US Market Open: NQ underperforms as NVDA -4.4% pre-market following potential Meta-Google partnership

25 Nov 2025, 11:45 by Newsquawk Desk

- US Q3 GDP initial estimate is to be released on December 23rd, while US PCE and Personal Income report (Sep) was rescheduled for December 5th, according to the BEA.

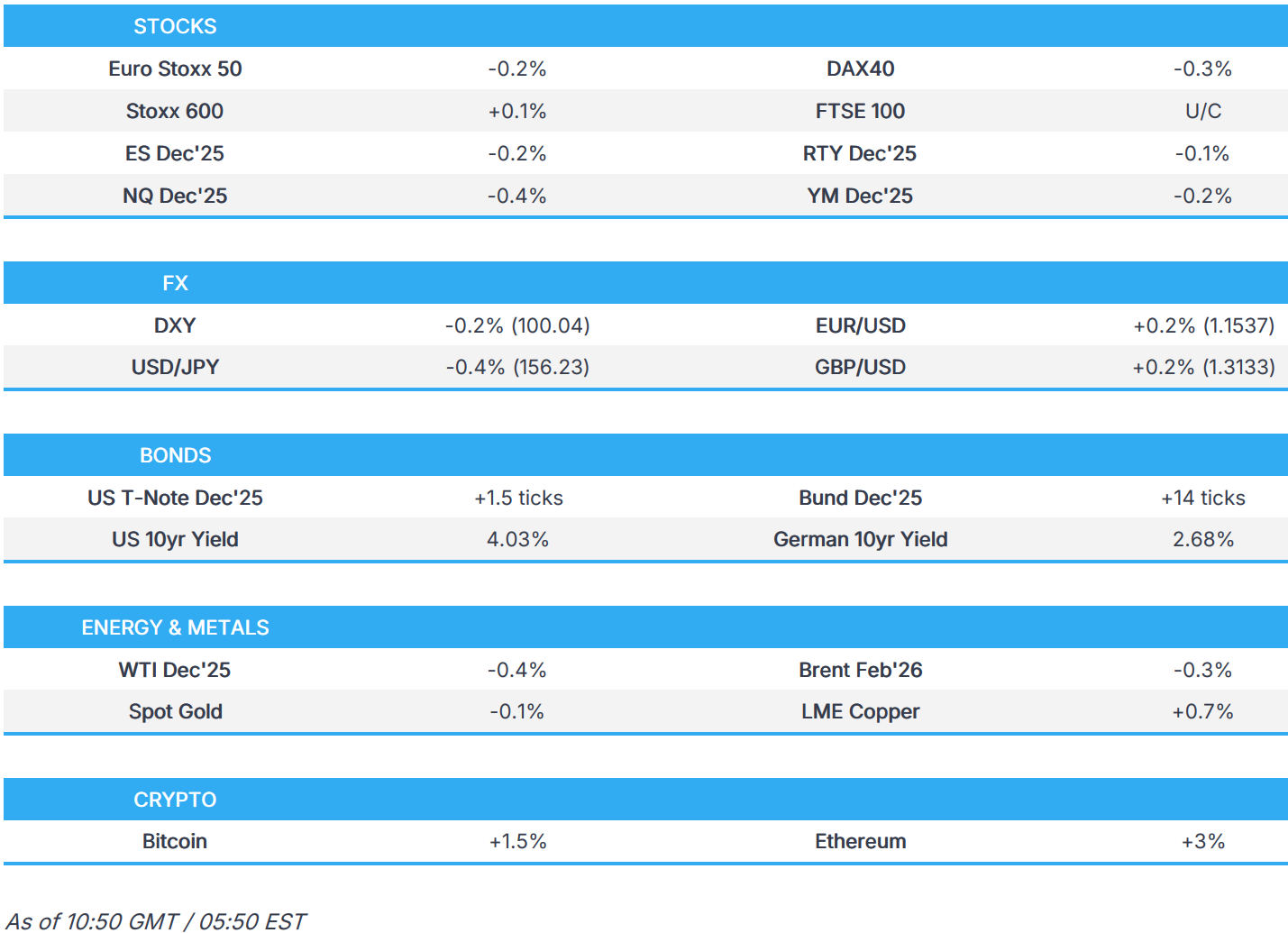

- European bourses are mostly lower alongside pressure seen in US equity futures; the NQ underperforms as NVIDIA (-4.4%) moves in the pre-market, on reports that Meta (U/C) is in talks to spend billions on Google's (+3.7%) AI chips.

- DXY moves lower, but still holds onto a 100.00 handle; JPY benefits from haven flows and PM Takaichi comments.

- Bonds hold an upward bias, given the subdued risk tone; Gilts unmoved by a relatively decent auction.

- Crude pulls back from recent gains, XAU is essentially flat and base metals are mixed.

- Looking ahead, US Weekly Prelim Estimate ADP, US PPI (Sep), Retail Sales (Sep), Consumer Confidence (Nov), Richmond Fed (Nov), Speakers including ECB’s Cipollone, Supply from the US, Earnings from Dell.

EUROPEAN TRADE

EQUITIES

- European bourses (STOXX 600 -0.1%) opened mixed, but have dipped off best levels in recent trade, to display a mostly negative picture in Europe. Nothing really behind the latest dip in sentiment, but did come alongside some pre-market pressure in NVIDIA as traders continue to digest Meta/Google related newsflow (detailed in the third bullet).

- European sectors are mixed. Basic Resources is the clear outperformer, continuing the sectoral strength seen in APAC trade, whilst Travel & Leisure is found towards the foot of the pile. For the latter, easyJet did initially see strength after its FY results, but dipped as markets digested rising costs. Also pressuring the sector is Evolution (-2.2%), which is dragged lower by a broker downgrade at Jefferies; analysts cited uncertainty re. potential litigation battle with Playtech.

- US equity futures (ES -0.2% NQ -0.4% RTY -0.1%) are trading lower across the board, albeit modestly so. There is some underperformance in the NQ, which has been pressured by pre-market losses in NVIDIA (-4.4%) amidst reports that Meta (U/C) is in talks to spend billions on Google's (+2%) AI chips.

- Alibaba Group Holding (BABA) Q2 2025 (CNY) adj. EPS 4.36 (exp. 4.59), Revenue 247.795bln (exp. 243.08bln), Adj. Net Income 10.352bln (exp. 9.497bln), Cloud Revenue 39.8bln (exp. 37.99bln), China e-commerce revenue 132.58bln (exp. 128.53bln)

- Click for the sessions European pre-market equity newsflow

- Click for the additional news

FX

- DXY resides towards the bottom end of a 100.01-100.26 range this morning, which is just inside Friday's 99.99-100.40 range. Upside is capped as rate cut bets were boosted following dovish rhetoric from Fed officials. From a more macro lens, attention is also on the Ukraine peace plan, which the Washington Post reported was now a 19-point plan, down from 28, with talks expected to continue. Elsewhere, it was announced that US President Trump and Chinese President Xi held a phone call that was said to be productive, in which leaders discussed many topics, including trade. The US schedule is heavy: weekly ADP average jobs data for the four weeks to 8th November are set for release (last week, the average rate of additions improved to -2.5k). US September PPI is seen rising 0.3% M/M (prev. -0.1%).

- EUR/USD is a little firmer today and trades within 1.1512 to 1.1540 range. Really not much to talk about from a European specific standpoint today, aside from German GDP (Q3) which was unrevised. Upside today comes in the context of a softer USD and optimism surrounding peace. Despite the optimism, there is still heightened uncertainty regarding the path to peace - as such the upside in the single currency has been relatively muted.

- JPY stands as the outperformer, recent weakness has spurred expectations of potential BoJ intervention, whilst wages are also on watch as Japanese PM Takaichi said the government is to spend JPY 1tln on SME wage hike support, and asking cooperation for base pay gains above inflation. This alongside the risk tone has helped to strengthen the JPY today. USD/JPY is currently at the bottom of a 156.15-156.98 range, dipping under Monday's 156.37 low, with Friday's trough at 156.20.

- Cable is a little firmer and trades above the 1.3100 mark in a 1.3096 to 1.3140 range; a peak which is roughly 4 pips above its 21-DMA. The Pound is largely moving at the whim of a slightly lower Dollar, but with price action contained into the Autumn Budget on Wednesday.

- AUD and NZD lower on broader risk whilst the latter looks ahead to a widely anticipated rate cut by the RBNZ at tomorrow's meeting (full Newsquawk RBNZ preview available on the Research Suite).

- PBoC set USD/CNY mid-point at 7.0826 vs exp. 7.1056 (Prev. 7.0847).

FIXED INCOME

- USTs are flat/slightly firmer. Initially moved lower soon after the European open, but then gradually edged off worst levels as global sentiment dipped. Nothing really behind the latest slip in the risk tone, but does come as NVIDIA (-3%) continues to sell off in the pre-market. Markets will remain focused on PPI, Retail Sales and ADP Weekly Prelim Estimate later today. USTs are currently trading within a 113-09+ to 113-15 range.

- Bunds are firmer by just over 10 ticks, and essentially following global peers. Currently towards the upper end of a 128.75 to 128.93 range, alongside the souring risk tone. Earlier, German GDP (Q3) which were unrevised, had little impact on German paper. Thereafter, German paper traded choppy into a 2030 Bobl Auction, which drew a better-than-prior b/c. No real move to the benchmark.

- Gilts opened flat, and then gained alongside peers. Currently towards the upper end of a 92.18 to 92.44 range, next level to the upside would be 92.46 which marks the 19th November peak. A relatively strong 2031 auction, which drew a b/c a touch above 3x, had little impact on Gilts.

- Netherlands sells EUR 1.445bln vs exp. EUR 1.0-2.0bln 3.50% 2056 DSL; Average yield 3.469%.

- UK sells GBP 4.5bln 4.125% 2031 Gilt: b/c 3.01x, average yield 4.088%, tail 0.6bps.

- Italy sells EUR 2bln vs exp. EUR 1.5-2bln 2.10% 2027 BTP Short Term & EUR 2.5bln vs exp. EUR 2-2.5bln 1.10% 2031, 2.40% 2039 BTPei.

COMMODITIES

- WTI and Brent have pulled back from Monday's bid higher despite the absence of any clear drivers. After peaking at USD 59.06/bbl and USD 62.92/bbl respectively in the latter part of Monday's session, benchmarks have gradually pulled back and have formed a trough at USD 58.32/bbl and USD 62.14/bbl. This comes as the risk tone started on the back foot at the start of the European session. Currently, benchmarks have bounced off their session lows as the global risk tone improves.

- Spot XAU trades choppy following Monday's bid above USD 4100/oz on dovish Fed rhetoric. After peaking at USD 4156/oz in the early hours of the APAC session, XAU pulled back to a trough at USD 4110/oz before a slight rebound as the risk tone soars following downside in NVIDIA (NVDA) shares.

- 3M LME Copper gapped higher and drove from USD 10.80k/t to a peak of USD 10.89k/t at the start of the APAC session as it followed on from Monday's positive risk tone and the Trump-Xi meeting. As the European session got underway, the red metal has pared back some of its initial gains as the risk tone starts to weaken, but remains near USD 10.85k/t.

- An announcement on North Sea energy licenses is expected on Wednesday, to coincide with the Budget, via Politico citing sources; official cited says there is likely to be a "pragmatic" shift on policy.

- India's Russian oil imports set to drop as sanctions hit according to Reuters citing sources. Sanctions to cause sharp December drop in Russian oil imports and refiners seek options on tighter Western curbs, bank scrutiny. US, EU sanctions pressure India's refiners to cut Russia buys.

- Hong Kong net gold exports to China (Oct) 8.02MT vs prev. 22.047MT; total gold export to China 30.08MT vs prev. 36.275MT.

- Caspian Pipeline Consortium says Black Sea terminal temporarily suspended oil loadings amid drone attacks.

NOTABLE DATA RECAP

- German GDP Detailed YY NSA (Q3) 0.3% vs. Exp. 0.3% (Prev. 0.3%)

- German GDP Detailed QQ SA (Q3) 0.0% vs. Exp. 0.0% (Prev. 0.0%)

- French Consumer Confidence (Nov) 89.0 vs. Exp. 90.0 (Prev. 90.0)

NOTABLE EUROPEAN HEADLINES

- UK Treasury asked banks to make public and prominent endorsements of the Budget this week, wanting lenders to praise new policies and show how they will boost lending to first-time buyers and small businesses, according to FT.

- French PM Lecornu has scheduled a debate on Wednesday, 10th December on defense and resources, via Politico citing sources. A second debate will be held on December 15th.

- French Socialist (PS) Leader Faure says he sees the budget as possible

NOTABLE US HEADLINES

- Fed's Kashkari (2026 voter) said there are real use cases for AI, but not for crypto, and noted people are feeling hardship due to inflation.

- White House said US President Trump signed an executive order related to AI research, while the order will boost AI-accelerated innovation and directs the building of AI platforms to harness federal scientific data sets.

- US Q3 GDP initial estimate is to be released on December 23rd, while US PCE and Personal Income report (Sep) was rescheduled for December 5th, according to the BEA.

- US House Speaker Johnson reportedly cautioned the White House that most House Republicans are not in favour of extending enhanced ACA subsidies, via WSJ citing sources.

GEOPOLITICS

MIDDLE EAST

- Taliban spokesman Mujahid said aerial raids took place in the provinces of Kunar and Paktika, which injured four civilians, while it was announced that nine children were killed after Pakistani forces bombed the home of a local resident in the Khost province.

RUSSIA-UKRAINE

- US is holding secret Russia-Ukraine peace talks in Abu Dhabi with US Army Secretary Dan Driscoll meeting delegations from Kyiv and Moscow in a push for a deal to end Russia's invasion, according to FT.

- A barrage of Russian missiles struck Kyiv overnight, in what the Ukrainian Energy Minister described as a "massive" attack on energy infrastructure, while the Kyiv Mayor said that some areas were experiencing disruptions to power and water.

- Regional Governor said three people were killed and 10 injured in a Ukrainian attack on Russia's Rostov region.

- Russia's Kremlin says that adjustments are being made to the published text of the Ukraine peace plan. Adds that it is impossible to discuss security system without participation of Europeans and at some stage this will be necessary and that Russia hasn't received adjusted US plans for Ukraine via RIA.

OTHER

- Taiwan's Premier said Taiwan is a fully sovereign and independent country and that for Taiwan's 23mln people, a ‘return’ to China is not an option, while he added that maintaining the status quo in the Taiwan Strait is a development the whole world is watching closely. Furthermore, he said they must strengthen self-defence capabilities and must stand together with like-minded democratic countries. In relevant news, Taiwan's Defence Ministry said a Chinese balloon was detected in the Taiwan Strait on Monday.

- Japanese Chief Cabinet Secretary Kihara said Japan's UN ambassador sent a letter to UN Secretary-General Guterres explaining Japan's stance on China's demand to withdraw PM Takaichi's remarks on Taiwan, while Kihara added that China’s claims that contradict the facts cannot be accepted, and Japan must firmly refute and communicate its position. It was separately reported that Japan's top foreign ministry official held talks with China's ambassador, according to Kyodo

- China asks airlines to extend flight cuts to Japan till March 2026, via Bloomberg citing sources.

- Drone reported on Romanian territory, according to CGTN. Alerts for residents in several counties to hide were lifted. Currently, no drone signals are being detects by radars in Romanian airspace. Too early to say how many drones breached the airspace (CGTN)

CRYPTO

- Firmer trade for the crypto complex, with Bitcoin back towards USD 87k whilst Ethereum moves higher and aims for USD 2.9k.

APAC TRADE

- APAC stocks traded mostly higher as the region took impetus from the tech-led rally on Wall St, where sentiment was bolstered as dovish comments from Fed officials boosted December rate cut bets.

- ASX 200 finished higher but lagged for most the session as strength in mining names was negated by underperformance in the top-weighted financial industry and losses in defensives.

- Nikkei 225 initially rallied on return from the extended weekend and briefly reclaimed the 49,000 level, before momentarily wiping out its entire spoils.

- Hang Seng and Shanghai Comp were underpinned by continued warming US-China relations following a call between US President Trump and Chinese President Xi, which Trump described as a very good call and noted that they discussed many topics, including Ukraine/Russia, fentanyl, soybeans and other farm products. The PBoC also conducted a CNY 1tln MLF operation that resulted in a net liquidity injection of CNY 100bln.

NOTABLE ASIA-PAC HEADLINES

- PBoC conducted a CNY 1tln Medium-term Lending Facility operation for a CNY 100bln net liquidity injection.

- Japanese PM Takaichi said she spoke with US President Trump on the phone after a phone call was proposed by the US side, and that Trump explained recent US-China relations following his call with Chinese President Xi. Furthermore, Trump told her that they are very close friends and that she could call him any time, while Takaichi believes they were able to confirm close cooperation between Japan and the US.

- Japanese Finance Minister Katayama said Japan has established a Japanese equivalent of the US Department of Government Efficiency to abolish ineffective subsidies.

- Japanese Chief Cabinet Secretary Kihara said the government is to hold a cabinet meeting on the supplementary budget this Friday.

- Japanese PM Takaichi says the government is to spend JPY 1tln on SME wage hike support; asking cooperation for base pay gains above inflation.