as we digest overnight Fed speak, updates concerning the BLS and the continued lack of substantial shutdown progress. On the BLS, the NY Times reported that some staff are being recalled to work only on the September CPI report (technically scheduled for next week, but shelved during shutdown). The series is required to determine the annual Social Security adjustment, which needs to be published by November 1st; as such, the narrative is that the BLS is preparing the release in anticipation of the gov’t reopening before month-end. For clarity, the staff are reportedly only working on CPI.

- JGBs traded in tandem with peers overnight but with slightly larger gains than those seen in USTs/Bunds despite a set of firmer-than-expected PPI data. Overnight, the benchmark got to a 135.95 peak early doors with gains of 23 ticks at best. Overnight, the benchmark got to a 135.95 peak early doors with gains of 23 ticks at best. Since, the action has been superseded by Komeito announcing it will be leaving the LDP-Komeito opposition. An update that adds further risk to the Japanese political landscape and potentially limits the scope of Takachi’s stimulus, lifting JGBs to a 136.16 peak with gains of 44 ticks at most. Since, the move has pared back to c. 136.00 as we await further details from Takaichi on her next steps, with the LDP seeking talks with Komeito next week on the subject.

- OATs are firmer by roughly 20 ticks. The deadline for Macron to announce his next PM is fast approaching. France needs to present its 2026 budget proposal by Monday, October 13th for a vote on it by the end of the year to be possible. While a full government cabinet is not needed to make a proposal, a PM is. Politico this morning reported that Macron is leaning towards giving caretaker Lecornu another chance. While the likes of Borloo remain an option, but a lesser one. Ahead Macron has since summoned all parties except RN and LFI to talks at 13:30BST today.

- Gilts opened higher by 21 ticks, following and marginally extending on the bias set by USTs and Bunds overnight. Though, similarly, the current 90.73 peak is shy of yesterday’s 90.83 best and by extension the 90.93 WTD peak. For the UK, focus remains on the upcoming budget as the NIESR outlines that an increase to income tax to plug the fiscal gap would be the least damaging way for Chancellor Reeves to deal with the situation.

- Bunds are lifting off Thursday’s 128.63 low and posting gains of c. 24 ticks at most. To a 128.91 high, eyeing the 129.01 peak from Thursday and then the 129.06 WTD best.

- Click for a detailed summary

COMMODITIES

- WTI and Brent are trading on the backfoot today, currently down by around USD 0.50/bbl and USD 0.60/bbl respectively. All focus remains on the situation in the Middle East, which has continued to move constructively, with Israel approving Trump's Gaza plan. It has been reported that the US President will land in Israel Monday morning, where he will hold a press conference. Most recently, the complex has notched new lows as the Israeli military confirmed the ceasefire agreement went into effect at 10:00 BST.

- Spot XAU consolidates in a c. USD 50/oz range following yesterday’s selloff back below the USD 4k/oz level, as the US dollar strengthens for the fourth straight day. Amid muted action in the yellow metal, XAG has reversed the prior day’s selloff and currently c. USD 0.50/oz away from a new ATH.

- Base metals continue to retrace on yesterday’s gains as production outages remain the key theme in the copper market. China’s re-entry into the markets helped 3M LME Copper peak at USD 11k/t, but as the greenback continued to strengthen, copper prices fell lower. 3M LME Copper continued to a low of USD 10.71k/t before bouncing back and is currently trading back above USD 10.8k/t.

- Saudi crude oil supply to China is set to fall to about 40mln barrels in November vs 51mln barrels in October, according to sources cited by Reuters.

- Shanghai Futures Exchange is adjusting the trading margin ratio and price limit range for nickel and tin futures, butadiene rubber and natural rubber futures; as of October 14th

- Click for a detailed summary

NOTABLE DATA RECAP

- Norwegian Core Inflation YY (Sep) 3.0% vs. Exp. 3.1% (Prev. 3.1%); Consumer Price Index YY (Sep) 3.6% vs. Exp. 3.5% (Prev. 3.5%)

- Italian Industrial Output MM SA (Aug) -2.4% vs. Exp. -0.4% (Prev. 0.4%); Y/Y (Aug) -2.7% vs. Exp. 0.5% (Prev. 0.9%)

NOTABLE EUROPEAN HEADLINES

- Politico reports that the general consensus is that French President Macron is leaning towards giving Lecornu another chance as PM. Since, President Macron has invited all parties, except RN and LFI, to talks on Friday at 13:30BST, via Politico citing France24.

- ECB's Kazaks says he expects ECB to be on hold for the foreseeable future, policy is around neutral mark, via Bloomberg TV. Euro strength and China price effect is a known unknown.

NOTABLE US HEADLINES

- Fed's Daly (2027 voter) said inflation has come in much less than had feared and the labour market is to a point where softening looks like it could be more worrisome if they don't risk manage it, while she added that policy is still modestly restrictive after the September rate cut and the Fed is also projecting more cuts, part of risk management.

- Federal Reserve Board announces expanded operating days of two large-value payments services, Fedwire® Funds Service and the National Settlement Service (NSS), to include Sundays and weekday holidays.

- US Treasury Secretary Bessent is finalising the first round of interviews for the next Fed Chair this week, according to FBN citing sources. It was also reported that Former Fed governor Larry Lindsey withdraws name from consideration for US Fed Chair position, according to CNBC.

- US President Trump said some Democrats are calling him to reopen the government, and he will be making permanent cuts to Democratic programmes in the shutdown.

- US Bureau of Labor Statistics is preparing to release a September CPI report despite the shutdown, according to NYT. Bloomberg sources suggested staff have been recalled for the preparation of the publication of the report by the end of the month. US CPI was scheduled to be released on October 15th.

- New York Attorney General Letitia James was indicted by the US Department of Justice, while she stated that the indictment is nothing more than a continuation of the President's desperate weaponisation of the justice system, and she will fight these baseless charges aggressively.

- US President Trump will make an announcement in the Oval Office from 17:00 EDT/22:00 BST on Friday.

GEOPOLITICS

MIDDLE EAST

- Israeli PM Netanyahu's office said Israel's government approved the Gaza plan for the release of all hostages. It was earlier reported that the Israeli PM's office said forces will not leave Gaza unless they are guaranteed there is no threat posed, while it added the mission in Gaza is not over.

- US President Trump's special Envoy Kushner said "We’ve made a deal here that isolates Hamas and encourages actors in the Arab world to pursue peace. This agreement ensures Israel’s security. If we need to act with force, we will. It will either happen the easy way or the hard way."

- US senior official said, hopefully, the Gaza deal will lead to an opportunity to expand the Abraham Accords. It was also stated that there will be 200 US troops deployed for Gaza as part of a joint task force which will include troops from Egypt and Qatar.

- Israeli Military says Gaza ceasefire agreement with Hamas came into effect at 10:00 BST

RUSSIA-UKRAINE

- Ukrainian Energy Ministry said Russian forces launched mass attacks on Ukrainian energy targets, while a Ukrainian official later stated that electricity was cut off in the entire eastern Ukraine following the Russian attack, according to Sky News Arabia.

OTHER

- UN Security Council will meet on Friday regarding tensions between the US and Venezuela, according to diplomats.

- Taiwan's President said they will accelerate their building of the T-Dome and establish a rigorous air defence system in Taiwan with multi-layered defence, high-level detection, and effective interception.

CRYPTO

- Bitcoin is flat and trades around USD 121k with Ethereum price action also lacklustre, trading around USD 4.3k.

APAC TRADE

- APAC stocks were mostly lower following the negative handover from Wall Street, where the stock market and gold prices pulled back from record levels, while the KOSPI outperformed against its regional counterparts on return from its extended holiday.

- ASX 200 lacked direction amid quiet catalysts and as weakness in the mining and materials sectors offset the strength in tech and financials.

- Nikkei 225 retreated following the firmer-than-expected PPI data, although participants also digested earnings updates, including from index heavyweight Fast Retailing, which was the biggest gainer after it reported a double-digit percentage increase in 6-month net.

- Hang Seng and Shanghai Comp conformed to the downbeat mood as trade frictions resurfaced following China's announcement of export controls on rare earth and items related to lithium batteries, while US President Trump commented that maybe they will have to stop importing massive amounts from China.

NOTABLE ASIA-PAC HEADLINES

- Japanese Finance Minister Kato said they are recently seeing one-sided, rapid moves, and it is important for currencies to move in a stable manner reflecting fundamentals, while he added they will thoroughly monitor for excessive fluctuations and disorderly movements in the forex market.

- Japan's Komeito leader Saito met with LDP Leader Takaichi and conveyed his intention to withdraw from the coalition, citing the lack of sufficient answers on issues of politics and money, according to NHK. Saito says the party cannot vote for LDP leader Takaichi's premiership in parliament.

- Japan's Komeito Leader Saito says if proposals are accepted then they will vote for passing supplementary budget through parliament Wish to hold additional talks with Komeito next week.

- Japan’s DPP Leader Tamaki says forming a coalition government with the LDP "has become a meaningless discussion", via JiJi.

DATA RECAP

- Japanese Corp Goods Price MM (Sep) 0.3% vs. Exp. 0.1% (Prev. -0.2%); YY (Sep) 2.7% vs. Exp. 2.5% (Prev. 2.7%)