US Market Open: Awaiting data schedule updates as the gov't reopens, Fed speak ahead

13 Nov 2025, 12:03 by Newsquawk Desk

- European stocks opened mixed and traded choppily since, with macro drivers light; FTSE 100 is subdued post-GDP.

- DXY drifted lower in early Europe after holding steady overnight, with little reaction to the passage and signing of the US funding bill that formally ends the shutdown.

- USTs opened softer as risk appetite improved overnight following the House vote to end the shutdown and President Trump signing the legislation.

- Crude benchmarks are steady after Wednesday’s slide, spot gold rises on a softer USD, and base metals extend on Wednesday’s gains.

- Looking ahead, highlights include US Cleveland Fed (Oct), New Zealand Manufacturing PMI (Nov). Speakers include BoE’s Greene, Fed’s Daly, Kashkari, Musalem & Hammack, ECB’s Elderson, SNB’s Tschudin & Moser, Supply from the US. Earnings from Applied Materials, Disney.

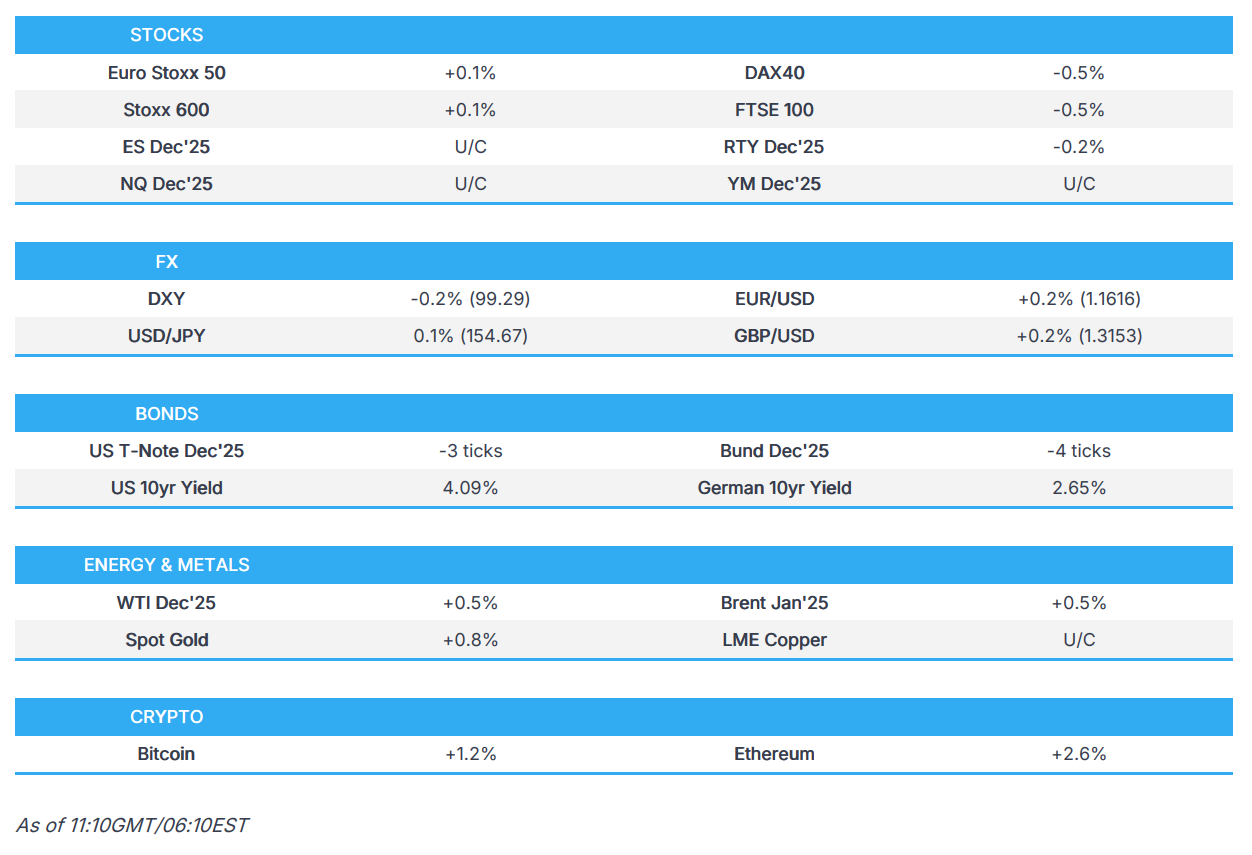

SNAPSHOT

TARIFFS/TRADE

- US officials flagged they will reduce tariffs on popular groceries, as pressure mounts to address the cost-of-living crisis, according to FT.

- EU is set to propose a plan to the US that would implement the next phase of the trade agreement reached in the summer, according to Bloomberg citing people familiar with the matter.

- EU seeks to accelerate crackdown on cheap Chinese parcels, according to FT.

- India announced anti-dumping duties on some steel products from Vietnam.

- China's Foreign Ministry said G7 countries should also stop manipulating trade issues with China.

EUROPEAN TRADE

EQUITIES

- European stocks opened mixed and traded choppily since, with pressure led by the DAX and FTSE 100. Softer UK Q3 GDP and weak manufacturing output hit UK sentiment and coupled with political uncertainty around PM Starmer weighs on the FTSE. Macro drivers were otherwise limited, though the morning brought a heavy earnings slate from names such as Deutsche Telekom, Siemens, Flutter, and Rolls-Royce.

- Sectors are mixed, with outperformance from Technology (+0.8%), Chemicals (+0.7%), and Insurance (+0.7%). Prosus (+3.0%) outperformed after Tencent’s earnings, lifting Tech, while Insurance and Chemicals gained amid light sector-specific news. Laggards include Financial Services (-1.5%), Energy (-0.5%), and Autos & Parts (-0.5%). Energy weakened as crude softened on constructive Russia–Ukraine headlines and mixed private inventories, with BP (-1.6%) and Shell (-1.1%) trading ex-div. Financial Services were dragged lower by a -11.5% slump in 3i post-interims, while Autos eased after strong gains in the prior session.

- US equity futures are mixed with a tentative feel. President Trump’s signing of the funding bill ended the shutdown but offered little support as the outcome was widely expected, with attention now shifting to a potential end-January shutdown risk. Broader uncertainty persists amid reports that October jobs and CPI data may not be released due to disruption at the BLS and other agencies. Today’s Fed speaker lineup features Musalem (’25, no text), Kashkari (’26, no text), Hammack (’26, no text), and Daly (’27, text + Q&A).

- Click for the sessions European pre-market equity newsflow

- Click for the additional news

- Click for a detailed summary

FX

- The DXY drifted lower in early Europe after holding steady overnight, with little reaction to the passage and signing of the US funding bill that formally ends the shutdown. Markets remain wary that the deal only delays the issue, with another funding standoff possible at end-January. Data uncertainty persists after the White House signalled that October CPI and jobs reports are unlikely to be released, while the BLS has given no timing confirmation; only September data is assured, with no date set. White House adviser Hassett warned the shutdown will drag Q4 GDP to 1.5–2.0%, with full-year growth near 2%, though he said supply-side policies should support growth without boosting inflation. The DXY trades near fresh weekly lows at the bottom of a 99.15–99.59 range, with support at 99.00 and the 98.91 low from October 30th.

- EUR/USD firmed as the pair followed the dollar’s slide, breaking above 1.1600 after an indecisive overnight session, driven by broad USD weakness rather than fresh Eurozone catalysts. EUR/USD holds within a 1.1579–1.1635 band, just shy of the 1.1637 October 30th high, with the 50DMA (1.1662) and 100DMA (1.1663) closely aligned overhead.

- GBP/USD posted modest gains after an initial dip on slightly softer UK GDP (-0.1% M/M vs Exp. 0.0%), before recovering on broader USD weakness. BoE pricing turned marginally more dovish (≈1bp) post-data, while focus remains on the fiscal challenges facing Chancellor Reeves ahead of the Nov 26 Budget, where she must balance discipline with avoiding growth or inflation risks. Political uncertainty around PM Starmer persists, though tensions eased after the Health Secretary dismissed reports of an attempted ouster. GBP/USD trades in a 1.3101–1.3171 band, with resistance at 1.3184 (Tuesday high) and 1.3191 (Monday peak).

- USD/JPY traded without clear direction overnight, easing after meeting resistance near 155.00. The pair extended lower into Europe as the dollar softened and risk sentiment faded. USD/JPY now sits toward the lower end of a 154.32–155.01 band, holding comfortably within yesterday’s 154.04–155.04 range.

- The Antipodeans diverged, with AUD/USD outperforming after stronger labour data and a drop in unemployment. The upbeat release briefly pushed AUD/NZD to 1.1637 before slipping back below 1.1600 (vs earlier 1.1534 low). As a result, NZD/USD lagged, unable to fully benefit from broader USD softness given AUD-driven cross dynamics.

- PBoC set USD/CNY mid-point at 7.0865 vs exp. 7.1156 (Prev. 7.0833).

- Click for a detailed summary

- Click for NY OpEx Details

FIXED INCOME

- USTs opened softer as risk appetite improved overnight following the House vote to end the shutdown and President Trump signing the legislation. Futures dipped to 112-27, around five ticks lower, matching Wednesday’s base and holding above the 112-20/112-15 lows from earlier in the week. The move later retraced as risk sentiment faded, lifting fixed income, JPY, and gold, while the USD came under pressure. With markets now awaiting delayed US data, the near-term bias appears dovish. Today’s lineup features Daly, Hammock, Kashkari, and Musalem, ahead of a 30yr auction. Data vendors are expected to update release schedules shortly, with some prints potentially arriving next week. Officials have suggested October BLS data may not be published, though confirmation is still awaited. Any forthcoming data will shape expectations for December, with markets pricing a ~55% chance of a 25bps cut, leaving the short end sensitive to the timing and tone of releases.

- Bunds traded directionally in line with USTs, slipping to an early 129.19 low before rebounding as the broader risk tone deteriorated, lifting the benchmark to a fresh 129.40 WTD high. German-specific news was limited, with focus instead on France and ongoing discussions around Ukraine funding.

- OATS welcomed positive developments for PM Lecornu as the National Assembly adjourned with 200+ amendments still pending, but crucially advanced the Social Security Financing Bill to the Lower House. Politico cited PS representative Guedj describing Lecornu as “fair” and “trustworthy,” a welcome endorsement ahead of renewed focus on the separate revenue bill. The vote on the revenue section is slated for November 17th, before lawmakers return to the Social component, with targeted passage by November 24th. While several contentious points remain, the momentum is favourable for both Lecornu and France’s fiscal trajectory. In response, the OAT–Bund 10yr spread has continued to tighten, narrowing to 72bps.

- Gilts opened firmer by five ticks on the dovish read from the morning’s soft growth data and strength in peers, before quickly reversing to a 93.60 trough (down ~10 ticks). The initial dovish impulse (Gilt-positive, yield-negative) was partly offset by the implied fiscal strain ahead of November’s Budget, which proved briefly Gilt-bearish. The move was short-lived, and Gilts later rebounded to a 93.83 peak, posting gains of up to 18 ticks and briefly outperforming as December cut odds ticked up by ~1bp to ~21bps. Focus now turns to upcoming October and November inflation prints, which will be pivotal given the MPC split and Governor Bailey’s likely tie-breaking role ahead of the December decision.

- Italy sold EUR 8bln vs exp. EUR 6.5-9.0bln 2.35% 2029, 3.25% 2032, 3.25% 2032, 4.65% 2055 BTP.

- Click for a detailed summary

COMMODITIES

- Crude benchmarks are steady after Wednesday’s ~USD 2.60/bbl slide, which followed OPEC’s modest upward revision to its 2025 supply outlook, reinforcing oversupply concerns. WTI trades USD 58.12–58.56/bbl and Brent USD 62.34–62.81/bbl through European hours. The IEA’s monthly report — raising 2025–26 demand and supply forecasts broadly in line with the EIA and OPEC (which kept its demand growth view unchanged) — drew little market reaction. Elsewhere, Reuters reported Russia’s Orsk refinery will remain offline until Sunday after Tuesday’s Ukrainian drone strike.

- Spot gold consolidated overnight within a USD 4180–4219/oz band after Wednesday’s sharp rally, before extending gains into Europe as the softer dollar provided support. XAU now trades near session highs around USD 4235/oz. With the US government reopened, markets await delayed data: the White House confirmed the September BLS report will be released but warned that October CPI and jobs data may never be published. In a quiet catalyst environment, this uncertainty has likely contributed to renewed dollar weakness.

- Base metals extended Wednesday’s gains after President Trump confirmed the end of the US government shutdown. 3M LME Copper briefly dipped to USD 10.87k/t in early APAC trade before reversing higher as the House passed the reopening bill, peaking at USD 10.98k/t before easing to USD 10.95k/t into Europe.

- US Private Inventory Data (bbls): Crude +1.3mln (exp. +2.0mln), Distillate +0.9mln (exp. -2.0mln), Gasoline -1.4mln (exp. -1.9mln), Cushing -0.0mln

- US DoE announced that contracts were awarded for the acquisition of approximately 1mln barrels of crude for the SPR.

- Click for a detailed summary

CRYPTO

- Crypto markets are on a modestly firmer footing, with Bitcoin attempting to reclaim the USD 103k level, while Ethereum topped USD 3,500.

NOTABLE DATA RECAP

- EU Industrial Production MM (Sep) 0.2% vs. Exp. 0.7% (Prev. -1.2%, Rev. -1.1%)

- EU Industrial Production YY (Sep) 1.2% vs. Exp. 2.1% (Prev. 1.1%, Rev. 1.2%)

- UK GDP Estimate MM (Sep) -0.1% vs. Exp. 0.0% (Prev. 0.10%); YY (Sep) 1.10% vs. Exp. 1.30% (Prev. 1.30%, Rev. 1.20%); 3M/3M (Sep) 0.10% vs. Exp. 0.20% (Prev. 0.30%, Rev. 0.20%)

- UK GDP Prelim QQ (Q3) 0.1% vs. Exp. 0.2% (Prev. 0.3%); YY (Q3) 1.3% vs. Exp. 1.4% (Prev. 1.4%)

- UK RICS House Price Balance (Oct) -19% vs Exp. -14% (Prev. -15%)

NOTABLE EUROPEAN HEADLINES

- Officials working for the UK Chancellor have asked the OBR to take into account measures on energy bills, rail fares and other forms of regulated prices in the upcoming budget forecasts, via Bloomberg citing sources; intended to provide extra fiscal space via lower inflation.

- EU's von der Leyen said the EU is working with Belgium on options to deliver on commitment to cover Ukraine's financing needs.

- The European Commission will reportedly encourage member nations finance officials to apply pressure on Belgium to back the EUR 140bln reparations loan for Ukraine, via Politico citing officials.

- German Economy Ministry, in its monthly report, said the recent threat of semiconductor supply bottlenecks and Chinese export restrictions on rare earths do not appear to pose an acute threat to the supply situation for German industry in short term.

- ECB's Buch said the markets are under-pricing geopolitical risk; adds new regulatory frameworks are not needed and needs commitment from legislators to not weaken current frameworks.

NOTABLE US HEADLINES

- US President Trump signed the government funding bill and announced an end to the government shutdown after the House voted to approve the bill, while Trump said the government will resume normal operations and reiterated a call for money to be paid to people directly to buy healthcare.

- US President Trump's administration froze flight cuts at 6% rather than hiking to 8% on Thursday, according to the US Department of Transportation.

- White House Economic Adviser Hassett said the government shutdown will impact this quarter's GDP and anticipates it to be between 1.5-2%, as well as noted that GDP for the year will be roughly 2% and that supply-side policies will allow growth without inflation. Hassett said he agreed with the last two Fed meetings that it was time to cut rates and noted the Fed is unlikely to cut 50bps, with the Fed more likely to do 25bps, while he added that he will do it if asked to be the Fed Chair.

- Fed's Collins (2025 voter) said it is likely appropriate to keep the policy rate on hold for some time and there is a relatively high bar for additional easing in the near term, while she is hesitant to ease policy further, absent notable labour-market deterioration and stated it is prudent to ensure inflation is durably on track to 2% before making any further policy rate cuts. Collins said further monetary support to activity runs the risk of slowing or stalling inflation's return to 2%, as well as noted that Fed policy is 'mildly restrictive' and that financial conditions are a tailwind for growth. Furthermore, she said dialling two notches down on rates made sense given risks and that elevated inflation warrants still mildly restrictive policy.

- Punchbowl writes, as the US shutdown ends, that it is now up to Johnson and Thune to determine how/if the Republican's will address health care costs. Surmising that "the next few months are strewn with political landmines for the GOP".

- Alphabet's (GOOGL) Google is subject to an EU antitrust investigation into its spam policy.

- Apple (AAPL) and Tencent (700 HK) agree on a 15% fee for WeChat game purchases, according to Bloomberg citing sources.

GEOPOLITICS

MIDDLE EAST

- Israel reportedly conducted artillery raids and shelling on the eastern areas of Gaza and Khan Younis, according to Al Jazeera.

- Israel is reportedly seeking a new 20-year security agreement with the US, doubling the usual term and adding "America First" provisions to win the Trump administration's support, according to Axios sources.

- White House said when asked about a report on the US mulling a base on the Gaza border, that this is not something the US is interested in.

- US Secretary of State Rubio said there's some concern of events in the West Bank spilling over and creating an effect that could undermine what they are doing in Gaza, but added they don't expect it to and will do everything they can to make sure it doesn't happen.

RUSSIA-UKRAINE

- US Secretary of State Rubio said as of now, the assessment the US has to make is that Russia does not really want peace.

- Russia's Kremlin said Ukraine must negotiate with Russia "sooner or later" and that its negotiation position is worsening by the day. Believes that Russia and Europe will resume dialogue sooner or later. Remans open to reaching a settle on Ukraine through political and diplomatic means. Wants peace settlement but will keep fighting in the absence of one to ensure its own security.

- G7 Foreign Ministers said they are raising economic costs to Russia and exploring measures against countries and entities that are helping finance its war efforts.

APAC TRADE

- APAC stocks followed suit to the mixed performance in the US, with little fresh catalysts as the government shutdown ended.

- ASX 200 was pressured amid underperformance in the tech, real estate and energy sectors, while stronger-than-expected jobs data from Australia did little to inspire a turnaround.

- Nikkei 225 was choppy as participants reflected on recent earnings releases and firmer-than-expected PPI data.

- Hang Seng and Shanghai Comp were mixed with strength in pharmaceuticals offset by weakness in energy and tech, while Chinese press noted that brokerage firms expect China's A-share market to continue to gain in 2026, with earnings growth anticipated to be around 4.7% next year.

NOTABLE ASIA-PAC HEADLINES

- BoJ Governor Ueda said they are aiming for stable inflation with a rise in wages and the BoJ is striving to achieve moderate inflation backed by wage growth by helping improve the economy, while he added the BoJ aims to achieve sustained economic growth that benefits the public. Ueda also said if long-term rates rise sharply in a way out of step with usual market moves, the BoJ is ready to respond flexibly, such as by increasing bond buying.

- South Korean Foreign Minister Cho asked US Secretary of State Rubio for a swift release of a joint fact sheet on last month's South Korea-US summit, while Rubio assured South Korea's Foreign Minister Cho that he would work with related US agencies for the release of a joint fact sheet on the summit, according to Yonhap.

- Alibaba (9988 HK / BABA) is preparing to overhaul the main mobile AI app in the coming months, in order to more closely resemble ChatGPT, via Bloomberg citing sources.

- China's Foreign Ministry on Japanese PM Takaichi's remarks, said despite strong protest from China, the PM has stubbornly refused to take that back. If Japan dares to intervene, that will constitute aggression. Japan must stop interfering in Chinese internals affairs.

NOTABLE APAC EARNINGS

- BiliBili (9626 HK) Q3 2025 (CNY): Revenue 7.69bln (prev. 7.31bln Y/Y). Average DAUs 117.3mln (prev. 107.3mln Y/Y), Margin 36.7% (prev. 34.9%).

- JD.Com Inc (JD) Q3 2025 (CNY): EPS 3.73 (exp. 2.89), Revenue 299.1bln (exp. 293.95bln). CEO: “In the third quarter, we continued to see strong growth in both user base and shopping frequency, and the number of our annual active customers surpassed a new milestone of 700 million in October.”

- Kioxia (285A JT) 6-month (JPY): Revenue 791bln (prev. 909bln), Operating Profit 132bln (prev. 292bln), PBT 84bln (prev. 248bln). 9-month guidance: Operating Income 229-269bln (exp. 268bln). Net Sales 1.29-1.34tln (exp. 1.31tln). Net Income 118.9-146.9bln (exp. 143bln)

- SMIC (981 HK) Q3 2025 (CNY): Net 191mln (exp. 183mln), Gross Margin 22% (exp. 19.6%).

- Tencent (700 HK) Q3 2025 (CNY): Revenue 192.9bln (exp. 188.8bln), Adj. Net 70.6bln (exp. 66bln). Operating 72.6bln (exp. 61.3bln); Strategic investment in AI is benefiting the company in business areas such as ad targeting and game engagement. Revenue Breakdown (CNY): International Game Revenue 20.8bln (exp. 18.1bln), Domestic Game Revenue 42.8bln (exp. 42.3bln), Social Networks Revenue 32.3bln (exp. 32.8bln)

DATA RECAP

- Japanese Corp Goods Price MM (Oct) 0.4% vs. Exp. 0.3% (Prev. 0.3%, Rev. 0.5%); YY (Oct) 2.7% vs. Exp. 2.5% (Prev. 2.7%, Rev. 2.8%)

- China M2 Y/Y money supply (Oct) 8.2% vs exp. 8.1%.