US Market Open: Sentiment hit after China's MOFCOM takes action against US firms

14 Oct 2025, 11:23 by Newsquawk Desk

- China's MOFCOM announced that it is taking countermeasures against five US-linked firms; said the US cannot have talks while threatening new restrictions.

- French PM Lecornu's government is to present a budget aiming to reduce the deficit to 4.7% by end-2026, according to La Tribune.

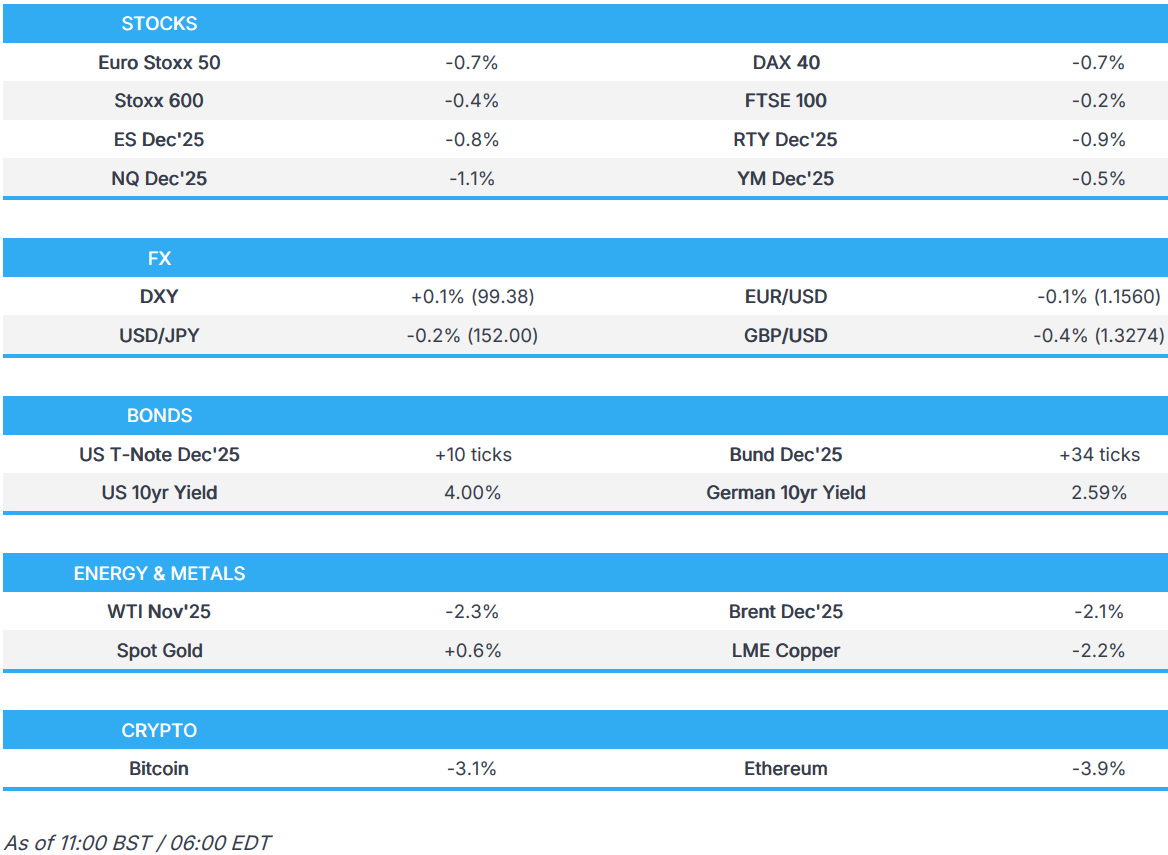

- Equities lower across the board, as markets digest the latest trade-related escalations by China on the US; traders also await a number of US earnings.

- JPY benefits from haven bid, GBP hit by soft jobs, Antipodeans dented by risk-tone.

- Global paper firmer amid the weakened risk tone, Gilts lead after data, OATs await PM Lecornu.

- Crude benchmarks fall as Middle East tensions ease, XAU pulls back from new ATHs.

- Looking ahead, US NFIB (Sep), Fed Discount Rate Minutes, Speakers including ECB’s Villeroy, Kocher, BoE’s Bailey & Taylor, Fed’s Powell, Waller, Collins & Bowman, BoC’s Rogers, RBA’s Hunter & Hauser, RBNZ’s Conway. Earnings from JPMorgan, Goldman Sachs, Citi, Wells Fargo, Johnson & Johnson & LVMH.

TARIFFS/TRADE

- China officially began special port fees for US ships, while it was earlier reported that China issued implementation rules on port fees on US ships and exempted China-made ships owned by US companies from port fees, while it is to adjust special port fees on US ships as needed.

- China's MOFCOM responded to the US saying it has proposed talks with China after rare earth restrictions, in which MOFCOM stated the US cannot have talks while threatening to intimidate and introduce new restrictions, which is not the right way to get along with China, while it urged the US to correct its “wrong practices” as soon as possible and show sincerity in talks with China. It also stated that export curbs are not an export ban and do not prohibit exports. Furthermore, it said they held working-level talks on Monday and noted that both sides have maintained communication under the framework of the China-US economic and trade consultation mechanism. However, MOFCOM later announced that it is taking countermeasures against five US-linked firms.

- China Transport Ministry said it opened an investigation into the impact of US 301 tariffs on China's shipping industry.

- China's Commerce Ministry urges the US to correct mistakes and hopes to resolve concerns through dialogue.

- China increases oversight of export license applications for rare earth magnets, via Reuters citing sources.

EUROPEAN TRADE

EQUITIES

- European bourses (STOXX 600 -0.4%) are broadly lower across the board, with sentiment hampered by the ongoing US-China spat; overnight, China's MOFCOM announced that it is taking countermeasures against five US-linked firms.

- European sectors hold a strong negative bias. Telecoms takes the top spot, boosted by post-earning strength in Ericsson (+13%) after it beat on profits and raised guidance. To the bottom of the pile resides Basic Resources, hampered by broader weakness in underlying metals prices.

- US equity futures (ES -0.8%, NQ -1.1%, RTY -0.9%) are lower across the board, following a similar theme seen in Europe. All focus today on a number of bank results, to kick off Q3 earnings seasons.

- BP (BP/ LN) Q3'25 Trading Statement: Upstream Production in Q3 is now exp. to be higher vs prior quarter, but flagged weaker trading into Q3.

- BlackRock Inc (BLK) Q3 2025 (USD): Adj. EPS 11.55 (exp. 11.24), Revenue 6.51bln (exp. 6.23bln); AUM 13.464tln (exp. 13.37tln).

- Click for the sessions European pre-market equity newsflow

- Click for the additional news

- Click for a detailed summary

FX

- After a soft start to the session, whereby DXY was dragged lower by the haven bid into the JPY, the Greenback was able to garner support at the expense of risk-sensitive currencies and the GBP (post-jobs data). The bout of risk aversion was triggered by China's decision to take countermeasures against five US-linked firms - a move which has dashed some of the hopes seen during yesterday's session. Furthermore, a source piece in the WSJ overnight stated that "people close to the Trump administration say the US side likely will demand that China rescind, not merely delay or water down the rare-earth export rule". Focus today on US NFIB Small Business Optimism index, and speakers include Fed Chair Powell, Waller, Collins & Bowman. DXY has ventured as high as 99.47, with the next target coming via last week's peak at 99.56.

- After initially looking like it was going to make a test of 1.16 overnight, EUR/USD was dragged lower by the broader pick-up in the USD. From a macro perspective, focus in the Eurozone remains on France with PM Lecornu set to present his budget at 14:00BST, aiming to reduce the deficit to 4.7% by end-2026. In terms of the specifics, Politico reports that additional measures to those previously expected will include a tax on the richest members of society. Even with the Socialists on board, the governing coalition would still need to find additional votes in the Assembly, which looks tough given that the Far Right and Left are expected to table a no-confidence motion on Lecornu. Elsewhere in core Europe, German ZEW data showed misses for both metrics, with the current conditions component slipping further into negative territory. EUR/USD has been as low as 1.1543 and is just about holding above last week's low at 1.1542.

- JPY is the only of the majors to out-muscle the USD given its safe-haven status. JPY was supported in early European trade as investors reacted to the increase in US-China tensions overnight (see USD section for details). Subsequently, USD/JPY was dragged as low as 151.63 vs. an earlier session high at 152.61. A pick-up in the USD has since seen the pair return to a 152 handle. In terms of the macro story for Japan, it is one that remains dominated by domestic politics following the collapse of the ruling coalition. Note, the LDP party has proposed October 21st for an extraordinary Diet session.

- GBP was hit in early European trade following the latest UK labour market report, which was largely viewed with a dovish lens. Surmising the data, Pantheon Macroeconomics highlighted the unexpected uptick in the unemployment rate and the decline in 3M/YY ex-bonus average earnings, which will factor into thinking on the MPC. Elsewhere, BRC retail sales slowed to 2.0% Y/Y in September from 2.9% as consumers remain cautious in the run-up to next month's fiscal event. Cable has delved as low as 1.3255 to levels not seen since early August.

- Antipodeans are both are softer vs. the USD and at the bottom of the G10 leaderboard. In the absence of any material domestic updates, AUD and NZD remain at the whim of broader risk dynamics, which are being led by US and Chinese trade tensions.

- Click for a detailed summary

FIXED INCOME

- USTs are bid, firmer by over 10 ticks to a 113-16+ high. Strength this morning comes on the back of the downbeat risk tone as China retaliates. Upside that has driven the benchmark to a fresh high for the month, with the next points of resistance at 113-21, 113-25+ and then the 113-29 September peak. Specifically, China's MOFCOM announced that it is taking countermeasures against five US-linked firms and outlined that the US cannot have talks while new restrictions are being threatened. Elsewhere, the docket is packed with Fed speak via voters Bowman, Waller, Chair Powell and 2025 voter Collins.

- OATs are firmer today, in-fitting with peers. A packed agenda for French politics. The main update this morning came from the French fiscal watchdog HCFP on the 2026 budget draft, a draft that was in-fitting with overnight sources. On the draft, HCFP described it as relying on overly optimistic scenarios and ambitious spending restraint that would be difficult to implement. Perhaps most pertinently today, PM Lecornu’s General Policy Statement is scheduled for 14:00BST. The statement should take no more than 90 minutes, afterwards other party leaders can respond. It is worth highlighting that the French Socialist Party will not vote against PM Lecornu's government, and instead opt for its own motion of no confidence, if it not satisfied with the proposal.

- Bunds are bid, given the market narrative outlined in USTs. No move to final German HICP for September this morning which was unrevised. For Bunds, the morning’s main event was October ZEW. The series came in softer than expected across the board and sparked some modest upside in Bunds, though well within earlier parameters. No move to a new Schatz auction which was fairly weak.

- Gilts are outperforming after the morning’s jobs data. Opened higher by 45 ticks before climbing to a 91.81 peak with gains of 57 ticks at best. Stopping a tick shy of the 91.82 September peak; if the move continues, then there is a bit of a gap before the 92.70 August high. The morning’s data saw an unexpected jump in the unemployment rate, going against the view from the most recent MPC statement that there is less of an immediate risk that the labour market will loosen very rapidly. A point that serves as a dovish impetus. However, this is caveated on face value by the elevated wage figure (incl-bonus). Upside that the ONS attributes to the public sector, as some pay rises are awarded earlier than they were in 2024.

- Germany sells EUR 4.25bln vs exp. EUR 5.5bln 2.00% 2027 Schatz: b/c 1.4x, average yield 1.91%, retention 22.7%.

- Italy sells EUR 8.5bln vs exp. EUR 6.75-8.5bln 2.35% 2029, 3.25% 2032, 2.80% 2028, 3.85% 2040 BTP.

- UK to sell GBP 9bln of 5.25% 2041 Gilt via syndication, according to a bookrunner cited by Reuters- Click for a detailed summary

COMMODITIES

- Crude benchmarks are trending lower as renewed trade worries, easing geopolitical tensions, and an oversupplied oil market weigh on prices. Benchmarks are steadily declining as the European session continues, with WTI and Brent currently c. USD 1.7/bbl lower and trading near lows at USD 58.20/bbl and USD 62.00/bbl, respectively.

- Precious metals extended to new ATHs during APAC trade, with XAU and XAG peaking at USD 4180/oz and USD 53.59/oz respectively, before selling off as US President Trump hints of total peace in the Middle East.

- Base metals have reversed Monday’s gains, with 3M LME Copper returning to USD 10.5k/t from a peak of USD 10.86k/t, as recent dollar strength weighs on the commodity space.

- IEA OMR: lowers 2025 world oil demand growth forecast to 710k BPD (prev. 740k BPD); leaves 2026 average oil demand growth forecast steady at 700k BPD.

- TotalEnergies (TTE FP) CEO says they are still quite bullish in medium term oil demand; CEO says there is no peak oil demand.

- US Energy Secretary Wright is set to announce the Trump administration's fusion roadmap at an industry gathering on Tuesday, via Axios citing DOE officials.

- Click for a detailed summary

NOTABLE DATA RECAP

- UK ILO Unemployment Rate (Aug) 4.8% vs. Exp. 4.7% (Prev. 4.7%); Employment Change (Aug) 91k vs. Exp. 123k (Prev. 232k)

- UK Avg Wk Earnings 3M YY (Aug) 5.0% vs. Exp. 4.7% (Prev. 4.7%, Rev. 4.8%); Ex-Bonus (Aug) 4.7% vs. Exp. 4.7% (Prev. 4.8%)

- UK HMRC Payrolls Change (Sep) -10k vs. Exp. -10k (Prev. -8k); Claimant Count Unem Chng (Sep) 25.8k (Prev. 17.4k, Rev. -2.0k)

- UK BRC Retail Sales YY (Sep) 2.0% (Prev. 2.9%); Total Sales YY (Sep) 2.3% (Prev. 3.1%)

- German HICP Final YY (Sep) 2.4% vs. Exp. 2.4% (Prev. 2.4%); MM (Sep) 0.2% vs. Exp. 0.2% (Prev. 0.2%)

- German ZEW Economic Sentiment (Oct) 39.3 vs. Exp. 41.0 (Prev. 37.3); Current Conditions (Oct) -80.0 vs. Exp. -74.8 (Prev. -76.4)

- EU ZEW Survey Expectations (Oct) 22.7 (Prev. 26.1)

NOTABLE EUROPEAN HEADLINES

- Barclays UK September Consumer Spending fell 0.7% Y/Y vs prev. 0.5% Y/Y increase in August.

- The tax elements of French PM Lecornu's draft finance bill reportedly include 30 articles, some have already been announced, but also the addition of a tax on "assets not allocated to an operational activity of property holding companies", via Playbook. Furthermore, Playbook, citing a source, reports that there is no question for the PS of "doing another round of negotiations on Wednesday, Thursday or Friday".

- The two motions of censure will be looked at on Thursday at 08:00 BST, but the Conference of Presidents on the National Assembly, via BFMTV.

- French fiscal watchdog HCFP says French government’s 2026 budget plan relies on overly optimistic economic assumptions; based on ambitious spending restraint that would be difficult to implement. France is at risk of under-delivering on spending and tax measures in 2026 budget. Budget bill includes belt-tightening measures worth over EUR 30bln, including EUR 13.7bln in taxes and EUR 17bln in spending cuts.

- French Socialist Party (PS) will not vote against PM Lecornu's government in the motions filed by LFI and RN, will instead file its own motion of no confidence in the scenario it is not satisfied with the budget proposals, via Reuters citing sources

- German Economy Ministry says current indicators do not point to economic recovery in Q3.

- Riksbank's Bunge says monetary policy must be forward looking; Inflation remains elevated, but with increased confidence that it will fall back, we were able to cut the policy rate to provide further support to the economy.

- EU Commission modifies drone wall proposals to suggest broader European drone defence initiative, via Reuters sources.

NOTABLE US HEADLINES

- Republicans on Capitol Hill and inside the Trump administration are said to be discussing potential pathways to prevent the tax credits from expiring at the end of the year, according to Politico. Some members of the House GOP leadership circle are having early, informal conversations with officials from the White House Office of Legislative Affairs and the Domestic Policy Council to develop a framework for a deal.

GEOPOLITICS

MIDDLE EAST

- US President Trump is said to have confirmed that Israeli PM Netanyahu will not annex any part of the West Bank, according to Al Arabiya.

- Iran's Foreign Ministry says US President Trump's desire for peace and dialogue is in conflict with US hostile and criminal behaviour against Iran.

- US President Trump posts "Gaza is only a part of it. The big part is, PEACE IN THE MIDDLE EAST!".

- Israeli's Defence Force says several suspects were identified crossing the yellow line and approaching IDF troops operating in the northern Gaza Strip, which constitutes a violation of the agreement; troops opened fire to remove the threat, via CGTN.

CRYPTO

- Bitcoin is a little lower and trades around USD 111.3k with Ethereum underperforming a touch, back below USD 4k.

APAC TRADE

- APAC stocks were mixed following the rebound on Wall St and with underperformance in Japanese markets as they reopened from the extended weekend and reacted to the recent US-China tariff tensions, as well as the Japanese ruling coalition split.

- ASX 200 struggled for direction as weakness in the financial and consumer-related sectors offset the gains in materials and miners, with the latter helped by the recent upside in metal prices and with Rio Tinto gaining following its quarterly activity update.

- Nikkei 225 underperformed as participants returned from the holiday closure and reacted to the recent US-China trade frictions and political uncertainty in Japan, while there were late headwinds after reports of China trade-related actions against the US.

- Hang Seng and Shanghai Comp are lower amid the backdrop of the tumultuous trade/tariff related headlines in which the recent softening in tone by the US on China was followed by reports overnight that China's MOFCOM is taking countermeasures against five US-linked firms and that China's Transport Ministry opened an investigation into US 301 tariffs impact on China shipping industry.

NOTABLE ASIA-PAC HEADLINES

- Monetary Authority of Singapore kept the prevailing rate of appreciation of the SGD NEER policy band, as well as made no change to the width and level at which the band is centred, as expected. MAS said it is in an appropriate position to respond effectively to any risk to medium-term price stability and MAS core inflation should trough in the near term but rise gradually over the course of 2026, while it added that Singapore’s economic growth has turned out stronger than expected and the output gap will remain positive in 2025.

- RBA Minutes from the September meeting stated the Board agreed no need for immediate reduction in the cash rate, while it added that future policy decisions are to be cautious and data dependent. RBA said the market path for the cash rate is within estimates of neutral but too imprecise to guide policy and it is important to see what Q3 data shows on the economy and supply capacity, as well as noted that policy is probably still a little restrictive, but this is difficult to determine and there are still risks on both sides for the economy.

- Japan's LDP proposes October 21st for extraordinary Diet, via FNN.

- China's Central Bank-backed Publication will continue to uphold decisive role of market in exchange rate formation and strengthen guidance of expectations.

DATA RECAP

- Singapore GDP QQ (Q3 A) 1.3% vs Exp. 0.5% (Prev. 1.4%); YY (Q3 A) 2.9% vs Exp. 1.9% (Prev. 4.4%)

- Australian NAB Business Confidence (Sep) 7.0 (Prev. 4.0); Business Conditions (Sep) 8.0 (Prev. 7.0, Rev. 8)

- Indian WPI Inflation YY (Sep) 0.13% vs. Exp. 0.5% (Prev. 0.52%)