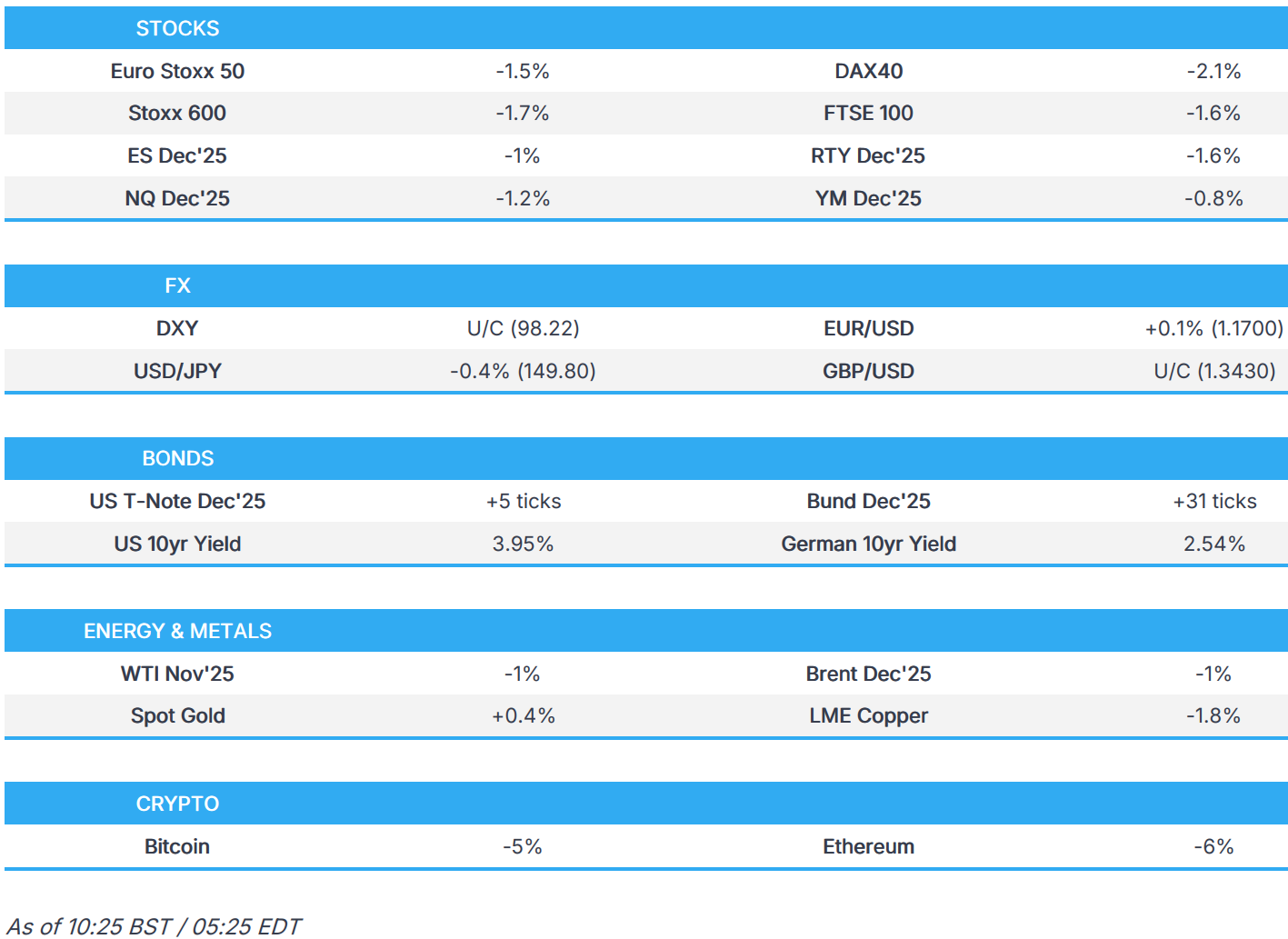

US Market Open: Sentiment tumbles amidst US regional banking fears; RTY -1.6%

17 Oct 2025, 11:21 by Newsquawk Desk

- European and US equity futures are lower across the board, with the US regional banking fears weighing on sentiment; KRE -2% in pre-market trade.

- DXY is a little lower; typical havens (JPY, CHF) benefit from the risk-tone whilst the Aussie lags.

- Global fixed paper driven higher as traders remain wary on US regional banks.

- Crude continues Thursday’s selling, XAU choppy amid debt concerns.

- Looking ahead, Speakers including BoE’s Pill, Greene & Breeden, Fed’s Musalem, ECB's Nagel, Earnings from Ally Financial, SLB, American Express, State Street. Suspended Releases: US Building Permits/Housing Starts (Sep), Industrial Production (Sep).

TARIFFS/TRADE

- US State Department said Secretary of State Rubio and USTR Greer met with Brazil's Foreign Affairs Minister Vieira and had very positive talks regarding trade and ongoing bilateral issues, while they agreed to work together to schedule a meeting between President Trump and President Lula at the earliest possible occasion.

- US State Department said China's sanctions against Hanwha Ocean's (042660 KS) US-linked units are attempts to undermine US-South Korea cooperation and coerce South Korea.

- South Korean Finance Minister said it's 'uncertain' whether US President Trump will accept Korea's position against an 'upfront' USD 350bln payment related to their tariff/trade agreement, according to Yonhap.

EUROPEAN TRADE

EQUITIES

- European equities (STOXX 600 -1.8%) opened entirely in the red and dipped soon after the cash open, before finding a base where indices currently reside. The ongoing US regional banking fears remain at the forefront of traders' minds.

- European sectors are all negative. Banks/Financial Services unsurprisingly underperform, given the aforementioned banking fears. Elsewhere, Defence names across Europe have been pressured after the White House suggested that the latest Trump-Putin conversation was good and constructive.

- US equity futures (ES -1% NQ -1.2% RTY -1.6%) continue to extend the losses seen in the prior session, in-fitting with the risk tone. It is worth highlighting that the Regional Banking ETF (KRE) is lower by roughly 2% in the US pre-market.

- Click for the sessions European pre-market equity newsflow

- Click for the additional news

- Click for a detailed summary

FX

- DXY is net lower with the USD showing a divergent performance vs. peers on account of the risk-averse moves triggered by the recent selling in regional US banks. As such, the USD is weaker vs. havens (CHF, JPY) and bid vs. risk-sensitive currencies (AUD, NZD). The question for markets is whether the selling pressure in Zions and Western Alliance Bancorp (on account of exposure to fraudulent loans) is a deep systemic issue or something that will have limited contagion, as per the SVB debacle in 2023. DXY hit a new low for the week at 98.02 (coincides with the 50DMA), before bouncing off the lows.

- EUR is up against the USD for a fourth session in a row on account of an aversion by the market to bid up the USD amid regional banking concerns and markets continuing to find solace in the developments in French politics this week. On the latter, with Lecornu having survived two no-confidence motions and odds of legislative elections by year-end receding to just 27% (vs. 50%+ earlier in the week), attention now turns to the subsequent debate and potential passage of the budget, as well as Moody's rating on France next Friday. Elsewhere, headline EZ HICP Finals were unrevised, and had limited impact on the Single-Currency. EUR/USD has eclipsed its 50DMA at 1.1692.

- JPY outperforms major peers on account of a haven bid alongside the selling in global equity markets. Subsequently, USD/JPY has slipped below the 150 mark for the first time since October 6th. From a domestic viewpoint, focus remains on the political landscape with the JIP co-head announcing "big progress" in discussions with the LDP party and stating that they will be entering the stage of finalising details. On the BoJ, comments from Governor Ueda over the past 24 hours have reiterated the Bank's view of raising rates if its economic forecasts are realised, whilst Assistant Governor Shimzu has noted that the Bank must tread carefully. USD/JPY has delved as low as 149.39 with the next downside target ahead of the 149 mark coming via the 6th October low at 149.04.

- The recovery in the pound vs. the dollar has faltered today on account of the broader risk tone. From a macro perspective, this week in the UK has been characterised by soft labour market metrics and sluggish growth with the former increasingly acknowledged by several BoE speakers this week. Next week also sees flash PMI and retail sales metrics, which are likely to be hampered by ongoing budget-related angst. Today's speaker slate includes BoE’s Pill, Greene & Breeden.

- Antipodeans are both lower vs. the USD on account of the risk-averse tone in the market with AUD continuing to lag its antipodean peer following yesterday's soft jobs metrics from Australia.

- PBoC set USD/CNY mid-point at 7.0949 vs exp. 7.1154 (Prev. 7.0968)

- Click for a detailed summary

- Click for NY OpEx Details

FIXED INCOME

- USTs are firmer, as the US regional banking backdrop remains at the forefront of market focus for today. USTs peaked at 114-02 early doors, sending the US 10yr yield below the 4% mark for the first time since April; for reference, the April low was 3.86%. Since, the benchmark has pulled back to just below the 114-00 mark but holds onto gains of c. 5 ticks on the session and around 25 on the week, as things stand.

- Bunds are bid, given the general risk tone and FTQ seen after the US regional banking flareup on Thursday. Bunds peaked at 130.59 early doors before seeing a relatively sharp pullback as the European morning got underway, to a 130.22 low; but, still firmer on the session. European specific newsflow of note for fixed income a little light, aside from largely unrevised headline HICP metrics. The docket ahead features ECB’s Nagel and Rehn.

- Gilts gapped higher by 46 ticks, acknowledging the upside seen in peers on Thursday after the Gilt close as the US regional banking situation reverberated to the broader risk tone. Opened at 93.10 and extended to a 93.17 peak, notching a new high for the week and taking the benchmark to its highest since July when Gilts briefly traded above 93.50. Amidst this, the UK 10yr yield found itself under pressure and to a 4.45% low; the lowest since July when 4.41% printed. Ahead, we have a handful of BoE speakers due. On the hawkish side, Pill and Greene feature and are followed by the usually more neutral Breeden.

- Click for a detailed summary

COMMODITIES

- WTI and Brent are pressured today amidst the ongoing risk-off sentiment, and as traders digest the latest constructive commentary surrounding the latest Trump-Putin call. The White House described that call as "good and productive" and have agreed to convene a meeting of high-level staff next week. WTI and Brent are currently trading towards the lower end of their respective USD 56.73-57.56/bbl and USD 60.30-61.11/bbl range.

- Spot gold continues to advance and remains at top end of the day's range (USD 4,279.10-4,380.79/oz). Price action this morning fairly rangebound, but ultimately at elevated levels given the risk-off environment.

- Base metals are lower across the board, pressured by the risk tone; 3M LME Copper currently off by around 1.6% in a USD 10,461.6-10,637.5/t range.

- Click for a detailed summary

NOTABLE DATA RECAP

- EU HICP Final YY (Sep) 2.2% vs. Exp. 2.2% (Prev. 2.2%); HICP Final MM (Sep) 0.1% vs. Exp. 0.1% (Prev. 0.1%)

- Swedish Unemployment Rate (Sep) 8.3% (Prev. 8.4%)

NOTABLE EUROPEAN HEADLINES

- BoE's Mann said the UK labour market is loosening but not falling off a cliff, while she added that the UK yield curve now provides a more appropriate financial condition for the UK economy.

- ECB's Scicluna said the ECB must not rush further interest rate action, because the effects of higher US tariffs on prices aren't yet clear, according to Bloomberg.

NOTABLE US HEADLINES

- Fed Governor Miran said the downside of tariffs has been nowhere near what people predicted and that tariffs have had no material signs of growth drag or inflation spike, while he doesn't think the cost of tariffs will be passed onto consumers.

- Fed's Kashkari (2026 voter) said it is too soon to know the effect of tariffs on inflation and the impact of tariffs is taking longer to be felt than had guessed, while he expects services inflation to trend down and it is possible that goods inflation could spill over. Furthermore, he said the job market is slowing down and it is challenging to read signals without core government data because of the shutdown, as well as noted that most folks say they are still concerned about inflation.

- The Trump administration's slashing of the federal workforce amid the government shutdown is threatening AI work at the Commerce Department, according to Axios, citing sources close to the agency.

- US Senator Majority Leader Thune said the Senate is expected to vote next week on a bill to pay federal workers who have been forced to work without pay which would include the military, according to Punchbowl.

- US nears tariff relief for auto industry after lobbying push and is to make an announcement as soon as Friday, according to Bloomberg.

- Punchbowl, on US Obamacare credit extension, writes "it's true" that there are House Republicans who want to extend the credits; however, House Republican leadership does not want to, and their view is "hardening as the shutdown drags on"

GEOPOLITICS

MIDDLE EAST

- Hamas said the return of Israeli hostages' bodies may take time as some were buried in tunnels destroyed by Israel and others remain under rubble, while the retrieval requires equipment to remove rubble, which is currently unavailable due to Israel's entry ban on such tools. Furthermore, it stated that it remains committed to the Gaza agreement and is keen to hand over all remaining hostages' bodies.

- "Israeli Foreign Minister: Israel is committed to Trump's plan, but Hamas is violating the agreement by holding the remains of 19 of our dead hostages", according to Sky News Arabia

RUSSIA-UKRAINE

- US President Trump said regarding Russian President Putin and Ukrainian President Zelensky, that they might do separate meetings, while he will probably meet Putin over the next two weeks. Trump commented that Tomahawks are also needed for the US, and he responded that he will speak to Senate Majority Leader Thune after House Speaker Johnson, about the Putin call and make the right determination, when asked about Russian sanctions.

CRYPTO

- Bitcoin is on the backfoot as risk assets take a beating; Ethereum is underperforming down to USD 3.7k.

- Binance are among the crypto firms hit by French money-laundering checks, via Bloomberg.

APAC TRADE

- APAC stocks were predominantly lower as the region followed suit to the losses on Wall Street, where risk sentiment took a hit as regional bank concerns were reignited following loan fraud disclosures by Western Alliance and Zions Bancorp.

- ASX 200 was led lower by underperformance in financials, energy and tech, while gold miners were boosted by the record highs in the precious metal.

- Nikkei 225 retreated amid a firmer currency and as banking stocks suffered in sympathy with US counterparts, while uncertainty lingered ahead of next Tuesday's PM vote with the Japanese Innovation Party noting a 50-50 chance of a coalition with the LDP.

- Hang Seng and Shanghai Comp conformed to the downbeat mood amid US-China frictions, with both sides blaming each other for the tensions.

NOTABLE ASIA-PAC HEADLINES

- Japan's LDP and CDP agreed to hold a vote to decide Japan's next PM on October 21st, while it was also reported that Japan Innovation Party co-leader Yoshimura said the chance of a coalition with the LDP is 50-50.

- Japan's Ishin Party (Innovation Party) Co-head Fujita announces big progress with the LDP following talks; will enter the stage of finalising details, final discussions are very delicate.

- Japan's Komeito party is reportedly arranging not to vote for the opposition PM candidate, according to Kyodo.

- BoJ's Uchida says Japan's economy is recovering moderately, although there are some weak signs. The BoJ will continue to raise interest rate if prices move in line with our forecast.

DATA RECAP

- Singapore Non-Oil Exports MM (Sep) 13.0% vs Exp. 9.0% (Prev. -8.9%)

- Singapore Non-Oil Exports YY (Sep) 6.9% vs Exp. -2.1% (Prev. -11.3%)