US Market Open: US Challenger Layoffs jumps 175.3% to a 7-month high, US equity futures modestly firmer/flat

06 Nov 2025, 11:43 by Newsquawk Desk

- Challenger October US Job Cuts jump 175.3% to a 7-month high at 153.074k (prev. 54.064k in September).

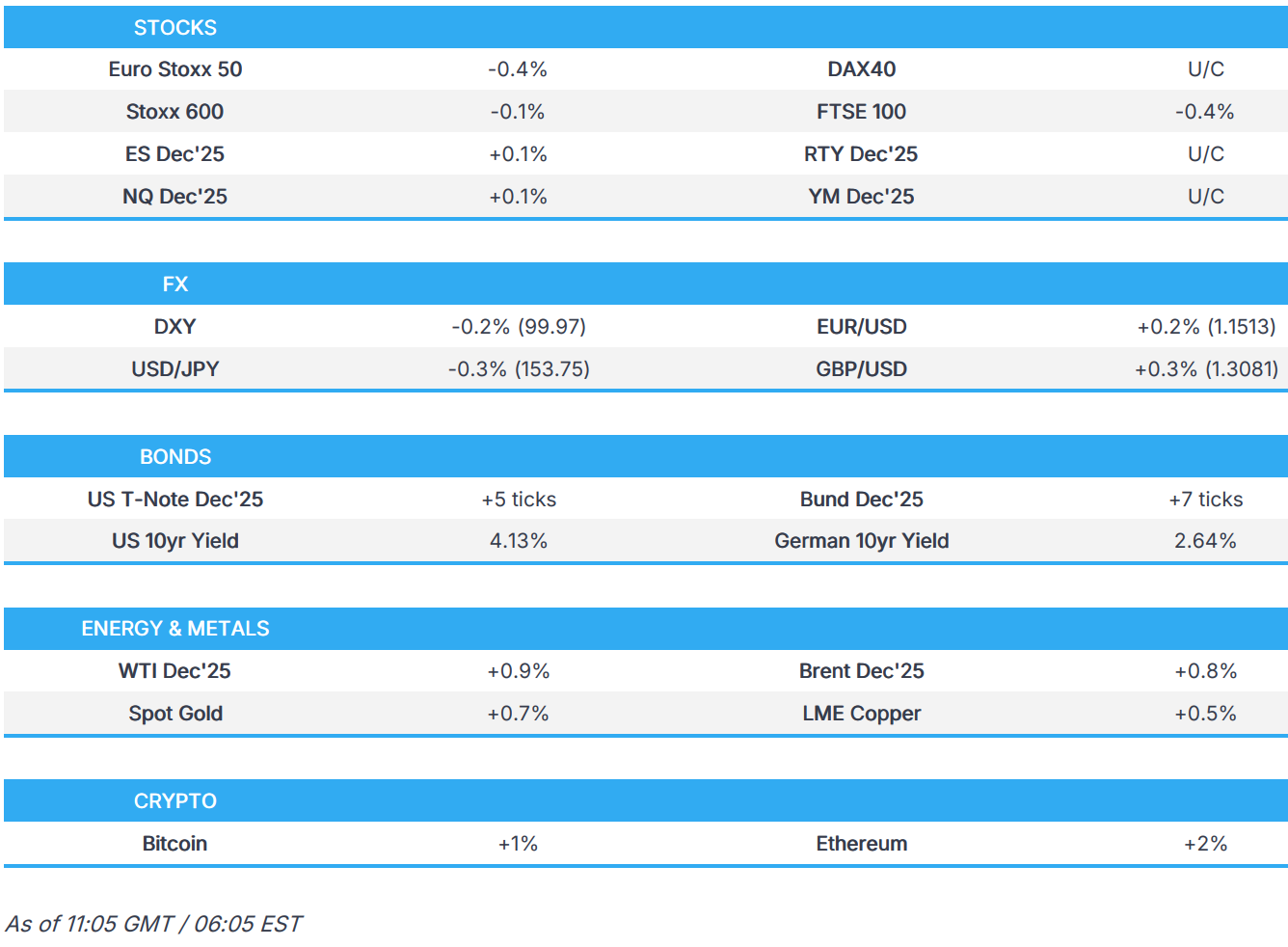

- European bourses are on the backfoot; US equity futures are modestly firmer/flat.

- Surprise early US Challenger release takes DXY sub-100; NOK gains on Norges, GBP awaits the BoE.

- Early Challenger lifted USTs to a session high, Gilts await the BoE.

- Crude benchmarks are higher despite Saudi oil price cuts and US inventory build; focus on Israel declaring the Egyptian border a closed military zone.

- Looking ahead, US Chicago Fed Labour Market Indicators, BoE & Banxico Policy Announcements, Speakers including Fed’s Williams, Barr, Hammack, Waller, Paulson & Musalem, ECB’s Lane, Nagel, BoE’s Bailey, BoC's Macklem, Rogers & Kozicki.

- Earnings from Airbnb, ConocoPhillips & Warner Bros.

TARIFFS/TRADE

- China bought two cargoes of around 120,000 tons of US wheat for December shipment, according to traders cited by Reuters. It was also reported that the US Grains and Bioproducts Council Chairman said a US sorghum shipment was sent to China last week.

- Japanese PM Takaichi said Japan will consider specific ways for Japan and the US to advance cooperation in the development of rare earth mining in waters around Minamitori Island.

- Chinese Commerce Ministry, on semiconductor flows, says China is committed to stability and security of global chip industry; will approve relevant export license applications of qualified Chinese exporters.

EUROPEAN TRADE

EQUITIES

- European bourses (STOXX 600 -0.2%) opened modestly lower and have traded with a negative bias throughout the European morning. Nothing really behind the sentiment today, but with traders mindful of looming US data and the BoE policy decision.

- European sectors are mixed; Banks take the top spot, joined closely by Retail and then Real Estate. To the downside, Construction & Materials lags, followed by Insurance. In terms of key movers; AstraZeneca (U/C, strong headline metrics), Maersk (-5.2%, strong Q3 metrics but faces "challenging" 2026), Commerzbank (-2.5%, boosts outlook but Net Income not so strong).

- US equity futures (ES +0.1%, NQ +0.1%, RTY U/C) are modestly firmer/flat, ahead of a slew of earnings. Main focus for the day was an early release of the US Challenger Layoffs, which jumped 175.3%, to a 7-month high at 153.074k (prev. 54.064k); a very modest uptick in futures was seen on the surprise release.

- Click for the sessions European pre-market equity newsflow

- Click for the additional news

- Click for a detailed summary

FX

- DXY is softer following rangebound trade, with a surprise early release of the US Challenger job cuts data prompted a cleaner breach back under 100.00, with the current intraday range between 99.89 - 100.11, and compared to yesterday's 100.06-100.36 range. Challenger October US Job Cuts jump 175.3% to a 7-month high at 153.074k (prev. 54.064k in September), according to Bloomberg. The release led to some upside in T-note futures and downside in the USD. On the tariff front, the US Supreme Court yesterday sharply questioned President Trump’s broad use of emergency powers to impose global tariffs, although this risk event is likely to be a slow burner, touted to end in Q1/Q2 2026, while ING's baseline is that tariffs will stay regardless of the ruling.

- EUR is slightly firmer against the USD, largely amid USD weakness, whilst little action was seen following a variety of comments from ECB's Schnabel and de Guindos, and largely pessimistic Construction PMI. EUR/USD resides in a 1.1490-1.1524 intraday range, with traders also cognizant of the converging 50 DMA (1.1670) and 100 DMA (1.1664).

- USD/JPY faded some of the prior day's advances and gave back the 154.00 status following an acceleration in wages, with USD weakness further weighing on the pair in early European hours. Aside from that, there is little else to mention for the JPY, with the pair comfortably tucked within yesterday's 152.96-154.35 range. Furthermore, one of Japan's largest labour unions, UA Zensen, is reportedly planning to push for a 6% wage hike for regular workers in next year's talks, according to Bloomberg.

- Sterling in focus as the clock ticks down to the Bank of England rate decision, minutes, and MPR are due at 12:00GMT/07:00EST, with the press conference at 12:30GMT/07:30EST. The MPC is expected to keep the Bank Rate at 4.0%, likely via a 6-3 vote, with focus on any signals regarding future easing. Despite softer-than-expected September inflation, elevated Y/Y CPI is expected to keep policymakers on hold, though three members may favour a cut. GBP/USD resides in a current 1.3042-1.3089 range after topping yesterday's peak at 1.3054.

- Diverging as the AUD/NZD cross rises above 1.1500 from a 1.1486 intraday low, with the AUD propped up by the base metals and the NZD hampered by cautious RBNZ commentary. Overnight, RBNZ Governor Hawkesby said he doesn’t think they are out of the worst on global trade tensions, while he added the labour market has deteriorated, which is something they anticipated. AUD/USD resides in a 0.6497-0.6518 range and is still some way off its 100 DMA (0.6539). NZD/USD is contained in a 0.5651-0.5669 range at the time of writing.

- EUR/NOK stopped just shy of its 100 DMA (11.7519) following the policy decision by Norges Bank, which opted to keep rates steady at 4.00% as expected. The Bank largely reiterated the statement from the prior meeting, suggesting that "no information has been received that indicates that the outlook for the Norwegian economy has changed significantly since the September policy meeting".

- PBoC set USD/CNY mid-point at 7.0865 vs exp. 7.1222 (Prev. 7.0901)

- Brazilian Central Bank maintained the Selic rate at 15.00%, as expected, with the decision unanimous. BCB evaluated that maintaining the interest rate at the current level for a very prolonged period is enough to ensure convergence of inflation to the target. Furthermore, it said that future monetary policy steps can be adjusted, and it will not hesitate to resume the rate hiking cycle if appropriate.

- Click for a detailed summary

- Click for NY OpEx Details

FIXED INCOME

- USTs are contained overnight as newsflow at the time was relatively limited and participants awaited a packed docket of Fed speak, texts are expected from Williams (voter) and Paulson (2026). Spent the morning near enough unchanged and just above the 112-10 session low. Thereafter, a bout of support was seen for havens generally around the European cash equity open; potential drivers include the Israeli comments on Egypt. Thereafter, the docket ahead was lightened by an early release of October’s Challenger job cuts. Printed at 153k (prev. 54k), to a seven-month high. This added to the modest strength seen in USTs and took them to a 112-18 high with gains of eight ticks at best. A print that has added a little bit of dovishness back into Fed pricing, though the odds of a 25bps cut in December remain at around 65% after losing the 70% handle yesterday following ADP and ISM Services. Markets see more job market indicators today via the Chicago Fed BLS unemployment forecast and the latest Revelio statistics.

- Bunds initial action was similar to that outlined above in USTs. Bunds spent the first part of the day holding near enough unchanged and just above the 129.03 opening mark. Thereafter, a pickup occurred around the European cash equity open before a 129.18 peak printed alongside Challenger; again, detailed in USTs above. Prior to this, an interesting speech from ECB’s Schnabel, where she said there are factors that are suggestive of tilting the structure of the ECB’s portfolio towards shorter-dated assets, but no move in Bunds at the time. Construction PMIs passed without impact this morning. Ahead, traders look to the referenced US events before remarks from ECB’s Nagel and Chief Economist Lane; particularly regarding the ECB’s portfolio, in light of Schnabel. No move to supply from Spain and France this morning. Overall, the auctions were well received with the long-dated French metric in particular garnering strength, a welcome sign amid the ongoing political turmoil.

- Gilts opened firmer by around 15 ticks and then quickly extended a handful more to a 93.33 high, a move that acknowledged the modest bullish action seen at the time, as outlined above. Price action for Gilts was a little more pronounced than that seen in peers, nothing too significant behind this but potentially a function of the relative underperformance seen in Gilts vs Bunds for much of Wednesday and/or positioning into the BoE. The BoE is expected to maintain the policy rate at 4.00%, though the decision will almost certainly be subject to dissent; expectations are broadly for either 7-2 or 6-3, however a split where Governor Bailey has to cast the deciding vote cannot be ruled out.

- Spain sells EUR 4.503bln vs exp. EUR 4-5bln 3.00% 2033, 1.85% 2035, 3.50% 2041 Bono & EUR 0.534bln vs exp. EUR 0.25-0.75bln 1.15% 2036 IL Bono.

- France sells EUR 10.98bln vs exp. EUR 9.5-11bln 3.50% 2035, 3.60% 2042 & 3.00% 2049 OAT.

- Click for a detailed summary

COMMODITIES

- Crude benchmarks have pared back on Wednesday’s losses following comments from Israeli Defense Minister Katz and sellers failing to extend through the lows of the 7-day range. After testing prior support lows, crude benchmarks sold off, reversing APAC gains, and troughed at USD 59.46/bbl and 63.37/bbl. However, this selloff was short-lived and benchmarks bid higher to a peak of 60.51/bbl and 64.34/bbl respectively. Saudi Arabia cut its December Light Crude OSP to Asia, in line with expectations. This confirms that the kingdom is comfortable with Brent prices holding between USD 60-65/bbl. Slight downticks were seen in crude benchmarks but move wasn’t sustained.

- Spot XAU has followed on from Wednesday’s gains as the yellow metal continues to consolidate following its 11% selloff from ATHs. XAU dipped to a trough of USD 3964/oz early in the APAC session but reversed higher and extended through Wednesday’s high at USD 3990/oz as the European session risk sentiment started off weak. Currently, the yellow metal is trading near session highs at USD 4017/oz. A surprising Challenger Layoff release had little impact on spot gold action.

- Base metals are trading mixed, with iron ore continuing to sell off as China steel industry heads into the low season while copper gains following risk-on tone during the APAC session. 3M LME Copper dipped to a low of USD 10.69k/t before driving higher as it followed the CME Copper bid back above USD 5/lb. 3M LME Copper peaked at USD 10.79k/t and remains in a c. USD 40/t band near session highs.

- Saudi Arabia set the December Light Crude OSP to Asia to + USD 1.00/bbl vs Oman/Dubai average (prev. + USD 2.20), to Europe at + USD 1.35/bbl vs ICE Brent (prev. +1.35), and to US at + USD 3.20/bbl vs ASCI (prev. + USD 3.70).

- Poland is in talks to import more US LNG to supply Ukraine and Slovakia, according to Reuters citing sources familiar with negotiations.

- Click for a detailed summary

NOTABLE DATA RECAP

- German Industrial Output MM (Sep) 1.3% vs. Exp. 3.0% (Prev. -4.3%)

- Swedish CPIF Flash YY (Oct) 3.1% vs. Exp. 2.9% (Prev. 3.10%); Modest SEK strength seen on the hotter-than-expected series.

- French Non-Farm Payrolls QQ (Q3) -0.3% (Prev. 0.2%)

- Spanish Ind Output Cal Adj YY (Sep) 1.7% (Prev. 3.4%, Rev. 3.3%)

- EU HCOB Construction PMI (Oct) 44.0 (Prev. 46)

- Italian HCOB Construction PMI (Oct) 50.7 (Prev. 49.8)

- French HCOB Construction PMI (Oct) 39.8 (Prev. 42.9)

- German HCOB Construction PMI (Oct) 42.8 (Prev. 46.2)

- UK S&P Global Construction PMI (Oct) 44.1 vs. Exp. 46.7 (Prev. 46.2)

- EU Retail Sales YY (Sep) 1.0% vs. Exp. 1.0% (Prev. 1.0%, Rev. 1.6%); MM (Sep) -0.1% vs. Exp. 0.2% (Prev. 0.1%, Rev. -0.1%)

NOTABLE EUROPEAN HEADLINES

- ECB's Schnabel says quantitative normalisation is proceeding smoothly, with strong liquidity positions of banks and abundant excess liquidity; on new structural portfolio, says factors suggest tilting the structure towards shorter-dated assets. "policy stance neutrality, the need to maintain policy space and considerations related to financial soundness are important factors that will guide the maturity of assets the ECB will buy under a new structural securities portfolio. These factors suggest tilting the structure towards shorter-dated assets."

- ECB's de Guindos states slight optimism on growth; adds that inflation news is positive. More optimistic on services inflation. Evolution of wages are fully aligned with projections. The level of uncertainty is huge. Comfortable with the current level of rates. Undershooting of inflation will be temporary. No discussion on modifying QT.

- Norges Bank keeps rates unchanged at 4.00%, as expected; Governor Bache says, "The job of overcoming inflation is not complete, and we are in no hurry to lower interest rates".

NOTABLE US HEADLINES

- Challenger October US Job Cuts jump 175.3% to a 7-month high at 153.074k (prev. 54.064k in September), according to Bloomberg.

- US President Trump said regarding the US shutdown, that it was a big factor in elections, while he does not think Democrats will act soon on the shutdown, and does not think it will be sorted soon. Trump reiterated the call to kill the filibuster and reopen the government immediately.

- US President Trump is scheduled to make an announcement at 11:00EST/16:00GMT on Thursday.

- US Department of Transportation announced it will start cutting flights by 4% on Friday which will rise to 10% next week if no shutdown deal is reached, while the FAA confirmed that flight cuts at 40 major airports will begin on Friday and warned it could take more actions after Friday if further air traffic issues emerge.

- Fed finalised new standards for grading large banks and said that the new large bank supervisory standards are substantially similar to changes proposed in July.

- Punchbowl writes, on the US shutdown, that "Trump and Hill Republicans are now in completely different places on the political impacts of this seemingly endless shutdown."

GEOPOLITICS

- "Israeli Defense Minister Yisrael Katz: Declaring war on smuggling operations through drones on our border with Egypt", according to Al Jazeera; "ordered the border area with Egypt to be turned into a closed military zone", via Iran International

OTHER NEWS

- US President Trump warned the Nigerian government that they had better move fast to stop the killing of Christians.

- US President Trump recently expressed reservations to top aides about launching military action to oust Venezuelan President Maduro, fearing that strikes might not compel Maduro to step down, according to sources cited by WSJ.

CRYPTO

- Bitcoin is a little firmer and trades just above USD 103k, whilst Ethereum outperforms a touch.

APAC TRADE

- APAC stocks were higher as the region took impetus from the rebound on Wall St, where all major indices gained amid dip buying and following stronger-than-expected ADP and ISM Services data releases.

- ASX 200 eked mild gains amid strength in miners, but with the upside limited as the top-weighted financials sector lagged after Big Four bank NAB reported a decline in full-year profit.

- Nikkei 225 rebounded from the prior day's selling and briefly reclaimed the 51,000 level before paring some of its gains.

- Hang Seng and Shanghai Comp benefitted from the improving US-China trade ties after China’s Commerce Ministry suspended the unreliable entity list announced in April and adjusted its export control lists, while there were comments from US President Trump who reiterated that Chinese President Xi is a good friend.

NOTABLE ASIA-PAC HEADLINES

- Japanese PM Takaichi looks to finalise an economic stimulus package to address inflation by late November and pass a supplementary budget to fund it, with some in the government eyeing a cost of over JPY 10tln, according to Nikkei.

- Japan Innovation Party co-leader Fujita said an early BoJ rate hike may give a mixed signal to businesses, while he added it is not a time for BoJ moves that have a big impact and they will not raise taxes to fund an earlier defence budget jump.

- One of Japan's largest labour unions, UA Zensen, is reportedly planning to push for a 6% wage hike for regular workers in next year's talks, according to Bloomberg.

DATA RECAP

- Japanese Overall Lab Cash Earnings (Sep) 1.9% vs. Exp. 1.9% (Prev. 1.5%, Rev. 1.3%)

- Australian Balance on Goods (Sep) 3,938M vs. Exp. 4,000M (Prev. 1,825M)

- Australian Goods/Services Exports (Sep) 7.90% (Prev. -7.80%)

- Australian Goods/Services Imports (Sep) 1.10% (Prev. 3.20%)