US Market Open: NQ outperforms following TSMC +1.8% results, Trump says US-China are in a trade war

16 Oct 2025, 11:27 by Newsquawk Desk

- US President Trump said they are in a trade war with China, and if the US don't have tariffs, they don't have national security, while he stated that tariffs are a very important tool for defence.

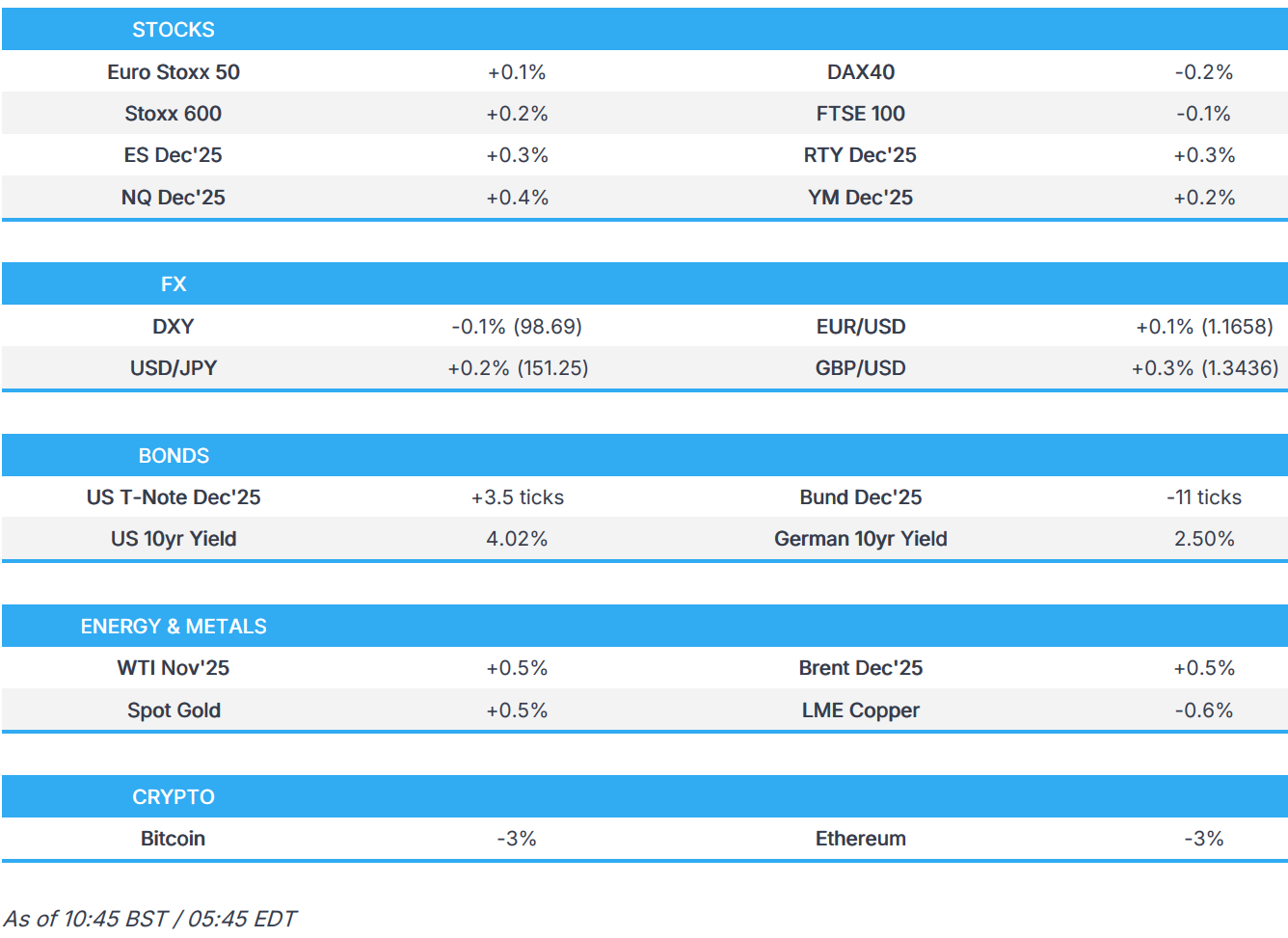

- European bourses are mostly higher, SMI bid post-Nestle results and NQ outperforms after strong Q3 TSMC earnings.

- USD mixed vs. peers, GBP leads whilst AUD was pressured by a weak jobs report.

- USTs are firmer, fleeting upside in OATs after PM Lecornu survives the 1st no confidence vote; now awaiting the 2nd vote.

- Crude benchmarks trade rangebound despite rising geopolitical tensions, XAU forms another new ATH.

- Looking ahead, highlights include Philly Fed (Oct), Atlanta Fed GDP, Comments from Fedʼs Waller, Barkin, Barr, Miran, Bowman & Kashkari, ECBʼs Lane & Lagarde, BoCʼs Macklem, BoEʼs Greene & Mann.

- Earnings from Bank of New York Mellon, KeyCorp, Charles Schwab, United Airlines, ABB & Bankinter.

TARIFFS/TRADE

- US President Trump said they are in a trade war with China, and if the US don't have tariffs, they don't have national security, while he stated that tariffs are a very important tool for defence.

- US President Trump claimed that South Korea signed a deal to make an "upfront" payment of USD 350bln to invest in the US, while it was also reported that Treasury Secretary Bessent said that South Korea and the US can resolve their differences over how to implement Seoul's USD 350bln investment pledge, and that he expects "something" to come "in the next 10 days", according to Yonhap.

- South Korean Presidential Policy Chief noted optimism when asked about tariff talks with the US, while South Korea's Finance Minister said the US may accept South Korea's proposal in tariff talks, according to Yonhap

- Mexican Economy Minister Ebrard said Mexico is in talks with the US to discount tariffs on heavy truck parts.

- Federal officials said they have found no evidence of widespread undervaluing of imported appliances after Whirlpool (WHR) last month accused its rivals of possible tariff evasion, according to WSJ.

- Russian Deputy PM Novak responds to US President Trump's remarks on India: says Russia continues to collaborate with partners, and Novak is confident partners will continue to work with them.

- China's Commerce Ministry said it took a constructive stance during recent US-China trade talks. Says rare earth export controls are different to an export ban. All licence applications for civilian use will be approved.

EUROPEAN TRADE

EQUITIES

- European bourses (STOXX 600 +0.2%) opened broadly modestly firmer, and have traded sideways throughout the morning. A brief slip seen in the earlier part of the morning, with no clear driver. Thereafter, indices picked up off worst levels amidst constructive trade-related commentary from the Chinese Commerce Ministry; it noted that "All licence applications for civilian use will be approved".

- European sectors are mixed. Consumer Staples has been boosted by post-earning strength after it reported decent Q3 metrics and announced job cuts. Elsewhere, Consumer Discretionary has been hampered by some downside in Luxury names; LVMH and Kering both received downgrades, with downside also likely some profit-taking after Wednesday's considerable upside.

- US equity futures are broadly firmer across the board, but with some clear outperformance in the NQ. The Tech sector has been boosted by pre-market upside in TSMC (+1.7%) after the Co. reported strong Q3 figures and lifted guidance. Commentary surrounding AI demand and Capex were also positive.

- Nestle (+7%) 9-month results marginally beat; announced 16k job cuts.

- TSMC (+1.7% pre-market) strong Q3 metrics and upgraded FY guidance.

- Click for the sessions European pre-market equity newsflow

- Click for the additional news

- Click for a detailed summary

FX

- DXY is a touch lower with the USD overall showing a mixed performance vs. peers. The US macro narrative remains fixated on the recent escalation of trade tensions between the US and China with the latest salvo from Trump being that, if the US doesn't have tariffs, they don't have national security. For now, the focus for the market is whether this is merely a negotiating tactic by Trump or a genuine intention to squeeze the Chinese economy. The US government remains shutdown and as such, tier 1 data points are lacking. For today's agenda, the Philly Fed Business Index is due following yesterday's solid NY Fed Manufacturing print. Elsewhere, the speaker slate includes Fedʼs Waller, Barkin, Barr, Miran, Bowman & Kashkari. DXY hit a WTD low overnight at 98.41 before trimming losses.

- EUR is a touch firmer vs. the USD in the run-up to the no-confidence votes in French PM Lecornu. The first motion put forward by the far-right National Rally (RN) will likely fail, as RN and the Union for Democratic Change (UDR) are the only major parties that are backing it. The second motion, put forward by the far-left, La France Insoumise (LFI), has a greater potential to pass given that it could see support from both the Left and the Right. If Lecornu survives, there will likely be some additional reprieve for the EUR and a narrowing of the GE/FR spread. If he falls, odds of fresh legislative elections will rise. Elsewhere, ECBʼs Lane, Lagarde, Wunsch and Kocher are due to give remarks later. EUR/USD has been as high as 1.1675.

- JPY is fractionally firmer vs. the USD with the pair extending above the 151 mark. The focus for Japan remains on domestic politics with LDP leader Takaichi scrambling to secure her position as PM. Her path to power appears to be reliant on forming an alliance with the Japanese Innovation Party (JIP) with the parties having met today and expected to continue discussions tomorrow. Overnight, BoJ's Tamura said the BoJ should push rates closer towards levels deemed neutral. However, his comments had little follow-through to JPY, given he is the most hawkish member on the board. USD/JPY is still some way off yesterday's peak at 151.87.

- GBP is firmer vs. the USD and extending on Wednesday's upside. August's M/M UK GDP printed in-line with expectations at 0.1% with the prior revised lower to -0.1% from 0%. On the budget, the latest trial balloon from the Treasury is that taxes on the wealthy "will be part of the story". For today's agenda, BoE's Mann and Greene are due to give remarks. Cable has ventured as high as 1.3442 with the next upside target coming via the 50DMA at 1.3473.

- AUD is flat vs. the USD after shrugging off overnight losses that were triggered by the latest Australian labour market report. The release saw an unexpected uptick in the unemployment rate and a smaller-than-forecast increase in employment change. Subsequently, AUD/USD slipped onto a 0.64 handle, delving as low as 0.6480 with odds of an RBA rate cut standing at circa 71%.

- PBoC set USD/CNY mid-point at 7.0968 vs exp. 7.1186 (Prev. 7.0995).

- Click for a detailed summary

- Click for NY OpEx Details

FIXED INCOME

- USTs are slightly firmer thus far, in contrast to EGBs and Gilts. However, magnitudes are slim with gains of just 6+ ticks at most in a 113-08 to 113-13+ band. A parameter that is entirely within Wednesday’s 113-06+ to 113-17+ range. Thus far, the main points of focus are US President Trump saying they are in a trade war with China. Though, commentary this morning from China’s Commerce Ministry has perhaps been a little more conciliatory than we have seen in recent sessions. Ahead, Fed speakers in focus with six officials appearing a total of nine times across the day. Additionally, we await the Philly Fed manufacturing report, which follows this week's upside surprise seen in the Empire manufacturing survey, and ahead of PMI data due next week.

- OATs marginally bid as the French PM survives the 1st no confidence motion; now awaiting 2nd vote. Into the second vote, OATs trade slightly heavier than Bunds with the OAT-Bund 10yr yield spread wider today and as high as 78.5bps. Of the two motions, the one filed by La France Insoumise (LFI) has a chance of passing; full Newsquawk primer available on the feed. For the motion to pass, a majority in the Assembly of 289 votes is needed. Elsewhere, no move to the morning’s French tap which, while taken down well enough and without reaction, was a little softer than the last very strong outing.

- A slightly softer start to the day. Bunds have at most posted losses of 21 ticks at a 129.93 trough. However, this has since moderated a touch to losses of just under 10 ticks in a 129.93 to 130.14 band. Specifics for the benchmark were a little light, no supply from Germany though the Spanish tap was received well enough and spurred no discernable reaction. Elsewhere, the final Italian inflation print for September was unrevised

- Gilts opened unchanged at Wednesday’s 92.43 close. External leads prior to the open were a little mixed, with USTs firmer while Bunds were softer but both within reach of the unchanged mark. The morning’s main update for the UK was August growth data. Overall, the series came in broadly as expected though the return to growth for the headline was offset by a downward revision to negative territory for July’s M/M figure. The data doesn't change the narrative for the BoE of a hold in November and a cut being possible in December. With a move dependent on how the next data points print (particularly CPI) and the November Budget. On that, the Guardian adds to recent reports around taxes for the wealthiest members of society while the FT previews the launch of a pension funds initiative next week.

- Spain sells EUR 4.442bln vs exp. EUR 4.0-5.0bln 1.25% 2030, 2.55% 2032 and 3.20% 2035 Bono.

- France sells EUR 11.499bln vs exp. EUR 9.5-11.5bln 2.40% 2028, 2.50% 2030, 2.70% 2031, and 0.00% 2031 OAT.

- Click for a detailed summary

COMMODITIES

- Crude benchmarks remain rangebound throughout the APAC session despite increased Russian oil restrictions and rising trade tensions. WTI and Brent oscillate in a USD 58.55-59.11/bbl and USD 62.18-62.75/bbl band respectively, as markets wait for further confirmation of Russian oil export restrictions. Most recently, crude futures have dipped down to fresh lows, but lacks a clear driver.

- Spot XAU continues to climb to record levels, peaking at USD 4242/oz during the APAC session and currently trading just shy of best levels at USD 4230/oz. This comes as US-China tensions, ongoing US government shutdown and further expectations of rate cuts in the US drive the precious metal higher.

- Base metals currently trading relatively muted as trade tensions weigh on the metal space while structural challenges support the metal space. 3M LME Copper is currently oscillating in a c. USD 130/t range as the market waits for more news.

- Vice President of Transneft says companies have not reduced oil supplies to the pipeline system; have enough capacity as Russia's OPEC+ oil output quota increases.

- "Russian Energy Minister: Oil refineries will postpone maintenance work to meet market needs", according to Al Arabiya.

- UBS sees the decline in real rates, potentially into negative territory, further boosting the portfolio appeal of gold, which could rise towards UBS' upside case of USD 4,700/oz.

- Equinor (EQNR NO) says production has started at its Bacalhau field (220k BPD)

- US Private Inventory Data (bbls): Crude +7.4mln (exp. -0.3mln), Distillate -4.8mln (exp. -0.3mln), Gasoline +3.0mln (exp. -0.1mln).

- US President Trump said Indian PM Modi assured him that they won't buy Russian oil, while he added that they now need to get China to stop buying Russian oil. It was later reported that some Indian oil refiners are preparing to cut Russian oil imports, with refiners expecting a gradual reduction in imports, according to Reuters sources.

- Saudi Aramco CEO warned of a global oil shortage if the industry fails to invest, according to FT.

- Ukraine's military says it struck Russia's Saratov oil refinery (140k BPD) overnight

- Click for a detailed summary

NOTABLE DATA RECAP

- UK GDP Estimate MM (Aug) 0.1% vs. Exp. 0.1% (Prev. 0.0%, Rev. -0.1%); 3M/3M (Aug) 0.3% vs. Exp. 0.3% (Prev. 0.2%)

- UK Services MM (Aug) 0.0% vs. Exp. 0.1% (Prev. 0.1%, Rev. 0.0%); YY (Aug) 1.7% vs. Exp. 1.6% (Prev. 1.5%, Rev. 1.7%)

- UK Manufacturing Output MM (Aug) 0.7% vs. Exp. 0.2% (Prev. -1.3%, Rev. -1.1%); YY (Aug) -0.8% vs. Exp. -1.0% (Prev. 0.2%, Rev. -0.1%)

- UK Industrial Output MM (Aug) 0.4% vs. Exp. 0.1% (Prev. -0.9%, Rev. -0.4%); YY (Aug) -0.7% vs. Exp. -0.7% (Prev. 0.1%, Rev. -0.1%)

- UK Goods Trade Balance GBP (Aug) -21.18B vs. Exp. -21.90B (Prev. -22.244B, Rev. -20.65B)

- Italian Consumer Prices Final YY (Sep) 1.6% vs. Exp. 1.6% (Prev. 1.6%); Consumer Prices Final MM (Sep) -0.2% vs. Exp. -0.2% (Prev. -0.2%)

NOTABLE EUROPEAN HEADLINES

- French PM Lecornu survives 1st round of no confidence motion; with 271 lawmakers voting against the government (vs 289 threshold to oust government)

- IFS writes that Chancellor Reeves would need to raise the fiscal buffer to around GBP 50bln vs the GBP 9.9bln she had in March, in order to have a better than 50-50 chance of avoiding additional tax increases and/or spending cuts, according to Bloomberg.

- UK Chancellor Reeves is to launch an initiative next week with 20 of the UK’s largest pension funds, which will try to make it more seamless for pension funds to back British infrastructure and growth projects, according to FT.

- ECB's Dolenc says rates should hold steady unless new shock hits, inflation risks are balanced, growth on a solid path.

- Swiss Government forecasts: Higher US tariffs have further clouded the outlook for the Swiss economy; forecast reflects expectations of a weak second half of 2025 and is based on the assumption that international tariffs will remain at current levels.

NOTABLE US HEADLINES

- US Treasury Secretary Bessent said the US investment boom is sustainable and just getting started, while he stated there is pent-up demand and America is open for business, according to CNBC. Bessent said the only thing slowing the US and President Trump down is the government shutdown, and he has seen numbers that the shutdown is hurting the economy by up to USD 15bln a day.

- US Treasury official said the government shutdown could cost the US economy USD 15bln per week, correcting Treasury Secretary Bessent's recent comments that estimated USD 15bln of costs per day.

- US Senate is set to leave for the week on Thursday and is nowhere near ending the shutdown, according to a former Politico journalist.

- BofA total card spending (w/e 11th Oct) +3.7% Y/Y (prev. 2.2%); surge driven either by higher prices during Amazon's (AMZN) Prime Day amid tariffs, or strong demand.

- US bipartisan group of senators reportedly discussing several different potential off-ramps involving the enhanced Obamacare subsidies, according to Punchbowl sources; discussing the possibility of two side-by-side votes intended to end the shutdown.

GEOPOLITICS

MIDDLE EAST

- IDF says "Sirens sounding in Eilat following a hostile aircraft infiltration", via X; Eilat alarms in Israel were a false alarm, according to Al-Hadath correspondent.

- Israel reportedly gave the US new intelligence that shows Hamas has access to more of the bodies than it claims, according to Axios' Ravid, while it was separately reported that the Red Cross received the remains of two new hostages, according to Sky News Arabia.

- US senior advisor said there were very positive conversations involving the US on making sure aid reaches Gaza, while the advisor stated that stabilisation forces are starting to be constructed and that many countries have raised their hand to be part of a Gaza stabilisation force.

- "Senior Egyptian official to Saudi Al-Hadath TV: The issue of the return of the dead hostages may lead to the postponement of the next stages of the Trump plan", according to Kann News.

RUSSIA-UKRAINE

- US President Trump said Ukraine would like to go on the offensive in the war with Russia, while he also suggested that Russian President Putin could make a settlement.

OTHER NEWS

- US President Trump confirmed that he authorised the CIA to operate in Venezuela.

- Venezuela's government said it rejects the statement by US President Trump in which he publicly admitted to having authorised operations to act against the peace and stability of Venezuela, while it stated the US statement constitutes a violation of international law and the UN Charter. Furthermore, it stated that US manoeuvres seek to legitimise an operation of "regime change" with the ultimate aim of appropriating Venezuelan oil resources.

CRYPTO

- Bitcoin is a little lower and trades back towards USD 110k, Ethereum also posts losses and back below USD 4k.

APAC TRADE

- APAC stocks took impetus from the positive handover from Wall Street, where most major indices ultimately gained despite a choppy performance as US-China frictions remained in focus.

- ASX 200 printed a record high with most sectors in the green amid a softer yield environment, which was facilitated by a rise in unemployment.

- Nikkei 225 climbed higher and was unfazed by disappointing Machinery Orders and comments from BoJ hawk Tamura.

- Hang Seng and Shanghai Comp lagged behind regional peers amid US-China frictions, and with the Hong Kong benchmark underperforming amid weakness in Chinese tech stocks, while it was also reported that the FCC is to expel Hong Kong Telecom from US networks.

NOTABLE ASIA-PAC HEADLINES

- BoJ, PBoC and BoK governors held a tripartite meeting on October 15th in Washington, which BoJ Governor Ueda chaired, while they exchanged views on recent economic and financial developments.

- BoJ's Tamura said the BoJ should push rates closer towards levels deemed neutral and the growth rate of Japan's economy is likely to rise, with overseas economies returning to a moderate growth path. Tamura said don't need to raise rates sharply or tighten monetary policy now, given both upside and downside risks, but stated that there is a strong possibility that the slowdown in overseas economies will not be as significant as initially expected. Furthermore, he said given upside price risks, the BoJ should push up rates closer toward neutral to avoid being forced to hike rates sharply in the future. BoJ's Tamura declined to comment when asked whether to propose a rate hike at the October meeting, while he stated he believes it is necessary to adjust the degree of monetary easing to make rate closer to neutral rate. He added a weak JPY could accelerate upward price pressures.

- RBA Assistant Governor Kent noted signs that financial conditions are less restrictive after past rate cuts and said the cash rate is within the range of neutral estimates, but the range is very wide and uncertain, while he added that neutral rates are not a suitable guide to the near-term path of monetary policy.

- Japan's Innovations Party, Fujita says another round of discussion with the LDP will take place this Friday. Both parties have found a lot of common ground. Not certain that a deal will be ultimately reached.

DATA RECAP

- Japanese Machinery Orders MM (Aug) -0.9% vs. Exp. 0.4% (Prev. -4.6%)

- Japanese Machinery Orders YY (Aug) 1.6% vs. Exp. 4.8% (Prev. 4.9%)

- Australian Employment (Sep) 14.9k vs. Exp. 20.0k (Prev. -5.4k)

- Australian Unemployment Rate (Sep) 4.5% vs. Exp. 4.3% (Prev. 4.2%, Rev. 4.3%)