US Market Open: US and Ukraine negotiations were productive; US equity futures down and DXY pressured by stronger Yen

01 Dec 2025, 11:15 by Newsquawk Desk

- US and Ukraine negotiations on Sunday focused on where the de facto border with Russia would be drawn under a peace deal, while the five-hour meeting was said to be difficult and intense, but productive, according to two Ukrainian officials cited by Axios.

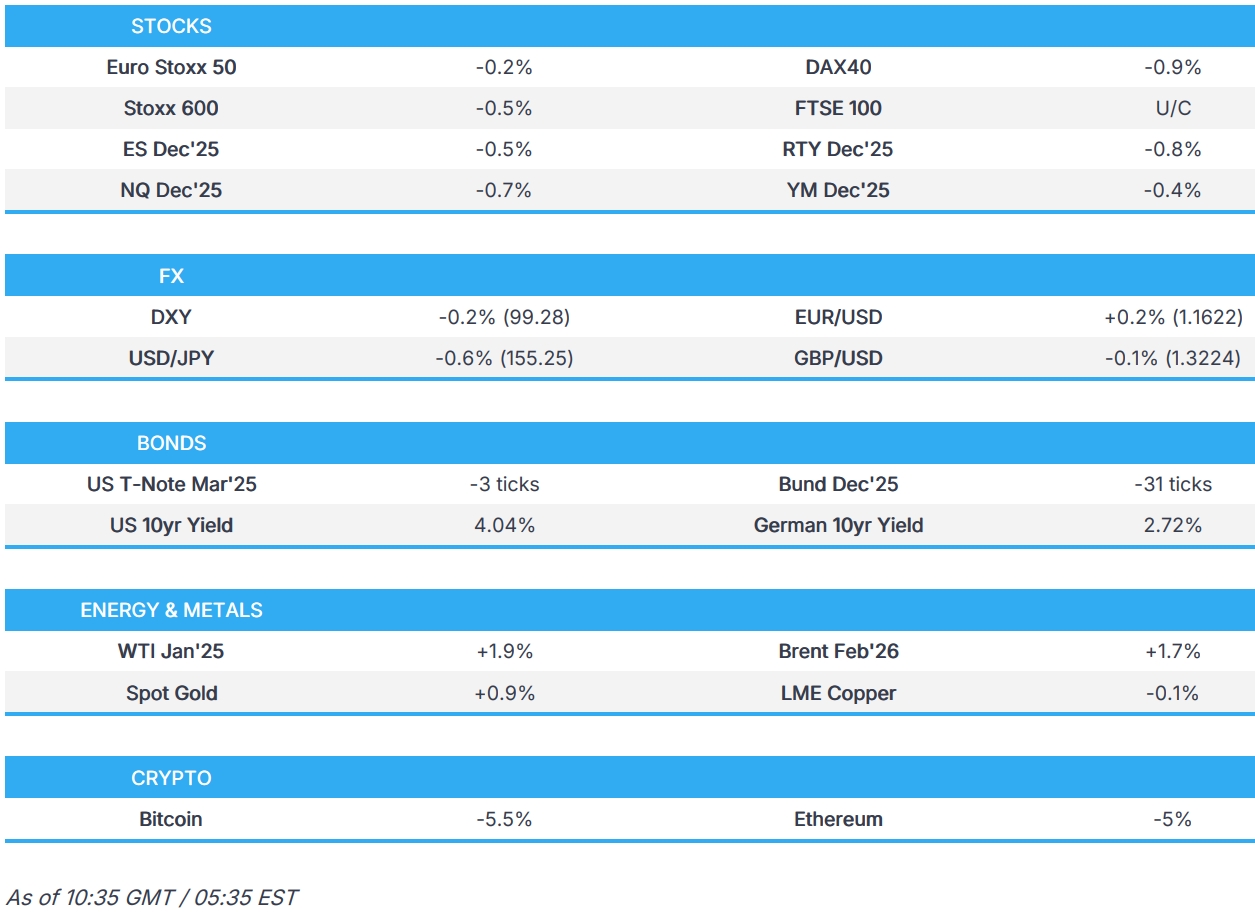

- European and US equity futures are broadly on the backfoot, following on from a cautious mood in APAC trade.

- DXY is pressured by the stronger JPY following jawboning from Japanese officials and after BoJ Governor Ueda hinted at a December rate hike.

- Bonds were initially pressured following on from JGB downside, and then took a leg lower alongside Gilt underperformance soon after the European cash open.

- Crude futures benefit after OPEC+ holds output steady through Q1’26 and in reaction to further Ukrainian strikes in Russian oil refineries; 3M LME Copper surges to fresh ATHs above USD 11.2k/t, but has since scaled back given the risk tone and downbeat Chinese PMI figures.

- Looking ahead, highlights include US Manufacturing PMI Final (Nov), US ISM Manufacturing PMI (Nov), Saudi-Russia Business Forum, EU Supply. Speak from Fed Chair Powell (Fed Blackout) and BoE's Dhingra.

EQUITIES

- European bourses (STOXX 600 -0.3%) are on the backfoot, following a cautious mood seen in APAC trade. The AEX (U/C) bucks the trend, with ASML (+1%) keeping the index afloat after positive analyst commentary.

- European sectors are mixed. Basic Resources leads, given the strength in underlying metals prices whilst Industrials sits at the foot of the pile, with Airbus (-3.5%) pressured after rolling out urgent fixes across its A320 fleet over the weekend.

- US equity futures are softer across the board (ES -0.5% NQ -0.7% RTY -0.8%), following the pressure seen in Europe. Focus later will be on US ISM Manufacturing figures, which will give further insight into the health of the US economy ahead of the FOMC meeting next week.

- Softbank (9984 JT) CEO said he did not want to sell a single NVIDIA (NVDA) share, but needed funds to invest in OpenAI and other opportunities.

- Swiss Government has filed charges against UBS' (UBSG SW) Credit Suisse for money laundering and organisational deficiencies, relating to Mozambican state-owned enterprise

- Click for the sessions European pre-market equity newsflow

- Click for the additional news

FX

- DXY is subdued in the presence of JPY strength and in the absence of any pertinent catalysts and with the Fed in a blackout period, while US President Trump said he knows who he will pick for the Fed chair role, but didn't give any further details. DXY resides towards the bottom of a 99.26-99.51 range (vs Friday's 99.38-99.82 parameter), with the next downside level the 17th November low at 99.25.

- JPY is the marked outperformer this morning, given the risk tone and commentary from BoJ Governor Ueda, who ultimately hinted at a possible December rate rise, although market pricing has been little changed since last week, with a 67% chance of a hold at the 19th December announcement. USD/JPY currently resides towards the bottom of a 155.24-156.15 parameter, the next support level is seen at 155.21 (19th November low).

- EUR and GBP diverge, the former underpinned by the USD, whilst the latter is subdued ahead of UK PM Starmer's speech at 10:30GMT, where he will reportedly outline the growth mission and will defend the Budget after Chancellor Reeves was forced to deny lying to the public about UK finances pre-Budget. No moves were seen in EUR or GBP on the Final Manufacturing PMI data. EUR/GBP reached a 0.8794 peak vs a 0.8754 intraday trough.

- Non-US dollars, CAD, AUD, NZD, are relatively flat with the broader market tone tentative and macro updates light. Upside capped in the antipodeans following overall disappointing Chinese PMIs, where the headline official Manufacturing PMI continued to show a decline in factory activity at 49.2 (exp. 49.2) and Non-Manufacturing disappointed with a surprise contraction at 49.5 (exp. 50.0), while RatingDog Manufacturing PMI missed estimates at 49.9 (Exp. 50.5).

- PBoC set USD/CNY mid-point at 7.0759 vs exp. 7.0709 (Prev. 7.0789).

- Click for NY OpEx Details

FIXED INCOME

- USTs Mar'26 down to 113-06, lower by five ticks at worst. Downside echoes peers, but offset by dovish Fed expectations as markets near-enough price a December cut, and we look to updates on the next Fed Chair after President Trump said he knows who he will pick. Polymarket ascribes a 58% chance that Hassett will be appointed. Treasury Secretary Bessent recently said Trump could make an announcement pre-Christmas.

- Bund Dec'25 at a 128.50 low, posting downside of 37 ticks. Support comes into play at 128.37 from the 20th of November. Thereafter, the figure before 127.88 from the last week of September. JGBs and Gilts (see below) driving much of the bearishness, alongside upside in numerous Commodity prices, and particularly crude post-OPEC.

- Gilts Mar'26 opened lower by 12 ticks before falling further to a 91.16 low with downside of 42 ticks at most. Underperformance driven by the Budget and Chancellor Reeves coming under scrutiny over the weekend, with particular reference to the timing of OBR briefings and her pitch-rolling on Income Tax. PM Starmer to speak at 10:30GMT on growth.

- JGBs Dec'25 hit overnight and were lower by c. 50 ticks at worst. Pressure on the back of hawkish BoJ commentary, where Ueda, among other points, said that delaying a rate hike too long could cause sharp inflation and force a rapid policy adjustment. Remarks that lifted BoJ pricing to over a 70% chance of a hike in December vs sub-60% on Friday.

COMMODITIES

- WTI and Brent are currently trading higher by c. 2%, as markets digest the OPEC+ and supply-related concerns following Ukraine’s attack on Russian refineries. WTI and Brent currently reside at the upper end of a USD 58.83/bbl to USD 59.97/bbl and USD 62.29/bbl to 63.35/bbl range respectively. Price action since the European cash open has been exceptionally lacklustre, and generally sideways around highs; some modest downticks have been seen in recent trade.

- Spot gold is firmer today and trades towards the upper end of a USD 4,205.63/oz to USD 4,262/oz range. XAU now at levels not seen since late October 2025; there is now a bit of clear air to the high of 21st October at USD 4,375.62/oz. Perhaps some focus on continued Ukrainian attacks on Russia, as traders now focus on the coming meeting between US Special Envoy Witkoff and Russian President Putin on Tuesday. Elsewhere, marked pressure in the crypto space perhaps sent flows to the more-traditional haven in APAC trade.

- Base metals held a strong positive bias throughout overnight trade, but then gave up some of the upside as the risk tone dipped a touch, with traders focusing on the disappointing Chinese PMI metrics. Focus has also been on the surge in 3M LME Copper, which saw the red-metal surge above USD 11.2k/t to print a fresh ATH at USD 11,297/t, before scaling back down to a current USD 11,189/t. ING opines that the latest bout of demand for the metal is thanks to “an upbeat CESCO Week event in Shanghai” – suggesting that it echoed the markets’ view of tight supply.

- OPEC+ agreed to keep group-wide oil output unchanged for Q1 2026, while it stated that participating countries approved the mechanism developed by the secretariat to assess participating countries’ maximum sustainable production capacity. Furthermore, it announced that the 41st OPEC and Non-OPEC ministerial meeting will be held on 7th June 2026.

- OPEC Secretariat receives update compensation plans from Iraq, the UAE, Kazakhstan, and Oman, according to a statement.

- Saudi Energy Minister said OPEC+ latest decision is the most important and transparent in deciding production level via State TV.

- Gas exports from Iraq's Khor Mor gas field resumed just days after a drone attack.

NOTABLE DATA RECAP

- EU HCOB Manufacturing Final PMI (Nov) 49.6 vs. Exp. 49.7 (Prev. 49.7)

- Spanish HCOB Manufacturing PMI (Nov) 51.5 vs. Exp. 52.4 (Prev. 52.1)

- German HCOB Manufacturing PMI (Nov) 48.2 vs. Exp. 48.4 (Prev. 48.4)

- French HCOB Manufacturing PMI (Nov) 47.8 vs. Exp. 47.8 (Prev. 47.8)

- Italian HCOB Manufacturing PMI (Nov) 50.6 vs. Exp. 50.3 (Prev. 49.9)

- UK S&P Global Manufacturing PMI (Nov) 50.2 vs. Exp. 50.2 (Prev. 50.2)

NOTABLE EUROPEAN HEADLINES

- Swiss voters overwhelmingly rejected the proposal for a 50% inheritance tax for the super-rich, according to FT.

- UK PM Starmer and Chancellor Reeves have been accused of misleading the Cabinet by using claims that there was a black hole in the public finances to justify tax rises during the run-up to the Budget, according to The Times’s Swinford, while it was separately reported by Bloomberg that Reeves denied lying about UK finances pre-Budget.

- UK PM Starmer is to defend the Budget after Reeves was accused of misleading the public, and will outline the growth mission after the Budget tax rises during a speech on Monday.

- S&P affirmed Latvia at A; Outlook Stable and affirmed Lithuania at A; Outlook Stable.

- ECB's de Guindos said the current level of interest rates is appropriate and, in terms of future moves, this is data dependent.

NOTABLE US HEADLINES

- US President Trump said on Friday he is cancelling all executive orders signed by former President Biden using autopen and stated that any document signed by Biden with autopen, which was approximately 92% of them, is hereby terminated and of no further force or effect. Furthermore, Trump stated that Biden was not involved in the autopen process and that if he said he was, he will be brought up on charges of perjury.

- US President Trump said he knows who he will pick as the next Fed chair.

- White House Economic Adviser Hassett said he will be happy to serve if US President Trump picks him as Fed chair.

- US State Department announced a pause on visa issuances for Afghan passport holders, and the US immigration service said it will halt all asylum decisions, while the US Citizenship and Immigration Services Director said USCIS halted all asylum decisions until they can ensure that every migrant is vetted and screened to the maximum degree.

- US Transportation Secretary Duffy said they have been in close contact with Airbus (AIR FP) about the software update recall for the A320 and the airlines that use them, as well as noted that travellers should not expect any major disruptions. It was also reported that Airbus was revising down the number of jets affected by the most time-consuming A320 repairs, while American Airlines said planes impacted by the Airbus glitch have been fixed.

- Mastercard SpendingPulse noted that US retail spending on Black Friday rose 4.1% Y/Y and ecommerce spending rose 10.4% Y/Y, while Adobe Analytics noted that consumer spending rose 9.1% Y/Y to a record USD 11.7bln on Black Friday.

- CyrusOne said it restored stable and secure operations at its Chicago 1 data centre in Aurora, Illinois.

- South African President Ramaphosa dismissed US President Trump's threat to exclude the country from next year's G20 summit and reaffirmed South Africa's status as a founding member of the group, according to Reuters.

- "It is exceedingly unlikely that the White House will embrace an ACA subsidies extension or offer its own plan", according to Punchbowl citing Trump admin sources.

GEOPOLITICS

MIDDLE EAST

- Israeli PM Netanyahu submitted a letter to President Herzog, while Netanyahu said in a video statement addressing the pardon request that his personal interest was to complete the legal process until the end, while he added that the military and national reality, and national interest, demand otherwise, and that ending the trial immediately would advance much-needed national reconciliation.

- Israeli helicopters fired in the eastern areas of Khan Yunis inside the Yellow Line, according to Al Jazeera.

- Israeli security estimates that Iran may take the initiative and carry out retaliatory operations instead of Hezbollah and estimates preparations for a Houthi response in retaliation for the killing of Hezbollah Top Commander Al-Tabatabai, according to Al Arabiya.

- Hezbollah’s leader said on Friday in response to Israel's killing of its military chief that the group has a right to respond and will set a time for it, while he added that Lebanon's government should prepare a plan to confront Israel.

- Iran’s Foreign Minister Araghchi held talks with Turkey regarding the nuclear issue and Israel, while he also held a meeting with the Saudi Deputy Foreign Minister for Political Affairs in Tehran.

RUSSIA-UKRAINE

- Russia's Kremlin said that Russian President Putin is due to meet US envoy Witkoff on Tuesday. On the Russia-Ukraine peace development, the Kremlin adds that they are not going to engage in megaphone diplomacy.

- Ukrainian President Zelensky said a delegation headed by the security council chief travelled to the US for talks, while it was also reported that Zelensky is to visit French President Macron in Paris on Monday.

- US and Ukraine negotiations on Sunday focused on where the de facto border with Russia would be drawn under a peace deal, while the five-hour meeting was said to be difficult and intense, but productive, according to two Ukrainian officials cited by Axios.

- US Secretary of State Rubio said the meeting with Ukrainians was very productive but noted there is more work to be done, while he added that they have been in touch to varying degrees with the Russian side.

- Ukraine’s First Deputy Foreign Minister said there was a good start to US peace talks with a warm atmosphere conducive to a potential progressive outcome.

- Ukraine’s military hit Russia’s Afipsky oil refinery, while it was also reported that Ukrainian sea drones struck two Gambia-flagged tankers off the Turkish coast on Friday, which were said to be part of a Russian shadow fleet used to bypass Western sanctions.

- Russian forces carried out a massive strike on Ukrainian military-industrial and energy facilities.

- Russia’s Foreign Minister said following a Ukrainian drone attack on the CPC Black Sea terminal, that the civilian energy infrastructure that was attacked plays an important role in ensuring global energy security and has never been subject to any restrictions or limitations, while they strongly condemned the ‘terrorist attacks’ on CPC and oil tankers.

- NATO is considering being “more aggressive” in responding to Russia’s cyber-attacks, sabotage and airspace violations, according to its most senior military officer, Admiral Giuseppe Cavo Dragone, cited by FT.

- NATO is reportedly preparing for the scenario of confronting Russia with limited US support, according to a report by Bloomberg citing a wargame in Transylvania that showed European soldiers defending the continent largely without US support as President Trump reduces US deployments in Europe.

OTHER

- US President Trump declared on Truth Social that the airspace above Venezuela is closed. It was separately reported that President Trump held a call with Venezuelan President Maduro, while Trump also commented that Defence Secretary Hegseth told him that he did not order a second boat strike.

- US bipartisan lawmakers raised alarms on Sunday that Defence Secretary Hegseth may have committed a war crime following a report that he ordered a follow-on attack to kill survivors of a boat strike in September, according to POLITICO.

- Venezuela said it rejects US President Trump’s “hostile, unilateral and arbitrary” post about Venezuela’s airspace and noted that the statement shows “colonial pretentions” towards Latin America, while it added that Venezuela demands respect for airspace and will not accept foreign orders or threats.

- China’s Coast Guard carried out law enforcement inspections around the Scarborough Shoal, while the report noted that the Chinese military’s Southern Theatre Command organised combat readiness patrols in the ‘territorial’ waters and airspace of the Scarborough Shoal and surrounding areas on November 29th, according to Xinhua.

CRYPTO

- Bitcoin sank overnight and continues to remain on the backfoot, below USD 86.6k whilst Ethereum slips below USD 2.9k.

APAC TRADE

- APAC stocks began the new month mixed, with participants cautious as they digested the weak Chinese PMI data.

- ASX 200 was dragged lower by weakness in healthcare, telecoms, financials and tech, while sentiment was also not helped by disappointing Chinese PMI data and weaker-than-expected Australian Gross Company Profits and Business Inventories.

- Nikkei 225 slipped beneath the 50k level amid a firmer currency and risks of a BoJ rate hike in December, while there were hawkish-leaning comments from BoJ Governor Ueda, who said that they will consider the pros and cons of raising rates at the December meeting.

- Hang Seng and Shanghai Comp were kept afloat despite the discouraging Chinese PMI data, in which the headline official Manufacturing PMI continued to show a decline in factory activity at 49.2 (exp. 49.2) and Non-Manufacturing disappointed with a surprise contraction at 49.5 (exp. 50.0), while RatingDog Manufacturing PMI missed estimates at 49.9 (Exp. 50.5).

NOTABLE ASIA-PAC HEADLINES

- BoJ Governor Ueda is to deliver a speech at the Japan Business Federation on December 25th, according to the central bank.

- BoJ Governor Ueda said if their projection of economic activity and prices materialise, the BoJ will continue to raise the policy interest rate in accordance with improvements in economy and prices, while he added that even if the policy interest rate is raised, accommodative financial conditions will be maintained and the likelihood of their baseline scenario for economic activity and prices being realised is gradually increasing. Ueda also commented that at the December meeting, the BoJ will examine and discuss economic activity and prices at home and abroad, as well as market developments, based on various data, and consider the pros and cons of raising rates. Furthermore, he said it is important for FX to move stably reflecting fundamentals and that a weak yen works to push up consumer inflation, while they must be mindful that FX moves affect inflation expectations and underlying inflation in guiding policy.

- Japanese Finance Minister Katayama said it is “clear” that volatile swings in the FX market and the rapid weakening of the yen aren’t based on fundamentals.

- China’s financial regulator guides banks and insurers to fully provide financial support services related to the Hong Kong fire and said insurance institutions should promptly handle claims and other procedures for disaster-affected customers, while it added that banks should strengthen financial credit support and actively assist in disaster reconstruction.

- Indonesia said at least 303 people died in three provinces after severe rains caused floods and landslides.

- Vanke has reportedly requested 12-months to pay its bonds under the extension plan, Bloomberg reports.

DATA RECAP

- Chinese NBS Manufacturing PMI (Nov) 49.2 vs. Exp. 49.2 (Prev. 49.0)

- Chinese NBS Non-Manufacturing PMI (Nov) 49.5 vs Exp. 50.0 (Prev. 50.1)

- Chinese NBS Composite PMI 49.7 (Prev. 50.0)

- Chinese RatingDog Manufacturing PMI Final (Nov) 49.9 vs. Exp. 50.5 (Prev. 50.6)