US Market Open: Stateside set to open modestly higher; no reaction to EZ HICP

02 Dec 2025, 11:20 by Newsquawk Desk

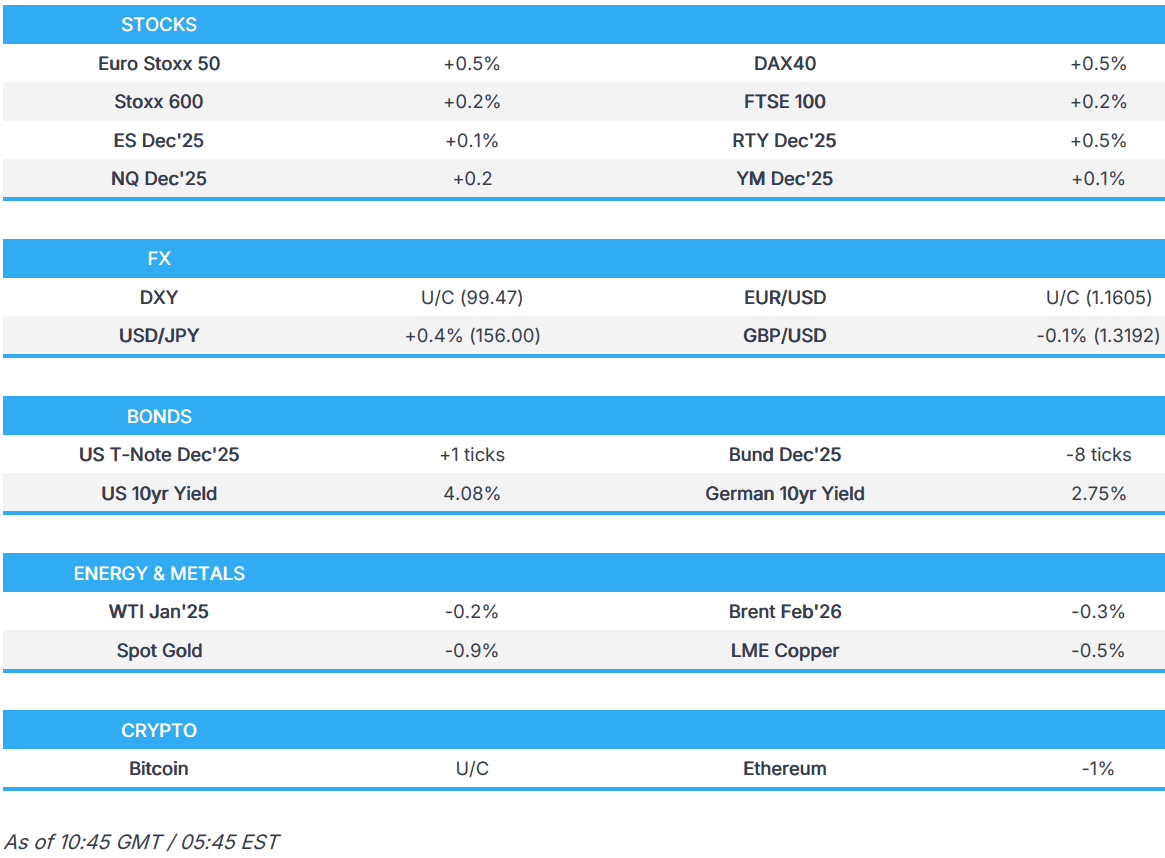

- European bourses started the morning flat/modestly firmer, but have since sauntered to session highs; US equity futures also modestly firmer.

- OpenAI CEO Altman declares a code red to combat threats to ChatGPT and plans to delay other initiatives such as advertising, according to The Information.

- DXY is modestly firmer, AUD initially outperformed after ANZ scaled back rate cut bets for 2026, but is now flat amidst USD-strength, USD/JPY rises back towards 156.00.

- Bonds are flat/modestly lower, Bunds little moved to EZ HICP whilst Gilts lag.

- Crude essentially flat in rangebound trade, XAU slips below USD 4.2k/oz.

- Looking ahead, highlights include US RCM/TIPP Economic Optimism, Earnings from Marvell & CrowdStrike.

TARIFFS/TRADE

- Chinese rare-earth magnet companies are reportedly finding workarounds to their government’s export restrictions, as they seek to keep sales flowing to Western buyers, according to WSJ.

- China reportedly issues first rare earth magnet general export licence after the Trump-Xi meeting, according to Reuters sources

- Exxon (XOM) is reportedly in talks with Iraq over purchasing Lukoil's stake in the West Qurna 2 oilfield, via Reuters citing sources.

- Russia's Kremlin Spokesperson Peskov says that Russia continues to be an important supplier of energy to India on a competitive basis. Looking at possibilities to increase imports from India. A decrease in oil trade volumes can be decreased for a brief period of time.

EUROPEAN TRADE

EQUITIES

- European bourses (STOXX 600 +0.2%) started the session flat/incrementally firmer before then catching a bid as the morning progressed; no clear driver for the upside, but a move which has sustained as indices reside near peaks.

- European sectors hold a slight positive bias. Banks take the top spot, with gains broad-based across the UK and Europe, but traders may also be digesting the latest update via the BoE, where it lowered capital requirements for UK banks as they pass stress tests. Media is found at the foot of the pile, joined closely by Travel & Leisure.

- US equity futures (ES +0.1% NQ +0.2% RTY +0.5%) initially mildly lower but then moved modestly into the green alongside the strength seen in Europe. The focus this morning has been on OpenAI's Altman, who declared a "code red", as he sees a rising threat to ChatGPT from Google.

- BNP Paribas sees end-2026 S&P 500 at 7,500 (vs 6,812.63 Monday close), sees end-2026 Stoxx 600 at 650 (vs current 576.04).

- US FDA is to stop requiring pharmaceutical firms to use primates for some safety studies, via FT.

- Click for the sessions European pre-market equity newsflow

- Click for the additional news

FX

- DXY and most G10 FX are uneventful in relatively quiet trade, with a similar lack of macro drivers seen during APAC hours. Specifically, DXY resides in a narrow 99.38-99.52 parameter, with ING calling for a lower dollar this week - "we expect that the remainder of the week will validate the market’s dovish pricing for next week’s Fed meeting". As it stands, the index trades at the upper end of the mentioned ranges, with recent strength thanks to some pressure seen in the GBP.

- EUR traded flat ahead of the EZ HICP metrics, and then was little moved on the release itself. Headline printed a touch above expected at 2.20% (exp. 2.10%) whilst the Services figure also ticked higher from the prior month. Overall, given the figures were near enough in line with expectations, there was little follow-through into the single-currency and held within a 1.1604 to 1.1616 range, before then touching 1.1600 as the USD picked up a touch.

- USD/JPY outperforms amid a pick-up in risk sentiment and after the pair's volatile Monday session, which saw a slump to 154.66 lows before bouncing back up and clear of 155.50 and then 156.00, with the pair eyeing yesterday's 156.15 peak as the near-term resistance level, and thereafter Black Friday's 156.58 high.

- GBP traded flat against the USD, before then moving lower in recent trade. Nothing behind the latest bout of pressure, but it does come after Cable breached 1.3200 to the downside, and then continued to tumble to make a fresh trough at 1.3180 (though it is a moving target).

- AUD outperforms after ANZ removed its call for an RBA cut in H1-2026, now sees the RBA on an "extended pause" through 2026. As a reminder, CBA and NAB also expect the RBA to be on hold for an extended period of time/foreseeable future. Westpac continues to expect two 2026 cuts, touting May and August for those. AUD/NZD marginally eclipsed 1.1450, from a 1.1418 trough.

- PBoC set USD/CNY mid-point at 7.0794 vs exp. 7.0746 (Prev. 7.0759)

FIXED INCOME

- A lack of fresh drivers for USTs. The March contract is near-enough flat in a narrow 112-25 to 112-29 band. Overnight, WSJ's Timiraos wrote that, regarding the search for the next Fed Chair, "Unofficially, the process seems to be all but over, with President Trump appearing to favour longtime adviser Kevin Hassett.".

- Bund Dec'25 is contained in a thin 128.18-35 band this morning. Specifics light. No move in Bunds on the EZ Flash HICP for November, the headline came in hotter-than-expected and ticked up from the prior, while Services lifted from the previous rate. Overall, the hotter-than-expected series chimes with the view that the ECB's easing cycle has likely concluded.

- Gilts underperform. If the move continues, we look to support for the Gilt Mar'26 contract at 90.53, a double-bottom from the session of and before the Budget. Currently, the low is 90.98, taking out Monday's base by a tick. A move that lifted the UK 10yr yield back above the 4.5% mark. However, this pressure proved somewhat fleeting as the benchmark bounced and has made its way back to the unchanged mark. Nothing fresh, though the OBR briefing is underway and we note remarks from BoE officials on the morning's FSR/FPC briefings.

- Saudi National Bank is seeking a USD 1bln syndicated loan, via Bloomberg. Loan is being syndicated to the broader market, incl. Asia, according to sources cited.

- JGB's led overnight after a strong 10yr auction and in a bit of a breather from the largely Ueda-induced selling seen at the start of the week. To a 134.72 peak with gains of just over 20 ticks at best.

- UK sells GBP 1bln 0.125% 2031 I/L Gilt: b/c 3.88x (prev. 3.49x), real yield 0.949% (prev. 0.889%)

- Germany sells EUR 3.563bln vs exp. EUR 4.5bln 2.00% 2027 Schatz: b/c 1.7x (prev. 1.7x), average yield 2.05% (prev. 1.98%), retention 20.82% (prev. 24.68%)

COMMODITIES

- WTI and Brent continue to trade within Monday's post-OPEC range of USD 58.83-59.97/bbl and USD 62.69-63.82/bbl, respectively, as a pause in output hike and rising geopolitical concerns continue to support crude prices in the near term. WTI and Brent peaked at the start of the APAC session at USD 59.67/bbl and 63.36/bbl before falling to troughs of 59.09/bbl and 62.88/bbl.

- XAU and XAG traded muted at the start of the European session. Oscillated in a tight USD 4201-4236/oz and USD 56.60-58/oz band, respectively. More recently, the yellow metal has fallen to make fresh session troughs of USD 4,181/oz - a move which lacked catalysts, but technicians highlight accelerating selling pressure after spot gold slipped below USD 4.2k/oz.

- 3M LME Copper gapped lower and fell to a trough of USD 11.12k/t before rebounding to a session high of USD 11.27k/t as global risk tone slightly turns around following Monday's selloff.

NOTABLE DATA RECAP

- EU HICP Flash YY (Nov) 2.2% vs. Exp. 2.1% (Prev. 2.1%); Services 3.5% (prev. 3.4%); HICP Excluding Food & Energy Flash YY (Nov) 2.40% (Prev. 2.40%)

- EU Unemployment Rate (Oct) 6.4% vs. Exp. 6.3% (Prev. 6.3%, Rev. 6.4%)

- UK BRC Shop Price Index YY (Nov) 0.6% (Prev. 1.0%)

- French Budget Balance (Oct) -136.17B (Prev. -155.4B)

- Hungarian GDP YY Final (Q3) 0.6% (Prev. 0.6%)

- UK Nationwide house price mm (Nov) 0.3% vs. Exp. 0.1% (Prev. 0.3%, Rev. 0.2%)

- UK Nationwide house price yy (Nov) 1.8% vs. Exp. 1.4% (Prev. 2.4%)

- Germany's VDMA says that engineering orders have risen 4% in October Y/Y, and engineering orders have fallen 6% in Aug-Oct period.

- Italian Unemployment Rate (Oct) 6.0% vs. Exp. 6.1% (Prev. 6.1%, Rev. 6.2%)

NOTABLE EUROPEAN HEADLINES

- Confederation of British Industry said Britain's private sector expects output to decline during the next three months in the gloomiest outlook since May as cautious consumer spending and cost pressures continue to weigh on businesses.

- BoE Financial Policy Committee Record: System-wide level of Tier 1 capital requirements is now around 13% of risk-weighted assets, 1ppt lower than its previous benchmark of around 14%. CCyB maintained at 2%. "The Committee has also identified areas for further work, including on buffer usability, the implementation of the leverage ratio in the UK, and initiatives by the Bank to respond to feedback on interactions, proportionality, and complexity. Committee supports the Bank’s plans for a private markets system-wide exploratory scenario (SWES)".

- OECD sees global growth of 3.2% in 2025 (maintained from prev. forecast), 2.9% in 2026 (maintained), 3.1% in 2027 (new forecast).

- UK OBR's Miles says it was not misleading for Chancellor Reeves to have said that the situation with public finances was very challenging.

- BoE Governor Bailey says he expects banks to support the economy through lending following recent capital changes.

NOTABLE US HEADLINES

- President Trump's schedule noted he will host a Cabinet meeting on Tuesday at 11:30EST/16:30GMT and will make an announcement at 14:00EST/19:00GMT.

- Fed Vice Chair of Supervision Bowman said it is important to finish Basel III, while she added they are working on a G-SIB surcharge.

- OpenAI's Altman has declared a "code red" effort to enhance the quality of ChatGPT, via WSJ, citing an internal memo. Co. is delaying other products to do this. Alphabet's (GOOGL) Google Gemini AI is of particular concern to Altman.

- Apple (AAPL) plans not to follow the order by the Indian government to preload phones with a state-run cyber safety app, according to Reuters, citing sources; Co. to voice its concerns around privacy and security following new app order

GEOPOLITICS

MIDDLE EAST

- Arab media reported new Israeli attacks in Khan Yunis and Rafah, according to Iran International.

RUSSIA-UKRAINE

- European Commission proposals for the Ukraine reparation loan should be distributed to member states tomorrow, and likely first discussion by EU ambassadors on Friday, according to Radio Liberty journalist

- Russian Foreign Minister Lavrov is to meet with Chinese Foreign Minister Wang Yi on Tuesday.

- Russia's Kremlin Spokesperson Peskov says US Special Envoy Witkoff and President Putin will discuss the understanding reached between the US and Ukraine, in a meeting at 14:00GMT/09:00EST, via TASS. S-400 and SU-57 fighter jets will be on the agenda.

OTHER

- Venezuelan President Maduro reportedly asked for sanction removal for more than 100 officials during a previous call with US President Trump. Furthermore, Trump gave Maduro a Friday deadline to leave Venezuela with his family, while the failure to meet the Friday deadline prompted Trump's comments on Saturday about the closure of airspace, according to sources cited by Reuters.

- US Treasury Secretary Bessent said the Treasury is investigating allegations that Minnesota tax dollars may have been diverted to Al-Shabaab.

- China's Coast Guard said it expelled a Japanese vessel in the waters of the Senkaku Islands on Tuesday.

- "Turkey says oil tanker attacked in Black Sea while sailing from Russia to Georgia", according to Sky News Arabia. However, Sky News Arabia later clarifies, "Turkey says cargo ship attacked in Black Sea while sailing from Russia to Georgia".

- Japan's Defence Minister Koizumi is considering a visit to the US as early as mid-January to hold talks with War Secretary Hegseth, via Kyodo.

CRYPTO

- Bitcoin is essentially flat and trades just above USD 86k.

APAC TRADE

- APAC stocks were predominantly in the green as the region shrugged off the weak lead from Wall Street, but with the upside capped amid quiet macro catalysts and in the absence of any tier-1 data.

- ASX 200 eked mild gains with the help of outperformance in energy, resources and mining, but with gains limited by underperformance in tech and utilities, while data was uninspiring with a larger-than-expected contraction in building approvals.

- Nikkei 225 nursed some of the prior day's losses but with the rebound contained amid risks of a BoJ December hike.

- Hang Seng and Shanghai Comp mostly traded mixed as participants reflected on a slew of monthly auto sales updates, while the mainland lagged after the PBoC's open market operations resulted in a net daily drain of CNY 146bln.

NOTABLE ASIA-PAC HEADLINES

- RBNZ Governor Breman said she will discuss with the MPC the possibility of being more transparent with how members vote, while she added that the mandate is very clear that we should focus on keeping inflation low and stable. Breman said that they aim to support a healthy, strong and growing economy, but keep inflation low and stable. It was separately reported that the RBNZ is to begin weekly open-market operations from December 4th and will update changes to the format in Q1 2026.

- Samsung Electronics (005930 KS) has completed development of its 6th-gen HBM4 and is entering full-scale mass production, via AJUNews.

DATA RECAP

- Australian Current Account Balance (AUD)(Q3) -16.6B vs. Exp. -13.3B (Prev. -13.7B)

- Australian Net Exports Contribution (Q3) -0.1% vs. Exp. -0.1% (Prev. 0.1%)

- Australian Building Approvals (Oct) -6.4% vs. Exp. -4.5% (Prev. 12.0%, Rev. 11.1%)