Europe Market Open: US-Japan sign agreement for minerals and rare earths; European futures lower following tailwind from APAC

28 Oct 2025, 07:17 by Newsquawk Desk

- APAC stocks failed to sustain the momentum from the record highs on Wall St and were mostly subdued.

- US President Trump and Japanese PM Takaichi signed an agreement on the US-Japan alliance and framework for securing the supply of critical minerals and rare earths.

- European equity futures indicate a lower cash market open with Euro Stoxx 50 future down 0.2% after the cash market closed with gains of 0.6% on Monday.

- DXY is net negative amid gains in the JPY with USD/JPY slipping below the 152 mark post-Trump and Takaichi meeting.

- Global fixed income markets are broadly firmer. Crude has struggled for direction following the prior day's choppy performance.

- Looking ahead, highlights include German GfK (Nov), Richmond Fed (Oct), CaseShiller Home Prices (Aug), Consumer Confidence (Oct), ECB SCE (Sept), RBNZ's Richardson, Supply from Italy, UK, Germany & US.

- Earnings from Visa, Electronic Arts, PPG Industries, UnitedHealth, SoFi, PayPal, UPS, DR Horton, VF Corp, HSBC, BNP Paribas, Novartis, Logitech, Iberdrola & ASM International.

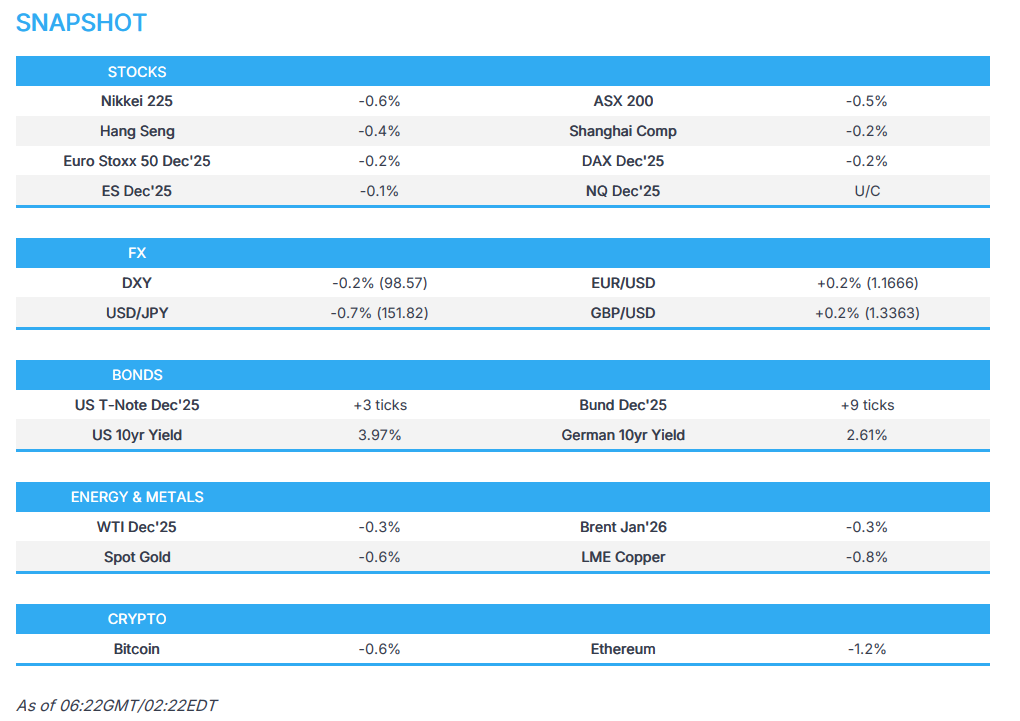

SNAPSHOT

US TRADE

EQUITIES

- US stocks were firmer and buoyed by the risk-on sentiment to start the week amid reports that the US and China agreed on a framework for a trade deal ahead of the Trump/Xi meeting later this week. Sectors were predominantly green with Communications leading the gains, followed by Tech and Discretionary, while Consumer Staples and Materials were the only sectors in the red. The stock-specific highlight was arguably Qualcomm (QCOM), which surged after announcing the launch of Qualcomm AI200 and AI250 chip-based accelerator cards and racks for data centres. As a result of the heightened risk appetite, spot gold was pressured and fell beneath USD 4k/oz, while the crude complex was initially bid, but later sold off to settle in the red.

- SPX +1.23% at 6,875, NDX +1.83% at 25,822, DJI +0.71% at 47,545, RUT +0.28% at 2,520.

- Click here for a detailed summary.

TARIFFS/TRADE

- US President Trump and Japanese PM Takaichi signed an agreement on the US-Japan alliance and framework for securing the supply of critical minerals and rare earths. White House said that the US and Japan plan to use economic policy tools and coordinated investment to accelerate the development of diversified, liquid, and fair markets for critical minerals and rare earths. Furthermore, within six months of the framework’s date, Japan and the US intend to take measures to support projects that generate end products for delivery to buyers in the US, Japan, and like-minded nations, while they will work to secure their critical minerals and rare earths supply chains by addressing non-market policies and unfair trade practices.

- Japanese senior government official said Japan and the US governments are preparing to release a fact sheet that includes potential investment projects in the US, while the fact sheet will include power generation and automobile-related products as potential investment projects and is expected to include company names such as Mitsubishi Heavy Industries.

- Japan is “very close” to opening its market to Brazilian beef, according to Brazil’s agriculture minister, in a move that would be a further blow to US exports, according to Bloomberg.

- China and ASEAN signed a free trade area 3.0 upgrade protocol, according to Xinhua.

- Ontario Premier Ford declined to apologise for sponsoring an anti-tariff television commercial that US President Trump used as a reason to terminate high-stakes trade talks with Canada, according to Bloomberg.

- UK is seeking a ‘steel club’ with the US and the EU to tackle Chinese oversupply, according to FT, while Britain’s Trade Minister said an alliance is a natural response to the global glut of metal, although talks had not yet reached a stage of a written proposal.

APAC TRADE

EQUITIES

- APAC stocks failed to sustain the momentum from the record highs on Wall St and were mostly subdued amid some profit taking and positioning ahead of this week's upcoming risk events.

- ASX 200 retreated in the absence of major catalysts and was dragged lower by weakness in healthcare, tech and miners.

- Nikkei 225 pulled back from all-time highs amid a firmer currency and despite US President Trump's visit to Japan, where he met with PM Takaichi and signed an agreement on US-Japan alliance and securing supply of critical minerals and rare earths.

- Hang Seng and Shanghai Comp were choppy ahead of the major risk events later in the week including the central bank decisions and the Trump-Xi meeting, while participants also reflected on recent comments from PBoC Governor Pan that they will resume government bond purchases and sales in the open market, as well as continue to maintain a supportive monetary policy stance and implement a properly loose monetary policy.

- US equity futures (ES U/C, NQ U/C) traded rangebound and took a breather following the prior day's record highs on Wall St.

- European equity futures indicate a lower cash market open with Euro Stoxx 50 future down 0.2% after the cash market closed with gains of 0.6% on Monday.

FX

- DXY mildly softened in rangebound trade with little fresh catalysts for the dollar ahead of central bank rate decisions later this week, including from the FOMC on Wednesday, while newsflow stateside remained sparse with President Trump currently in Asia, although Treasury Secretary Bessent recently named the five candidates in the running to be the next Fed chair.

- EUR/USD eked slight gains, albeit with upside limited amid a lack of drivers and with the ECB widely anticipated to stand pat at its meeting on Thursday.

- GBP/USD breached through yesterday's resistance, although gains were capped amid a report that the UK OBR is expected to cut its trend productivity growth forecast by about 0.3%, which is said to threaten a GBP 20bln hit to UK public finances.

- USD/JPY continued its pullback and dipped beneath the 153.00 level amid the cautious mood across the Asia-Pac region and the readout from the Trump-Takaichi meeting.

- Antipodeans remained afloat and held on to the prior marginal gains in uneventful trade amid a light calendar.

- PBoC set USD/CNY mid-point at 7.0856 vs exp. 7.1029 (Prev. 7.0881)

FIXED INCOME

- 10yr UST futures marginally edged higher as sentiment in Asia turned cautious, but with upside capped by supply.

- Bund futures rebounded from Monday's trough but remained beneath the 130.00 level with the recovery limited ahead of German GfK data and issuances including EUR 4.0bln of Bobls later, followed by EUR 4.5bln of Bunds tomorrow.

- 10yr JGB futures gradually edged higher alongside the subdued risk appetite and in the absence of any data, while participants also await the BoJ policy decision later in the week, in which the central bank is expected to refrain from any adjustments, although focus will also be on any clues for when the central bank will resume hiking rates.

COMMODITIES

- Crude futures struggled for direction following the prior day's choppy performance, while reports noted that OPEC+ is leaning towards another modest production increase at its meeting later this week.

- OPEC+ base case scenario is a small hike for now, according to Bloomberg citing delegates, while the group is so far expected to focus on a third monthly increase of 137k BPD.

- IEA chief Birol said a significant chapter for LNG is starting soon and that 300bcm of LNG is to hit markets in the next five years. Birol said that, absent major geopolitical tensions, oil and gas prices are expected to be lower, while he added that sanctions could push oil prices upward, but the effect is likely to be limited due to surplus capacity and slowing demand.

- Venezuela's President Maduro announces immediate suspension of energy agreements with Trinidad and Tobago.

- Spot gold attempted to nurse some of the prior day's losses but ultimately failed to sustain the USD 4,000/oz status.

- Copper futures ultimately declined amid the cautious mood in Asia ahead of this week's major risk events.

CRYPTO

- Bitcoin traded indecisively on both sides of the USD 114k level and within relatively contained parameters.

NOTABLE ASIA-PAC HEADLINES

- Japanese PM Takaichi thanked US President Trump for his enduring friendship with late PM Shinzo Abe, while she added that President Trump contributed to Asia's peace, including the Thai-Cambodia deal, and stated that the Middle East deal was an unprecedented historical achievement. Takaichi said she highly values Trump's commitment to world peace and stability, as well as expressed readiness to promote further collaboration with the US to achieve a free and open Indo-Pacific. Furthermore, Takaichi said she will continue to strive as Japan’s leader to strengthen the nation’s power, including defence capabilities, and wants to realise a new golden age of the Japan-US alliance with President Trump.

- US President Trump said former PM Abe was a great friend of his and noted that the US has received Japan's orders of military equipment, which Trump appreciates, while Trump said they are signing a deal and that the US-Japan trade deal is a very fair deal. Furthermore, Trump said this will be a relationship that will be stronger than ever before and that the US is Japan's ally at the strongest level.

- US Treasury Secretary Bessent highlighted in a meeting with Japanese Finance Minister Katayama the important role of sound monetary policy formulation and communication in anchoring inflation expectations and preventing excessive exchange rate volatility. It was also stated that conditions are substantially different twelve years after the introduction of Abenomics, while Bessent was glad to hear Katayama’s perspective on Japanese fiscal measures under consideration and expressed eagerness to learn more as the full package is developed to better understand its potential impact.

- Japanese Economy Minister Kiuchi said foreign exchange moves are determined by various factors and it is important for foreign exchange moves to reflect fundamentals and remain stable, while he added it is important to avoid rapid, short-term fluctuations in foreign exchange moves.

- Japan and South Korea are coordinating to hold the first summit meeting between PM Takaichi and South Korean President Lee on October 30th on the sidelines of the APEC summit meeting in South Korea, according to Asahi.

DATA RECAP

- South Korean GDP QQ (Q3 A) 1.2% vs. Exp. 0.9% (Prev. 0.7%)

- South Korean GDP YY (Q3 A) 1.7% vs. Exp. 1.5% (Prev. 0.6%)

GEOPOLITICS

MIDDLE EAST

- Palestinian TV reported that Israeli vehicles fired on the eastern areas of Gaza City, according to Sky News Arabia.

RUSSIA-UKRAINE

- Lukoil reportedly intends to sell its foreign assets after sanctions were imposed against the company, according to Interfax.

- US reportedly floated a six-month deadline for Berlin to sort out the ownership limbo affecting the German assets of Russian oil major Rosneft PJSC, allowing them to be temporarily exempted from US sanctions, according to Bloomberg sources.

OTHER

- US State Department senior official said the US expects Thailand will work with Cambodia to begin the release of 18 soldiers immediately, while the official added that US policy towards North Korea remains aimed at denuclearisation, and that US policy on Taiwan has not changed.

- North Korea said Foreign Minister Choe met with Russian President Putin and discussed many businesses to strengthen bilateral relations, while Choe and Russia's Foreign Minister Lavrov agreed on all points while holding strategic discussions on global issues. Furthermore, the North Korean side expressed support for Russian measures to remove the root of the Ukraine conflict, and the Russian side expressed support for North Korean efforts to protect its current position, security interests, and sovereign rights, according to KCNA.

EU/UK

NOTABLE HEADLINES

- UK OBR is expected to cut its trend productivity growth forecast by about 0.3%, according to FT citing sources, increasing the prospect of big tax rises, including income tax. It was noted that Chancellor Reeves faces a GBP 20bln hit to UK public finances from the productivity growth downgrade.

- UK is to stop disclosing identity of stock market short sellers, with the FCA overhauling regulations in a break from EU rules to be more in line with the US, according to FT.

DATA RECAP

- UK BRC Shop Price Index YY (Sep) 1.0% vs Exp. 1.6% (Prev. 1.4%)