Europe Market Open: All eyes on BoE announcement; European equity futures uneventful

06 Nov 2025, 07:12 by Newsquawk Desk

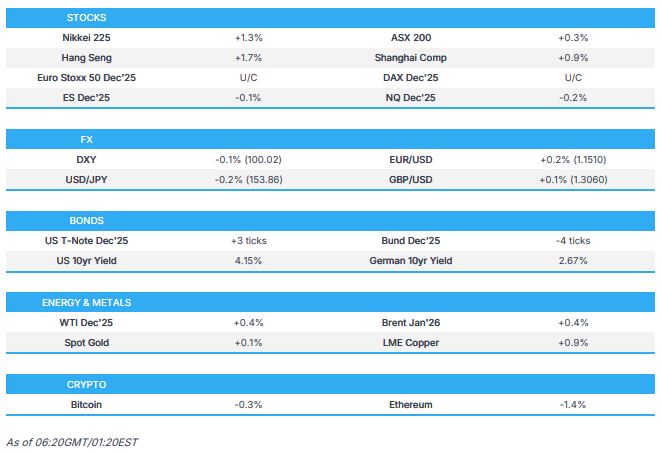

- APAC stocks were higher as the region took impetus from the rebound on Wall St, where all major indices gained amid dip buying.

- European equity futures indicate an uneventful cash market open with Euro Stoxx 50 futures relatively flat after the cash market closed with gains of 0.2% on Wednesday.

- DXY traded rangebound after having recently snapped a 5-day rally, despite firmer-than-expected ADP and ISM Services data, while catalysts were quiet overnight

- 10yr UST futures saw some slight reprieve after slumping yesterday; Bund futures languished near the prior day's lows.

- US President Trump is scheduled to make an announcement at 11:00EST/16:00GMT on Thursday.

- Looking ahead, highlights include German Industrial Production, EZ Retail Sales, Canadian Leading Index, US Chicago Fed Labour Market Indicators, US Challenger Layoffs, BoE, Banxico & Norges Bank Policy Announcements, Speakers including Fed’s Williams, Barr, Hammack, Waller, Paulson & Musalem, ECB’s Lane, Nagel, Schnabel & de Guindos, BoE’s Bailey, BoC's Macklem, Rogers & Kozicki, Supply from Spain & France

- Earnings from Continental, Commerzbank, AstraZeneca, Sainsbury’s, Airbnb, ConocoPhillips & Warner Bros.

SNAPSHOT

US TRADE

EQUITIES

- US stocks ended the day with notable gains after a downbeat start as initial AMD weakness post-earnings weighed with investors touting lofty valuations, but this soon pared. Sectors were mainly green with Communication Services and Consumer Discretionary sitting atop of the pile, with Consumer Staples, Tech, and Real Estate sitting in the red, albeit marginally. US data came via ADP and ISM Services, both of which came in hotter than anticipated, with both garnering a Dollar bid and pressuring on USTs.

- SPX +0.37% at 6,796, NDX +0.72% at 25,620, DJI +0.48% at 47,311, RUT +1.54% at 2,465.

- Click here for a detailed summary.

TARIFFS/TRADE

- China bought two cargoes of around 120,000 tons of US wheat for December shipment, according to traders cited by Reuters. It was also reported that the US Grains and Bioproducts Council Chairman said a US sorghum shipment was sent to China last week.

- Japanese PM Takaichi said Japan will consider specific ways for Japan and the US to advance cooperation in the development of rare earth mining in waters around Minamitori Island.

NOTABLE HEADLINES

- US President Trump said regarding the US shutdown, that it was a big factor in elections, while he does not think Democrats will act soon on the shutdown, and does not think it will be sorted soon. Trump reiterated the call to kill the filibuster and reopen the government immediately.

- US President Trump is scheduled to make an announcement at 11:00EST/16:00GMT on Thursday.

- US Department of Transportation announced it will start cutting flights by 4% on Friday which will rise to 10% next week if no shutdown deal is reached, while the FAA confirmed that flight cuts at 40 major airports will begin on Friday and warned it could take more actions after Friday if further air traffic issues emerge.

- Fed finalised new standards for grading large banks and said that the new large bank supervisory standards are substantially similar to changes proposed in July.

APAC TRADE

EQUITIES

- APAC stocks were higher as the region took impetus from the rebound on Wall St, where all major indices gained amid dip buying and following stronger-than-expected ADP and ISM Services data releases.

- ASX 200 eked mild gains amid strength in miners, but with the upside limited as the top-weighted financials sector lagged after Big Four bank NAB reported a decline in full-year profit.

- Nikkei 225 rebounded from the prior day's selling and briefly reclaimed the 51,000 level before paring some of its gains.

- Hang Seng and Shanghai Comp benefitted from the improving US-China trade ties after China’s Commerce Ministry suspended the unreliable entity list announced in April and adjusted its export control lists, while there were comments from US President Trump who reiterated that Chinese President Xi is a good friend.

- US equity futures were contained after a gradual pullback from yesterday's peak and amid light overnight catalysts.

- European equity futures indicate an uneventful cash market open with Euro Stoxx 50 futures relatively flat after the cash market closed with gains of 0.2% on Wednesday.

FX

- DXY traded rangebound after having recently snapped a 5-day rally, despite firmer-than-expected ADP and ISM Services data, while catalysts were quiet overnight with participants awaiting US Challenger job cuts data and a slew of Fed speakers on Thursday.

- EUR/USD extended the prior day's rebound and reclaimed the 1.1500 status, but with upside limited by a lack of drivers.

- GBP/USD remained afloat after partially nursing some of this week's losses ahead of today's BoE meeting.

- USD/JPY faded some of the prior day's advances and gave back the 154.00 status following an acceleration in wages.

- Antipodeans were rangebound in the absence of any tier-1 data releases and despite the positive risk appetite.

- PBoC set USD/CNY mid-point at 7.0865 vs exp. 7.1222 (Prev. 7.0901)

- Brazilian Central Bank maintained the Selic rate at 15.00%, as expected, with the decision unanimous. BCB evaluated that maintaining the interest rate at the current level for a very prolonged period is enough to ensure convergence of inflation to the target. Furthermore, it said that future monetary policy steps can be adjusted, and it will not hesitate to resume the rate hiking cycle if appropriate.

FIXED INCOME

- 10yr UST futures saw some slight reprieve after slumping yesterday in the aftermath of the firm ADP and ISM Services data, while prices were also not helped by the Quarterly Refunding Announcement, with the US Treasury beginning preliminary discussions on boosting auction sizes.

- Bund futures languished near the prior day's lows after its recent slide to briefly beneath the 129.00 level, and as attention turns to German Industrial Production data scheduled today.

- 10yr JGB futures partially clawed back some of their opening losses as participants digested the labour cash earnings data, which accelerated to 1.9% from 1.5%, as expected.

COMMODITIES

- Crude futures nursed some losses after declining yesterday in a choppy fashion, but with the rebound limited following this week's larger-than-expected build in weekly crude stockpiles and with Saudi Arabia lowering OSPs to Asia and US.

- Saudi Arabia set the December Light Crude OSP to Asia to + USD 1.00/bbl vs Oman/Dubai average (prev. + USD 2.20), to Europe at + USD 1.35/bbl vs ICE Brent (prev. +1.35), and to US at + USD 3.20/bbl vs ASCI (prev. + USD 3.70).

- Poland is in talks to import more US LNG to supply Ukraine and Slovakia, according to Reuters citing sources familiar with negotiations.

- Spot gold marginally extended its mid-week recovery but remained beneath the psychologically key USD 4,000/oz level.

- Copper futures gradually edged higher with prices underpinned amid the constructive risk appetite.

CRYPTO

- Bitcoin traded indecisively and failed to sustain a brief reclaim of the USD 104k level.

NOTABLE ASIA-PAC HEADLINES

- Japanese PM Takaichi looks to finalise an economic stimulus package to address inflation by late November and pass a supplementary budget to fund it, with some in the government eyeing a cost of over JPY 10tln, according to Nikkei.

- Japan Innovation Party co-leader Fujita said an early BoJ rate hike may give a mixed signal to businesses, while he added it is not a time for BoJ moves that have a big impact and they will not raise taxes to fund an earlier defence budget jump.

- One of Japan's largest labour unions, UA Zensen, is reportedly planning to push for a 6% wage hike for regular workers in next year's talks, according to Bloomberg.

- RBNZ Governor Hawkesby said he doesn’t think they are out of the worst on global trade tensions, while he added the labour market has deteriorated, which is something they anticipated.

DATA RECAP

- Japanese Overall Lab Cash Earnings (Sep) 1.9% vs. Exp. 1.9% (Prev. 1.5%, Rev. 1.3%)

- Australian Balance on Goods (Sep) 3,938M vs. Exp. 4,000M (Prev. 1,825M)

- Australian Goods/Services Exports (Sep) 7.90% (Prev. -7.80%)

- Australian Goods/Services Imports (Sep) 1.10% (Prev. 3.20%)

GEOPOLITICS

MIDDLE EAST

- Turkey’s intelligence chief and Hamas delegations discussed steps to overcome ceasefire process problems, according to Reuters citing security sources.

RUSSIA-UKRAINE

- US informed Russia of a Minuteman missile launch, while it was separately reported that US President Trump said they will be working on a plan with China and Russia to denuclearise.

- Russia’s Kremlin said it hopes that the situation surrounding statements about the possibility of nuclear tests will not affect US-Russia relations, according to Interfax.

OTHER NEWS

- US President Trump warned the Nigerian government that they had better move fast to stop the killing of Christians.

- US President Trump recently expressed reservations to top aides about launching military action to oust Venezuelan President Maduro, fearing that strikes might not compel Maduro to step down, according to sources cited by WSJ.

EU/UK

NOTABLE HEADLINES

- UK Chancellor Reeves is set to spare UK banks from the budget tax raid, according to FT.