Europe Market Open: APAC and Wall St losses stream into Europe with European equity futures lower

18 Nov 2025, 06:42 by Newsquawk Desk

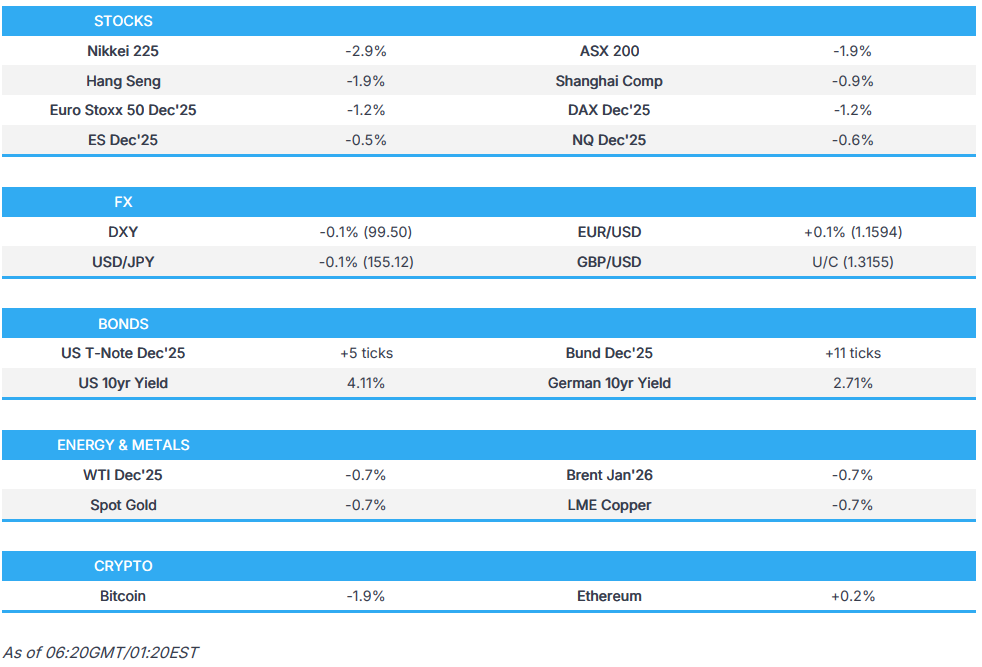

- APAC stocks extended losses throughout the session following a similar lead from Wall Street, which had seen heavy losses on Monday. Overall newsflow in APAC hours was quiet, although tech stocks were among the laggards in the region.

- DXY traded flat for most of the session and eventually drifted lower before dipping under 99.50 despite quiet newsflow, but as haven FX (JPY and CHF) gained amid risk aversion.

- JGB futures saw limited movement at the short end while the long end continued to weaken, pushing the 20-year yield to its highest level since July 1999.

- Bitcoin saw deep losses and eventually fell under the USD 90,000 mark to levels last seen in April, whilst Ethereum fell under USD 3,000.

- European equity futures are indicative of a lower cash open, with the Euro Stoxx 50 future down 1.1% after cash closed 0.9% lower on Monday.

- Looking ahead, highlights include US ADP Weekly Estimate, US Factory Orders (Aug), US Durable Goods (Aug), and Japanese Trade Balance. Speakers include ECB’s Elderson; BoE’s Pill, Dhingra; Fed’s Barr, Barkin. Earnings include Home Depot, Baidu, Medtronic, PDD; Imperial Brands, Diploma.

- Click for the Newsquawk Week Ahead.

US TRADE

EQUITIES

- US stocks saw heavy losses on Monday, with all sectors, aside from Communications and Utilities, in the red. There was no one specific catalyst for the risk-off trade to start the week, just further concerns regarding elevated valuations in the AI space, while the SPX slipped below 6,700 and closed beneath its 50-DMA of 6,707.

- SPX -0.91% at 6,672, NDX -0.83% at 24,800, DJI -1.18% at 46,590, RUT -1.96% at 2,341

- Click here for a detailed summary.

NOTABLE US HEADLINES

- US President Trump said he wants 1% inflation, according to Bloomberg.

- Fed Governor Waller made the case for continuing interest-rate cuts and said he supports a 25bps cut in December, arguing it would provide additional labour-market insurance, via the Federal Reserve; in the Q&A, Waller said that if the job market rebounds there would be less need for insurance cuts, and that the balance sheet is essentially where it needs to be. He said rising market rates suggest reserves are becoming scarce, and that the balance sheet may need to grow again within months; he noted increasing reports of planned layoffs, said the Fed should pay more attention to the labour market than to the current inflation overshoot, and that firms are funding AI investments by not hiring, with low- and middle-income households cutting spending and affecting hiring. He said a 25bps cut will not restore previous job-growth levels, warned razor-thin votes could undermine confidence in future decisions, and said the neutral rate is unclear. He added the Fed needs a stronger reason than five years of above-target inflation to avoid cutting, said he would have ended QE earlier, noted no market stress from a higher budget deficit, flagged difficulty judging the accuracy of the October jobs data, and said past experience has made the Fed more cautious about 50bps cuts

- Amazon’s (AMZN) US dollar bond sale drew roughly USD 80bln of demand, according to Reuters. Amazon set the size of its US dollar bond offering at USD 15bln, according to Bloomberg.

- Apple (AAPL) iPhone sales surge in China, taking 25% share, according to Bloomberg citing Counterpoint.

- Federal Reserve Governor Lisa Cook’s lawyer provided the first detailed defence of her mortgage applications, arguing that apparent discrepancies in loan documents were either accurate at the time or an “inadvertent notation”, according to the WSJ.

DATA RECAP

- Atlanta Fed GDPnow (Q3): 4.1% (prev. 4.0%).

TRADE/TARIFFS

- The UK is reportedly considering options to retaliate against Europe over steel tariffs, with the government working on counter-measures should it fail to secure preferential treatment on EU plans to raise steel-import tariffs to 50% and cut existing quotas by nearly half; the UK is also examining how to accelerate the replacement of its own steel safeguards, due to expire in June next year, so it can introduce its own tightened import quotas, according to Bloomberg citing sources.

- US President Trump said a country — which he did not specify — wanted to try to renegotiate the terms of its trade deal.

- US President Trump said he expects to issue dividends to Americans based on tariff revenues, probably in the middle of 2026, according to Reuters.

APAC TRADE

EQUITIES

- APAC stocks extended losses throughout the session following a similar lead from Wall Street, which had seen heavy losses on Monday. Overall newsflow in APAC hours was quiet, although tech stocks were among the laggards in the region.

- ASX 200 showed a clear defensive bias across its sectors, with tech the hardest hit. No obvious reaction was seen to the RBA minutes, which largely emphasised uncertainty and data-dependence.

- Nikkei 225 edged lower after the open and eventually surrendered the 49,000 level, falling as much as 3% intraday. Several additional factors on top of the global risk aversion could've exacerbated losses, including woes surrounding Japan–China relations and the recent JPY and long-end JGB weakness. Several Japanese officials verbally intervened throughout the session but failed to sway the index meaningfully.

- KOSPI lagged as the index joined the global stock rout, following the prior day's outperformance.

- Hang Seng and Shanghai Comp opened in the red and initially conformed to regional losses, with Hong Kong underperforming the Mainland amid its tech exposure.

- US equity futures traded on either side of the flat mark, initially resuming trade in modest positive territory before reversing as the mood from APAC lightly seeped into US futures.

- European equity futures are indicative of a lower cash open, with the Euro Stoxx 50 future down 1.1% after cash closed 0.9% lower on Monday.

FX

- DXY traded flat for most of the session but eventually drifted lower before dipping under 99.50 despite quiet newsflow, but as haven FX (JPY and CHF) saw some gains due to risk aversion. Participants look ahead to Tuesday’s ADP report, Wednesday’s FOMC minutes, and the delayed US data due later in the week, while a broader macro reaction to NVIDIA earnings cannot be ruled out.

- EUR/USD was uneventful in a narrow range below 1.1600 for most of the session before USD weakness took the pair back around the round figure, with light newsflow and little on the near-term calendar for EUR traders, leaving EUR pairs and crosses largely at the whim of the quote currency.

- GBP/USD traded flat in similarly muted conditions for a majority of the session before USD weakness lifted the pair more convincingly above 1.3150, with attention limited to remarks from BoE’s Dhingra scheduled after the European close today.

- USD/JPY was broadly unchanged for most of the session despite the APAC risk-off tone, after choppy moves triggered by fresh rounds of verbal intervention from Japanese officials, including Finance Minister Katayama, noting alarm over FX volatility, which briefly supported the JPY. The pair later gained amid late haven flows, with USD/JPY eventually falling under the 155.00 mark.

- Antipodeans drifted lower throughout the session amid the risk aversion. AUD showed little immediate reaction to the RBA minutes, which offered limited fresh detail but reiterated a cautious, data-dependent stance.

- PBoC set USD/CNY mid-point at 7.0856 vs exp. 7.1096 (Prev. 7.0816)

FIXED INCOME

- 10yr UST futures were in a tight, choppy range, mirroring the modest, risk-driven gains seen in the prior session amid the risk aversion across APAC.

- Bund futures eventually moved into the green amid the risk aversion, whilst lows were seen at the open, although the contract found support just above the 128.50 mark, with little on the EZ docket ahead.

- JGB futures saw limited movement at the short end while the long end continued to weaken, pushing the 20yr yield to its highest level since July 1999. Repeated verbal intervention from Japanese officials did little to arrest the decline.

- Australia sold AUD 300mln 4.75% 2054 AGB; b/c 2.85x (prev. 4.05x), average yield 5.0603% (prev. 4.8213%)

- China began marketing a EUR bond sale to raise up to EUR 4bln; guidance was set at mid-swaps +28bps for the 4-year tranche and mid-swaps +38bps for the 7-year tranche, according to Bloomberg and the term sheet.

COMMODITIES

- Crude futures were pressured by the broader risk-off tone. Energy-specific headlines were limited, while geopolitical developments included sharp nuclear rhetoric from North Korea and the UN Security Council’s adoption of a US-led resolution to establish an international stabilisation force in Gaza, with 13 votes in favour and abstentions from Russia and China.

- Spot gold softened despite steady FX and risk aversion across APAC, with precious metals offered as spot gold met resistance just above USD 4,050/oz and silver failed to hold above USD 50/oz.

- Copper futures were weighed by the risk-off backdrop, though declines in base-metal futures remained shallower than those seen in spot precious metals.

- Rio Tinto (RIO AT/RIO LN) is imposing surcharges on aluminium shipments it sells to the US, according to Bloomberg.

- Rio Tinto (RIO AT/RIO LN) reduced production at its Yawun alumina refinery to extend its operational life, with output set to decline by 1.2mln tonnes annually and the refinery’s production to be cut by 40% in 2026, according to Reuters.

CRYPTO

- Bitcoin saw deep losses and eventually fell under the USD 90,000 mark to levels last seen in April, whilst Ethereum fell under USD 3,000.

- Technicians will be cognizant of the "death cross" formed for Bitcoin as the 50 DMA fell under the 200 DMA.

NOTABLE ASIA-PAC HEADLINES

- Japanese Finance Minister Katayama said she is keeping an eye on markets with regard to fiscal policy and would not comment on FX levels, adding she is alarmed over FX moves; she said currencies should move in a stable manner reflecting fundamentals, and that the government will thoroughly monitor for excessive or disorderly forex fluctuations with a high sense of urgency. She noted concern over recent one-sided, rapid FX moves and said that while GDP avoided the worst, negative growth justifies a sizeable package, according to Reuters.

- Japan’s Economy Minister Kiuchi said long-term rate moves are determined by markets and that the government is watching market moves — including long-term rates — closely, according to Reuters.

- RBA November meeting minutes said it is appropriate in the current environment to remain cautious and data-dependent, with members determined they could remain patient while assessing incoming data on the extent of spare capacity. On rates, the minutes noted a mixed picture on whether policy remains restrictive — in contrast with the clearer signals seen in 2024 — and said the cash rate could be held at its current level if demand recovers more strongly than expected, while policy easing is still seen if the labour market weakens materially or growth disappoints; the Board said it is not possible to be confident about which scenario is more likely. The minutes said there may be a little more underlying inflationary pressure than previously assessed, noted the AUD remains close to equilibrium estimates, and said global growth is likely to slow in H2 2025, though the likelihood of a severe downside scenario has diminished, according to Reuters.

GEOPOLITICS

MIDDLE EAST

- The UN Security Council adopted the US-led resolution establishing an international stabilisation force in Gaza, with 13 countries voting in favour while Russia and China abstained, according to Reuters.

- Hamas said the UN resolution imposes international trusteeship on Gaza, which is rejected by Palestinians and factions, and that the resolution does not meet Palestinian rights and demands, according to Reuters.

- US President Trump said the US will be selling F-35s (LMT) to Saudi Arabia.

RUSSIA-UKRAINE

- A White House official said President Trump would sign the Russia-sanctions bill if decision-making authority remains, according to Reuters.

- The US Treasury said sanctions against Rosneft and Lukoil are reducing Russian oil revenues and pushing Russian crude prices to multi-year lows, while Treasury OFAC analysis stated the sanctions may have a long-term negative effect on the volume of Russian oil sales.

- The Ukrainian military said a Russian missile attack targeted the east of the country, according to Al Arabiya.

OTHERS

- US President Trump, when asked if he would launch strikes against Mexico to stop drugs, said it is “okay with me” and added he is not happy with Mexico, saying Mexico knows where he stands, according to Reuters.

- Japan’s Trade Minister Akazawa said there are currently no particular changes in China’s export-control measures on rare earths and other products, according to Reuters.

- North Korea said South Korea’s nuclear-propelled submarine will lead it to arm itself with nuclear weapons and said it will respond to the confrontational stance of the US–South Korea joint factsheet, via KCNA.

- The US Ambassador to Japan posted that the United States is fully committed to the defence of Japan, including the Senkaku Islands, and said nothing the China Coast Guard flotilla does can change that fact, via X.

EU/UK

NOTABLE HEADLINES

- UK Chancellor Reeves is reportedly considering a last-minute raid on banking profits in the budget, according to The Telegraph.