US Market Open: Muted market action due to holiday lull and CME issues

28 Nov 2025, 11:20 by Newsquawk Desk

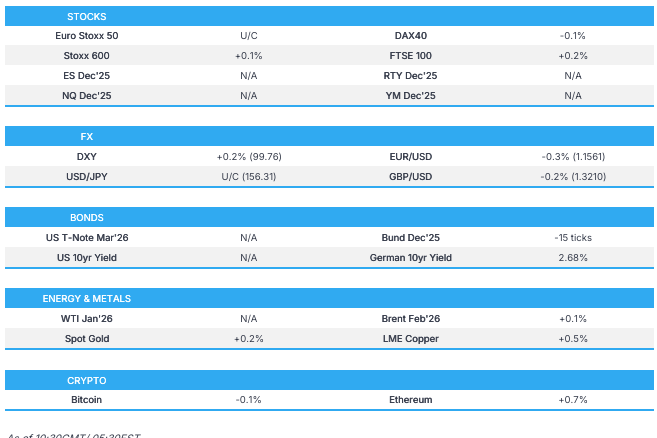

- European bourses are mostly flat, with the FTSE 100 (+0.1%) the only major index posting gains. Overall market action is muted amid light news flow, reflecting both Thanksgiving and the CME issues.

- An outage at CME Group has halted trade in FX, commodities, Treasuries and equities futures; "Due to a cooling issue at CyrusOne data centers, our markets are currently halted," CME said.

- DXY is firmer within a 99.50–99.75 range, having found support at the half-round figure and pushed above Thursday’s 99.71 peak.

- EGBs are ultimately a little softer post-data; the EUR dipped during the releases but has since bounced off lows.

- WTI and Brent traded with a positive bias overnight, extending the prior session’s gains. WTI trading was later halted due to the CME outage.

- Looking ahead, highlights Canadian GDP (Q3), German Nationwide HICP, Credit Review for France.

- Desk Schedule: There is normal service on Friday, 28th November until 18:15GMT/13:15EST at which point the desk will close.

SNAPSHOT

NOTABLE US HEADLINES

- CME Group (CME) says BrokerTec EU markets are open and trading, all other CME group markets remain halted amid the data center cooling issue at CyrusOne.

- CME announced that CME Globex futures and options markets were halted due to technical issues, and Cboe halted trading on C1 due to ongoing issues at CME. CME later announced that markets were halted due to a cooling issue at CyrusOne data centres, while it is working to resolve the outage issue and will advise clients of pre-open details as soon as available.

- US President Trump said that they may be cutting income tax almost completely because of tariff proceeds.

- US President Trump posted that he will permanently pause migration from all third-world countries to allow the US system to fully recover and will terminate all of the millions of Biden's illegal admissions, while he will end all federal benefits and subsidies to non-citizens.

- US President Trump ordered a review of all green card holders from countries "of concern" after the attack on National Guards in Washington DC, according to Axios.

TARIFFS/TRADE

- Nexperia issued an open letter to the leadership of Nexperia’s entities in China and noted that it continues to seek constructive collaboration with its entities in China, and has been requesting an open dialogue to find a path forward. Furthermore, it urged the leadership of Co.’s entities in China to take immediate steps towards structured negotiations to address the restoration of the supply chain, but added that it did not receive any meaningful response.

- Indonesia is reportedly resisting attempts by US President Trump to force it to accept a so-called “poison pill” and other coercive clauses in its “reciprocal tariff” trade deal with the US, according to FT.

- India expects to have a deal with the US before year-end as most issues are resolved, according to the Indian Trade Secretary

- EU Commission receives notifications from Apple (AAPL) under the Digital Market Act: Notifications from Apple (AAPL) indicated that its core platform services like Apple ads and maps meets the digital market thresholds.

EUROPEAN TRADE

EQUITIES

- European bourses are mostly flat, with the FTSE 100 (+0.1%) marginally higher this morning. Overall market action is muted amid light news flow, reflecting both Thanksgiving and the CME issues.

- European sectors are largely in the red. Basic Resources (+0.2%) and Energy (+0.3%) are marginal outperformers, supported by underlying moves in metals and energy. Laggards include Travel & Leisure (-0.7%), Autos (-0.4%) and Insurance (-0.4%). Ongoing Nexperia concerns continue to pressure Autos, as the company warns of imminent production halts.

- A CME Group outage has halted trading in US equity futures, with no guidance yet on reopening. Prior to the halt, futures were modestly firmer, with ES +0.1% and NQ +0.2%.

- Click for the sessions European pre-market equity newsflow

- Click for the additional news

FX

- DXY is firmer within a 99.50–99.76 range, having found support at the half-round figure and pushed above Thursday’s 99.71 peak. Fresh catalysts have been limited overnight and through the European morning, with FX futures on CME halted due to an exchange issue. Comments from US President Trump noted they may be cutting income tax almost completely using tariff proceeds.

- EUR and GBP are subdued against the USD but flat versus each other, leaving downside in the USD pairs driven by the Dollar rather than EZ- or UK-specific developments.

- JPY is flat and uneventful amid thin conditions and few catalysts, with USD/JPY holding a 155.65–157.18 range, comfortably inside Thursday’s 154.37–157.89 span.

- NZD is pulling back after recent post-RBNZ outperformance, while AUD/NZ D remains near weekly lows (1.1400) after sliding from a 1.1536 pre-RBNZ high.

- PBoC set USD/CNY mid-point at 7.0789 vs exp. 7.0769 (Prev. 7.0779)

FIXED INCOME

- EGBs are ultimately a little softer post-data; the EUR dipped during the releases but has since bounced off lows.

- Bunds briefly pushed above 129.00 on cooler French HICP before fading, slipping back below 129.00 and extending losses to ~128.84 despite broadly softer German state CPI prints.

- Gilts contained overall, but have traversed a relatively wide range of just under 40 ticks as traders digest what appears to be another manifesto U-turn, by PM Starmer; markets now await the verdict from Chancellor Reeves on the matter.

- UK DMO to sell GBP 1bln 4.25% 2039 Gilt via tender on Dec 4th.

COMMODITIES

- WTI and Brent traded with a positive bias overnight, extending the prior session’s gains. WTI trading was later halted due to the CME outage. Since then, Brent Feb ’26 has slipped from its overnight highs and is now moving within a USD 62.72–63.26/bbl range.

- Precious metals are firmer, though with limited catalysts this morning. Spot gold is confined to a narrow USD 4,147.92/oz–4,193.20/oz range, with geopolitics remaining the main focus.

- Base metals retain a strong positive tone, with 3M LME Copper trading near the top of its USD 10,940.56–11,008.40/t range. The current upside looks mainly like a modest rebound from recent pressure.

- Ukraine's military says it hit Russia's Saratov oil refinery.

CRYPTO

- Bitcoin is rangebound, trading on both sides of the USD 91,000 level and within yesterday's range.

NOTABLE EUROPEAN HEADLINES

- S&P said UK public finances remain constrained and it expects fiscal pressures in the UK to persist over the medium term despite revenue-raising measures announced in the Autumn Budget, while it added that general government deficits are forecast to moderate through to 2028 and there are risks to the UK’s fiscal consolidation plan, especially toward the end of the forecast horizon.

- Moody's says UK budget affirms commitment to fiscal consolidation however, they highlight execution risk.

- ECB Consumer Expectations Survey results (October 2025); 12-month inflation expectations raised, 3- and 5-year expectations unchanged.

NOTABLE EUROPEAN DATA RECAP

Germany

- German State CPIs chimed with mainland consensus for the M/M, but the Y/Y figures defied the bias for a modest uptick.

- German Retail Sales MM Real (Oct) -0.3% vs. Exp. 0.2% (Prev. 0.2%)

- German Import Prices MM (Oct) 0.2% (Exp. 0.0%, Prev. 0.2%)

- German Retail Sales YY Real (Oct) 0.9% vs. Exp. 0.1% (Prev. 0.2%)

- German Import Prices YY (Oct) -1.4% vs. Exp. -1.6% (Prev. -1.0%)

- German Unemployment Rate SA (Nov) 6.3% vs. Exp. 6.3% (Prev. 6.3%)

- German Unemployment Change SA (Nov) 1.0k vs. Exp. 5.0k (Prev. -1.0k)

France

- French GDP QQ Final (Q3) 0.5% vs. Exp. 0.5% (Prev. 0.5%)

- French CPI Prelim MM NSA (Nov) -0.1% vs. Exp. -0.1% (Prev. 0.1%)

- French CPI Prelim YY NSA (Nov) 0.9% vs. Exp. 1.0% (Prev. 0.9%)

- French Producer Prices YY (Oct) -1.2% (Prev. 0.1%)

- French CPI (EU Norm) Prelim MM (Nov) -0.2% vs. Exp. 0.0% (Prev. 0.1%)

- French CPI (EU Norm) Prelim YY (Nov) 0.8% vs. Exp. 1.0% (Prev. 0.8%)

- French Consumer Spending MM (Oct) 0.4% vs. Exp. 0.2% (Prev. 0.3%

Spain

- Spanish HICP Flash YY (Nov) 3.1% vs. Exp. 2.9% (Prev. 3.2%)

- Spanish CPI YY Flash NSA (Nov) 3.0% vs. Exp. 2.9% (Prev. 3.1%); Core 2.6% (prev. 2.5%)

- Spanish CPI MM Flash NSA (Nov) 0.2% (Prev. 0.70%)

- Spanish HICP Flash MM (Nov) 0.0% (Prev. 0.5%)

- Spanish Retail Sales YY (Oct) 3.8% (Prev. 4.2%, Rev. 4.1%)

Italy

- Italian CPI (EU Norm) Prelim YY (Nov) 1.1% vs. Exp. 1.3% (Prev. 1.3%)

- Italian CPI (EU Norm) Prelim MM (Nov) -0.2% vs. Exp. -0.1% (Prev. -0.2%)

- Italian Consumer Price Prelim YY (Nov) 1.2% vs. Exp. 1.3% (Prev. 1.2%)

- Italian Consumer Price Prelim MM (Nov) -0.2% vs. Exp. -0.1% (Prev. -0.3%)

- Italian GDP Final YY (Q3) 0.6% vs. Exp. 0.4% (Prev. 0.4%)

- Italian GDP Final QQ (Q3) 0.1%

Others

- Swiss GDP YY (Q3) 0.5% (Prev. 1.2%, Rev. 1.3%)

- Swiss GDP QQ (Q3) -0.5% vs. Exp. -0.4% (Prev. 0.1%, Rev.

GEOPOLITICS

RUSSIA-UKRAINE

- Ukrainian President Zelensky said Ukrainian and US delegations will meet this week to work out a formula for peace and security discussed in the Geneva talks.

- Russia's Kremlin says Russia wants to try move towards peace in Ukraine despite its belief that Ukrainian President Zelensky is not legitimate.

- Ukrainian Presidential top aide said should not count on them giving up territory as long as Zelensky is President.

- Belgium warned that using frozen Russian assets to fund Ukraine will endanger a peace deal, according to FT.

OTHERS

- US President Trump said regarding Venezuela that they will begin to stop drug cartels on land soon.

- Russian President Putin to visit India between December 4th-5th, according to IFX.

- Chinese Foreign Minister Wang Yi to visit Russia between December 1st-2nd.

APAC TRADE

- APAC stocks were rangebound in the absence of a lead from Wall Street due to Thanksgiving Day and as participants digest a deluge of data at month-end.

- ASX 200 lacked direction as strength in the tech, mining and the consumer sectors is counterbalanced by losses in financials, real estate and telecoms.

- Nikkei 225 traded indecisively amid a slew of data in which Industrial Production and Retail Sales topped forecasts, while Unemployment rose and Tokyo CPI printed mostly in line with estimates, aside from the firmer-than-expected core reading.

- Hang Seng and Shanghai Comp were mixed, albeit with trade confined to within relatively tight parameters, while China Vanke shares and bonds were volatile and initially continued to slump with its H shares hitting a record low amid the ongoing default concerns, before staging a notable recovery.

NOTABLE ASIA-PAC HEADLINES

- BoJ decided to increase the upper limit on the consecutive-day purchases of the same issue under the Securities Lending Facility (SLF) for 10-year JGBs from Dec 1st.

- Japan finalised JPY 18.3tln extra budget to fund stimulus package

- Samsung Electronics (005930 KS) appoints new CEO, Tae-Moon Roh.

- Meituan (3690 HK) Q3 (CNY): Revenue 95.5bln (exp. 97.5bln), Adj Net -16bln (exp. -13.96bln); sees operating loss trend to continue in Q4; market competition remained overheated recently.

DATA RECAP

- Taiwan Q3 GDP 8.2% Y/Y (prelim. 7.64%). Guidance: 2025 7.37% (prev. 4.45%), 2026 3.54% (prev. 2.81%)

- Japanese Unemployment Rate (Oct) 2.6% vs. Exp. 2.5% (Prev. 2.6%)

- Japanese Jobs/Applicants Ratio (Oct) 1.18 vs. Exp. 1.2 (Prev. 1.2)

- Japanese Industrial Production MM SA (Oct P) 1.4% vs. Exp. -0.6% (Prev. 2.6%)

- Japanese Industrial Production YY SA (Oct P) 1.5% vs. Exp. -0.5% (Prev. 2.0%)

- Japanese Retail Sales YY (Oct) 1.7% vs. Exp. 0.8% (Prev. 0.5%, Rev. 0.2%)

- Tokyo CPI YY (Nov) 2.7% vs Exp. 2.7% (Prev. 2.8%)

- Tokyo CPI Ex. Fresh Food YY (Nov) 2.8% vs Exp. 2.7% (Prev. 2.8%)

- Tokyo CPI Ex. Fresh Food & Energy YY (Nov) 2.8% vs Exp. 2.8% (Prev. 2.8%)