EU Market Open: A quiet session ahead with US away for Thanksgiving Holiday

27 Nov 2025, 06:54 by Newsquawk Desk

- APAC stocks were mostly higher following the positive momentum from Wall Street, where all major indices gained ahead of Thanksgiving celebrations.

- 10yr JGB futures edged higher but with the gains modest after reports that Japan is likely to increase issuances of 2yr and 5yr JGBs.

- Alibaba shares were pressured after the Pentagon said it should be on the list of firms with Chinese military ties, while China Vanke shares were hit and its bonds slumped.

- US President Trump told Japan to lower the volume on Taiwan, following a call with Chinese President Xi, according to WSJ.

- European equity futures indicate an uneventful open with Euro Stoxx 50 futures up flat after the cash market closed with gains of 1.5% on Wednesday.

- Looking ahead, highlights include German GfK (Dec), EZ M3 (Oct), Consumer Confidence Final (Nov), Japanese Tokyo CPI (Nov), Industrial Profit (Oct) & Retail Sales (Oct), ECB Minutes (Oct), Speakers including BoE’s Greene, ECB’s Cipollone & de Guindos, Supply from Italy.

- Holiday: US Thanksgiving Day; Desk will run normal services on Thursday, 27th November until 18:15GMT/13:15EST. At which point, the desk will close and then re-open later at 22:00GMT/17:00EST for the APAC session. Thereafter, there is normal service on Friday, 28th November until 18:15GMT/13:15EST at which point the desk will close.

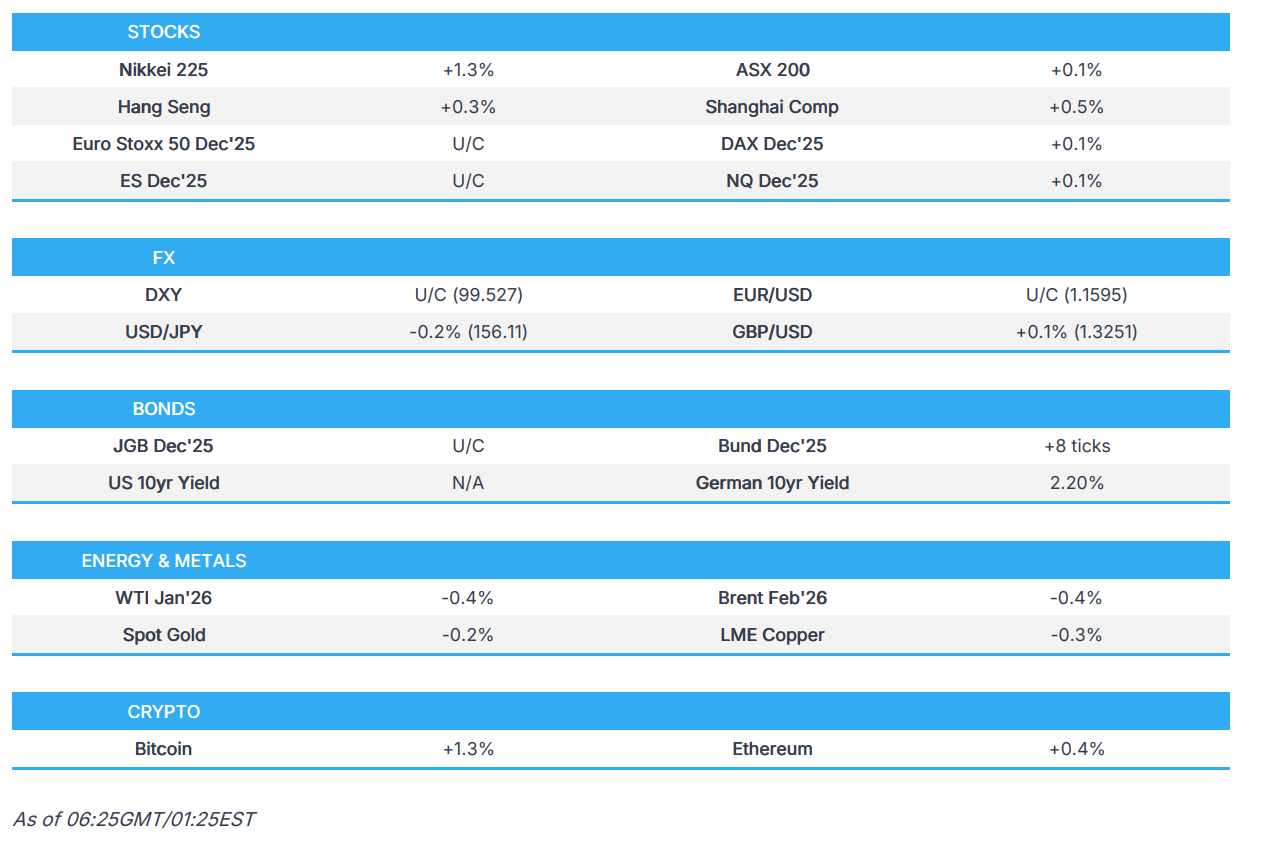

SNAPSHOT

US TRADE

EQUITIES

- US stocks gained as risk-on trade was evident heading into Thanksgiving with outperformance in the Russell and the Nasdaq, alongside broad-based gains. Tech was one of the clear outperformers, but Communications lagged with AI names trading higher after recent pressure, although Alphabet (GOOGL) gave up some of its recent rally, weighing on the comms sector. The latest US data was mixed with low initial jobless claims easing labour market concerns, and durable goods beat expectations, although Chicago PMI saw a notable slump.

- SPX +0.65% at 6,810, NDX +0.87% at 25,237, DJI +0.67% at 47,427, RUT +0.91% at 2,489.

- Click here for a detailed summary.

TARIFFS/TRADE

- USTR extended exclusions from China section 301 tariffs related to the forced technology transfer investigation until 10th November 2026.

- US Pentagon reportedly said that Alibaba (BABA/9988 HK) should be on the list for China military ties.

- Canadian PM Carney said talks with the US on trade have not restarted yet, while he had a short conversation with US President Trump on Tuesday and plans to go to Washington next week for the World Cup draw.

NOTABLE HEADLINES

- Fed Beige Book stated that economic activity was little changed since the previous report, according to most of the twelve Federal Reserve Districts, though two Districts noted a modest decline and one reported modest growth. It also noted that overall consumer spending declined further, although higher-end retail spending remained resilient, while employment declined slightly over the current period, with around half of the Districts noting weaker labour demand.

- US President Trump said regarding the shooting of National Guard members near the White House that the assault was an act of terror and the Department of Homeland Security is confident the suspect entered into the US from Afghanistan in 2021, while he directed the mobilisation of an additional 500 troops for Washington DC and said the US must re-examine every single alien who entered US from Afghanistan under Biden.

- US Citizenship and Immigration Services said that effective immediately, the processing of all immigration requests relating to Afghan nationals is stopped indefinitely pending further review of security and vetting protocols.

- US ordered American diplomats in Europe, Canada and New Zealand to press governments to restrict most immigration, according to NYT.

APAC TRADE

EQUITIES

- APAC stocks were mostly higher following the positive momentum from Wall Street, where all major indices gained ahead of Thanksgiving celebrations.

- ASX 200 eked slight gains amid tech outperformance and better-than-expected capex data, although the commodity-related sectors lagged.

- Nikkei 225 rallied to above the 50k level following reports that Japan is to issue more than JPY 11tln in additional government bonds for the FY25 extra budget, and with the supplementary budget expected to be about JPY 18.3tln.

- Hang Seng and Shanghai Comp both ultimately gained but with initial weakness seen in Hong Kong amid mixed fortunes among the Chinese tech heavyweights with Alibaba pressured after the Pentagon said it should be on the list of firms with Chinese military ties, while China Vanke shares were hit and its bonds slumped following reports that the developer is to hold a bondholder meeting to discuss repayment extension for a yuan bond due December 15th.

- US equity futures took a breather after recent advances, and with US participants away on Thursday for Thanksgiving Day.

- European equity futures indicate an uneventful open with Euro Stoxx 50 futures up flat after the cash market closed with gains of 1.5% on Wednesday.

FX

- DXY remained lacklustre after having softened heading into the Thanksgiving Day holiday and with mixed data releases from the US, where Jobless Claims fell, and Durable Goods also printed better than expected, but Chicago PMI disappointed. Meanwhile, the Fed Beige Book noted economic activity was little changed since the previous report, according to most of the twelve Federal Reserve Districts, although two Districts noted a modest decline and one reported modest growth.

- EUR/USD edged higher and breached through resistance at the 1.1600 level, as recent ECB commentary continued to suggest an unwillingness to cut rates, while the attention turns to the latest ECB minutes scheduled later.

- GBP/USD marginally extended on gains after climbing back above the 1.3200 level in the aftermath of the UK Autumn Budget.

- USD/JPY was choppy and traded both sides of the 156.00 level, while there were comments from BoJ's Noguchi, who reiterated that they will gradually adjust the degree of monetary accommodation if economic activity and prices develop in line with the bank's outlook and stated they must take a measured, step-by-step approach in adjusting policy.

- Antipodeans extended on recent advances with NZD sustaining the post-RBNZ momentum and with upside facilitated by the constructive risk tone and encouraging data releases including stronger New Zealand Retail Sales and Business Confidence, as well as better-than-expected Australian Private Capex.

- PBoC set USD/CNY mid-point at 7.0779 vs exp. 7.0733 (Prev. 7.0796).

FIXED INCOME

- 10yr UST futures were little changed with US markets closed for Thanksgiving Day and after the latest 7yr offering stateside was an overall soft auction, but was an improvement from the prior month.

- Bund futures sat above the 129.00 level but with gains capped after recent whipsawing and ahead of German GfK data.

- 10yr JGB futures edged higher but with the gains modest after reports that Japan is likely to increase issuances of 2yr and 5yr JGBs, as well as the sale of treasury bills under its revised plan, while there were plenty of comments from BoJ's Noguchi who advocated a gradual approach to hiking rates.

COMMODITIES

- Crude futures faded some of the gains from the prior session, where price action was choppy amid Russia/Ukraine peace efforts and mixed data, while the latest EIA inventory report showed a larger-than-expected build in headline crude stocks.

- Baker Hughes Rig Count: Oil -12 at 407, Natgas +3 at 130, Total -10 at 544.

- Spot gold marginally declined after yesterday's indecision, but with downside cushioned after recent dollar weakness.

- Copper futures took a breather after recently climbing in tandem with broader risk sentiment.

- LME executive said COMEX premium over LME is likely to persist over the next 18 months, while they are focused on listing new Chinese Indonesian brands in aluminium.

- ICSG Secretary General Paul White said world copper mine production is forecast to rise by 2.3% and world refined copper output is expected to rise by 0.9% in 2026, while world apparent refined copper usage is forecast to grow by 2.1% in 2026 and the global copper market will swing to a deficit of roughly 150,000 tons in 2026.

CRYPTO

- Bitcoin extended on its recent rebound with prices returning to above the USD 91,000 level.

NOTABLE ASIA-PAC HEADLINES

- China's market regulator conducted anti-unfair competition compliance guidance on smartphones and app platform firms in Shenzhen, while it stated that irrational competition is prominent in mobile phones and mobile applications.

- BoJ's Noguchi said the BoJ will gradually adjust the degree of monetary accommodation if economic activity and prices develop in line with the bank’s outlook, and if the price target is achieved in the second half of the projected period of the Outlook Report, the BoJ should adjust rates at an appropriate pace to align with that timeline, which means raising the policy interest rate at a pace that will make it possible to smoothly reach the neutral interest rate when the 2% inflation target is achieved. Furthermore, he said problems are likely to arise if the pace of policy adjustment is either too fast or too slow, and noted that the BoJ must take a measured, step-by-step approach in adjusting policy.

- Japan is likely to increase issuance of two- and five-year JGBs from January in a revised bond sale plan for fiscal 2025, and likely to increase the sale of treasury discount bills by around JPY 6tln, while the total JGB scheduled sales for fiscal 2025 are set to increase by around JPY 7tln from the current JPY 171.8tln under the revised plan, according to Reuters sources. In relevant news, Japan's fiscal 2025 supplementary budget is expected to be about JPY 18.3tln, according to NHK.

- Bank of Korea kept the base rate unchanged at 2.50%, as expected, while it stated that room will be left for potential rate cuts and it will decide whether and when to implement any further base rate cuts. BoK said domestic demand is expected to sustain the recovery, but export growth is likely to slow down, and the economy faces high uncertainties from the trade environment and domestic recovery. BoK Governor Rhee said Thursday's rate decision was not unanimous as board member Shin Sung-Hwan dissented in Thursday's rate decision and noted that domestic demand recovery is not strong. Rhee revealed that three board members said they are open to a near-term cut, and outside of Governor Rhee, the board is split 50-50 on whether the bank should cut rates or hold in the near term. Furthermore, he said the growth rate will be close to the Korean economy's potential next year and FX volatility remains high, while he added they need to be alert to its impacts on prices and have policy tools to stabilise the FX market if needed.

- RBNZ Governor Hawkesby said he thinks they are in a position where they can put out an OCR projection which is broadly unchanged, and in a position where they can sort of watch and wait to see how things progress over the course of the next year. Hawkesby separately commented that they have lowered the cash rate a lot and he is more confident now that official cash rate is actually stimulatory, while he also commented that the hurdle is high for any further rate cuts and cannot keep the door open to easing forever.

DATA RECAP

- Chinese Industrial Profits YY (Oct) -5.5% (Prev. 21.6%)

- Chinese Industrial Profits YTD YY (Oct) 1.9% (Prev. 3.2%)

- Australian Capital Expenditure (Q3) 6.4% vs. Exp. 0.5% (Prev. 0.2%)

- Australian Private Capital Expenditure for 2025-26 (AUD)(Estimate 4) 191.3B (Prev. 174.8B)

- New Zealand ANZ Business Confidence (Nov) 67.1% (Prev. 58.1%)

- New Zealand ANZ Activity Outlook (Nov) 53.1% (Prev. 44.6%)

- New Zealand Retail Sales Volumes Q/Q (Q3) 1.9% (Prev. 0.5%)

- New Zealand Retail Sales Y/Y (Q3) 4.5% (Prev. 2.3%)

GEOPOLITICS

MIDDLE EAST

- Australia's Foreign Minister said Australia listed Iran's Islamic Revolutionary Guard Corps as a state sponsor of terrorism.

RUSSIA-UKRAINE

- US reportedly demands a peace deal before security guarantees for Ukraine, according to Politico.

OTHER NEWS

- US President Trump told Japan to lower the volume on Taiwan, following a call with Chinese President Xi, according to WSJ. It was separately reported that Japanese government sources said US President Trump conveyed to Japanese PM Takaichi to avoid further escalation with China in a phone call on November 25th.

- US President Trump said the US will stop all payments and subsidies to South Africa and that South Africa will not be receiving an invitation to the 2026 G20, while he added that he did not attend the G20 in South Africa because the government refuses to acknowledge or address human rights abuses endured by Afrikaners, and other descendants of Dutch, French and German settlers. South African President Ramaphosa later noted that it was a regrettable statement by US President Trump regarding South Africa's participation in 2026 G20 meetings