Europe Market Open: Trump signs government funding bill to end shutdown; European equity futures are positive

13 Nov 2025, 07:03 by Newsquawk Desk

- US President Trump signed the government funding bill and announced an end to the government shutdown after the House voted to approve the bill, while Trump said the government will resume normal operations and reiterated a call for money to be paid to people directly to buy healthcare.

- White House Press Secretary Leavitt said the October CPI and jobs data is likely to never be released, while it was separately reported that there was no official word from BLS on plans for October data.

- US officials flagged they will reduce tariffs on popular groceries, as pressure mounts to address the cost-of-living crisis, according to FT.

- APAC stocks followed suit to the mixed performance in the US, with little fresh catalysts as the government shutdown ended.

- European equity futures indicate a positive cash market open with Euro Stoxx 50 futures up 0.4% after the cash market closed with gains of 1.1% on Wednesday.

- Looking ahead, highlights include UK GDP (Sep/Q3), EZ Industrial Production (Sep), US Cleveland Fed (Oct), New Zealand Manufacturing PMI (Nov), IEA OMR, BoE Minutes of the Market Participants Group Meeting, Speakers including BoE’s Greene, Fed’s Daly, Kashkari, Musalem & Hammack, ECB’s Elderson, SNB’s Tschudin & Moser, Supply from Italy & US, Earnings from Zealand Pharma, B&M European, Burberry, Siemens, Sabadell, Applied Materials, Disney, JD com & Bilibili.

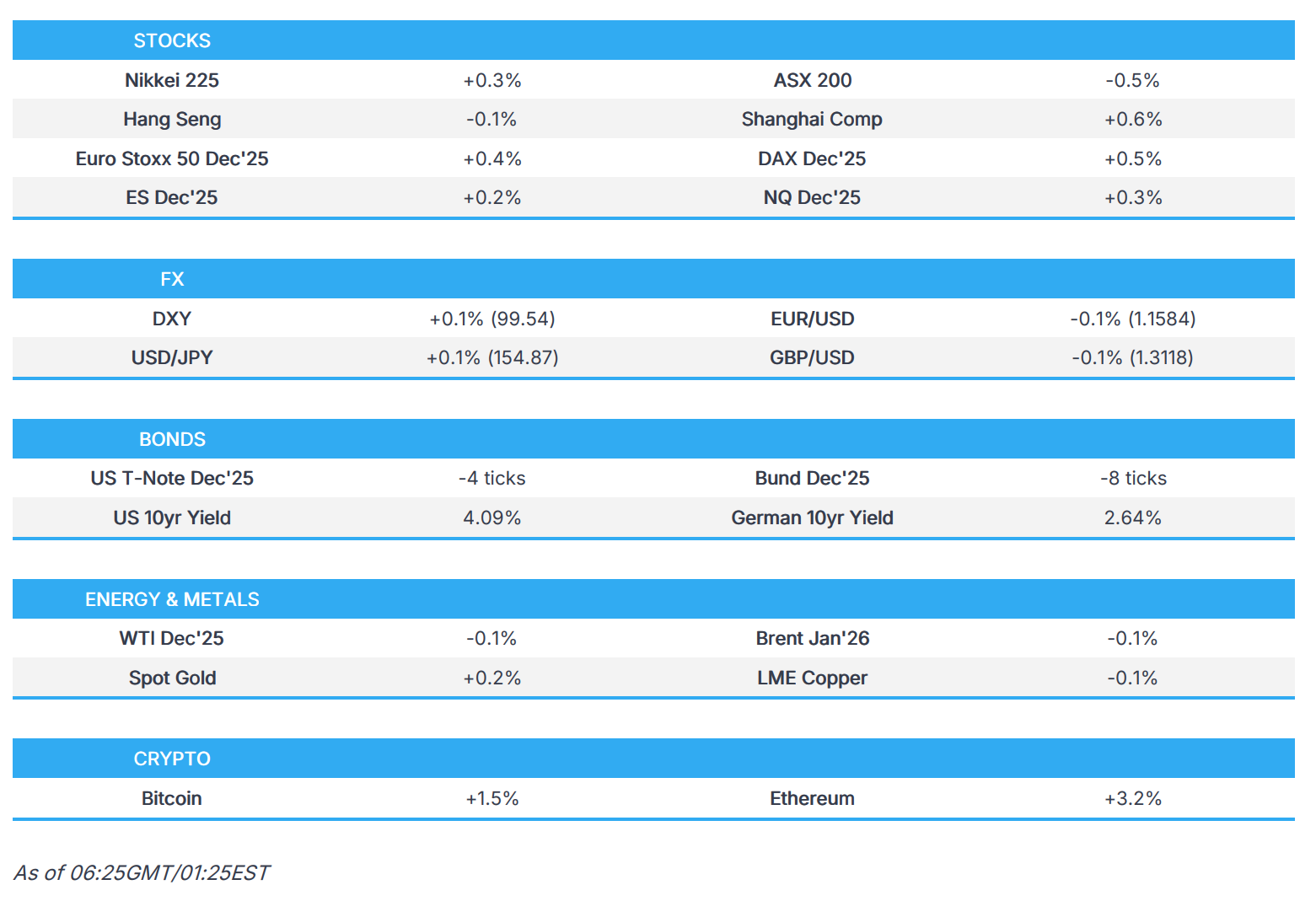

SNAPSHOT

US TRADE

EQUITIES

- US stocks were mixed with the SPX, NDX, and RUT closing little changed, but the DJI saw strong outperformance thanks to upside in heavyweights UnitedHealth (UNH) and Goldman Sachs (GS). Cisco (CSCO) also saw upside ahead of earnings. Breadth was more positive with the RSP rising while sectors were varied as Health Care, Financials and Materials outperformed, but Energy, Communication and Consumer Discretionary lagged. Tech was flat despite the upside in AMD (AMD) after its analyst day.

- SPX +0.08% at 6,852, NDX -0.06% at 25,517, DJI +0.68% at 48,255, RUT -0.26% at 2,452.

- Click here for a detailed summary.

TARIFFS/TRADE

- US officials flagged they will reduce tariffs on popular groceries, as pressure mounts to address the cost-of-living crisis, according to FT.

- FBI Director said China agreed on a plan to stop fentanyl precursors and agreed to control seven chemical substances, which are now banned.

- EU is set to propose a plan to the US that would implement the next phase of the trade agreement reached in the summer, according to Bloomberg citing people familiar with the matter.

- EU seeks to accelerate crackdown on cheap Chinese parcels, according to FT.

- India announced anti-dumping duties on some steel products from Vietnam.

NOTABLE HEADLINES

- US President Trump signed the government funding bill and announced an end to the government shutdown after the House voted to approve the bill, while Trump said the government will resume normal operations and reiterated a call for money to be paid to people directly to buy healthcare.

- US President Trump's administration froze flight cuts at 6% rather than hiking to 8% on Thursday, according to the US Department of Transportation.

- White House Press Secretary Leavitt said the October CPI and jobs data is likely to never be released, while it was separately reported that there was no official word from BLS on plans for October data. Furthermore, the White House later announced that the September BLS data will be released after the government reopening, but didn't mention a specific date.

- White House Economic Adviser Hassett said the government shutdown will impact this quarter's GDP and anticipates it to be between 1.5-2%, as well as noted that GDP for the year will be roughly 2% and that supply-side policies will allow growth without inflation. Hassett said he agreed with the last two Fed meetings that it was time to cut rates and noted the Fed is unlikely to cut 50bps, with the Fed more likely to do 25bps, while he added that he will do it if asked to be the Fed Chair.

- Fed Governor Miran (voter) said Fed policy is too restrictive and they should not take inflation data at face value, while he is in favour of using the Fed's balance sheet more judiciously than in the past.

- Fed's Collins (2025 voter) said it is likely appropriate to keep the policy rate on hold for some time and there is a relatively high bar for additional easing in the near term, while she is hesitant to ease policy further, absent notable labour-market deterioration and stated it is prudent to ensure inflation is durably on track to 2% before making any further policy rate cuts. Collins said further monetary support to activity runs the risk of slowing or stalling inflation's return to 2%, as well as noted that Fed policy is 'mildly restrictive' and that financial conditions are a tailwind for growth. Furthermore, she said dialling two notches down on rates made sense given risks and that elevated inflation warrants still mildly restrictive policy.

- Fed's Bostic (2027 voter) said that despite the shifts in the labour market, the clearer and urgent risk is still price stability. Bostic said labour market signals are not strong enough to warrant an aggressive monetary policy response vs. the risk of ongoing inflation pressures. Furthermore, he favours keeping the Fed Funds Rate steady until they see clear evidence of inflation moving towards the 2% target, and he views the current policy stance as 'marginally restrictive', while he noted that if conditions change, he is willing to alter his stance.

- NY Fed's Manager of SOMA portfolio Perli said there is ‘no reason why’ there can’t be sizable standing repo facility usage and that the standing repo facility should be used when needed. Perli added that stable repo market conditions are in everyone’s interest and that a standing repo facility works well and is an important market stabiliser, while he also commented that at some point the Fed will need to expand the balance sheet again.

- US Supreme Court to hear arguments on Trump bid to fire Fed Governor Lisa Cook on January 21st.

APAC TRADE

EQUITIES

- APAC stocks followed suit to the mixed performance in the US, with little fresh catalysts as the government shutdown ended.

- ASX 200 was pressured amid underperformance in the tech, real estate and energy sectors, while stronger-than-expected jobs data from Australia did little to inspire a turnaround.

- Nikkei 225 was choppy as participants reflected on recent earnings releases and firmer-than-expected PPI data.

- Hang Seng and Shanghai Comp were mixed with strength in pharmaceuticals offset by weakness in energy and tech, while Chinese press noted that brokerage firms expect China's A-share market to continue to gain in 2026, with earnings growth anticipated to be around 4.7% next year.

- US equity futures kept afloat with little fresh macro catalysts aside from the widely expected government reopening.

- European equity futures indicate a positive cash market open with Euro Stoxx 50 futures up 0.4% after the cash market closed with gains of 1.1% on Wednesday.

FX

- DXY remained flat amid light fresh catalysts and despite the House passing the funding bill to reopen the government, which President Trump then signed to end the government shutdown. There were several comments from Fed officials, including Bostic, who is set to retire in February 2026, and kept to a hawkish stance as he argued that the labour market signals are not strong enough to warrant an aggressive monetary policy response against the risk of ongoing inflation pressures, while Collins said it is likely appropriate to keep the policy rate on hold for some time and noted a relatively high bar for additional easing in the near term.

- EUR/USD was indecisive after stalling just shy of the 1.1600 handle and failed to benefit from the somewhat recent hawkish-leaning ECB rhetoric.

- GBP/USD lacked demand but is off this week's worst levels which had coincided with political uncertainty, although some of the concerns were alleviated after the UK Health Secretary pushed back on reports of a plot to oust the PM, while participants now await the incoming UK GDP data.

- USD/JPY traded indecisively overnight and pulled back after hitting resistance around the 155.00 level amid the tentative mood in Japan.

- Antipodeans were mixed with AUD/USD the outperformer following stronger-than-expected jobs data and a drop in the Unemployment Rate.

- PBoC set USD/CNY mid-point at 7.0865 vs exp. 7.1156 (Prev. 7.0833).

- BoC Minutes said the Governing Council Members had a range of views about the timing of the cut, but arguments for a move in October were considered more important. Members felt indicators of underlying inflation would give signals about the trend of total inflation, while they expressed concern that weakness in the labour force could persist and broaden.

FIXED INCOME

- 10yr UST futures mildly pulled back from yesterday's peak following softer demand at the 10yr auction stateside.

- Bund futures lingered near a weekly high following the prior day's rebound and with little fresh catalysts.

- 10yr JGB futures traded uneventfully with demand contained after firmer-than-expected Japanese PPI data and following the latest 5yr JGB auction, which resulted in slightly lower than previous bid-to-cover and accepted prices.

COMMODITIES

- Crude futures were lacklustre after tumbling yesterday amid oversupply concerns and positive Ukraine/Russia rhetoric, while the latest private sector inventory data was mixed and provided little to inspire a rebound.

- US Private Inventory Data (bbls): Crude +1.3mln (exp. +2.0mln), Distillate +0.9mln (exp. -2.0mln), Gasoline -1.4mln (exp. -1.9mln), Cushing -0.0mln

- US DoE announced that contracts were awarded for the acquisition of approximately 1mln barrels of crude for the SPR.

- EIA STEO stated world oil supply and demand were revised marginally higher for 2025 and 2026, with world oil demand in 2025 seen at 104.1mln bpd (prev. 104mln bpd) and 2026 seen at 105.2mln bpd (prev. 105.1mln bpd), while world oil production in 2025 was seen at 106mln bpd (prev. 105.9mln bpd) and 2026 production was seen at 107.4mln bpd (prev. 107.2mln bpd).

- Russia's Lukoil filed for an extension of the US Treasury's deadline prohibiting transactions with the company after Nov. 21st.

- Spot gold gradually extended on recent gains after returning to above the USD 4,200/oz level.

- Copper futures edged higher but with upside contained amid the mixed risk appetite.

CRYPTO

- Bitcoin marginally gained in choppy trade as prices swung back and forth of the USD 102k level.

NOTABLE ASIA-PAC HEADLINES

- BoJ Governor Ueda said they are aiming for stable inflation with a rise in wages and the BoJ is striving to achieve moderate inflation backed by wage growth by helping improve the economy, while he added the BoJ aims to achieve sustained economic growth that benefits the public. Ueda also said if long-term rates rise sharply in a way out of step with usual market moves, the BoJ is ready to respond flexibly, such as by increasing bond buying.

- South Korean Foreign Minister Cho asked US Secretary of State Rubio for a swift release of a joint fact sheet on last month's South Korea-US summit, while Rubio assured South Korea's Foreign Minister Cho that he would work with related US agencies for the release of a joint fact sheet on the summit, according to Yonhap.

DATA RECAP

- Japanese Corp Goods Price MM (Oct) 0.4% vs. Exp. 0.3% (Prev. 0.3%, Rev. 0.5%)

- Japanese Corp Goods Price YY (Oct) 2.7% vs. Exp. 2.5% (Prev. 2.7%, Rev. 2.8%)

GEOPOLITICS

MIDDLE EAST

- Israel reportedly conducted artillery raids and shelling on the eastern areas of Gaza and Khan Younis, according to Al Jazeera.

- White House said when asked about a report on the US mulling a base on the Gaza border, that this is not something the US is interested in.

- US Secretary of State Rubio said there's some concern of events in the West Bank spilling over and creating an effect that could undermine what they are doing in Gaza, but added they don't expect it to and will do everything they can to make sure it doesn't happen.

RUSSIA-UKRAINE

- US Secretary of State Rubio said as of now, the assessment the US has to make is that Russia does not really want peace.

- G7 Foreign Ministers said they are raising economic costs to Russia and exploring measures against countries and entities that are helping finance its war efforts.

EU/UK

NOTABLE HEADLINES

- Officials working for the UK Chancellor have asked the OBR to take into account measures on energy bills, rail fares and other forms of regulated prices in the upcoming budget forecasts, via Bloomberg citing sources; intended to provide extra fiscal space via lower inflation.

DATA RECAP

- UK RICS House Price Balance (Oct) -19% vs Exp. -14% (Prev. -15%)