EU Market Open: European equities to open in the green; Choppy APAC trade following hawkish BoJ sources

04 Dec 2025, 07:02 by Newsquawk Desk

- The Trump admin is reportedly preparing to hold a high-level meeting to decide whether to provide licenses to allow NVIDIA (NVDA) to export the H200 to China, according to FT.

- US President Trump said the meeting between Russian President Putin, Special Envoy Witkoff and Kushner was a reasonably good meeting and "we'll see what happens".

- Trump's aides and allies were said to be discussing the possibility of Treasury Secretary Bessent also leading the NEC, according to Bloomberg; Bond investors reportedly warned the US Treasury over picking NEC Director Hassett as Fed chair, according to FT.

- USD/JPY pared gains after hawkish BoJ sources via Reuters suggested the central bank is likely to raise interest rates in December.

- APAC stocks were mostly higher following the positive momentum from Wall Street; European equity futures indicate a positive cash market open with Euro Stoxx 50 futures up 0.6% after the cash market closed with gains of 0.2% on Wednesday.

- Looking ahead, highlights include Swedish CPIF, EZ Retail Sales, US Challenger Layoffs, Jobless Claims, Revelio Public Labor Statistics, Chicago Fed Labour Market Indicators (Final), Durable Goods, Factory Orders, Atlanta Fed GDP, BoE DMP. Speakers include BoEʼs Mann, ECBʼs Lane, Cipollone & de Guindos, Fedʼs Bowman. Supply from Spain, France & UK. Earnings from Kroger & Dollar General.

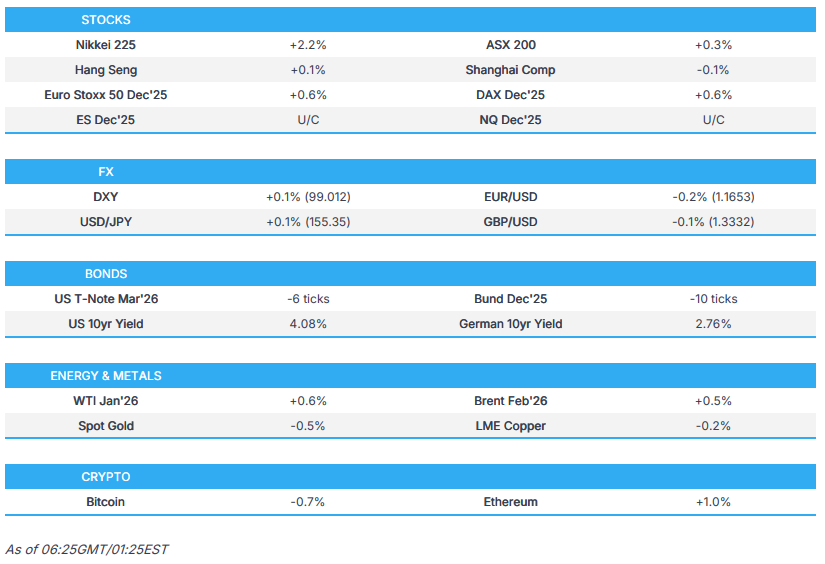

SNAPSHOT

US TRADE

EQUITIES

- US stocks trended higher throughout the session, although futures were initially knocked on reports in the Information that Microsoft (MSFT) is lowering AI software quotas as multiple sales teams failed to hit quotas for AI product sales last year, which hit MSFT and other AI names in the pre-market. However, stocks had started to pare before accelerating once MSFT denied the story and equities moved higher throughout the US session. The advances were led by the Russell 2000, while most sectors gained with outperformance in energy and financials, although tech and utilities closed in the red.

- SPX +0.30% at 6,850, NDX +0.20% at 25,607, DJI +0.86% at 47,883, RUT +1.91% at 2,512.

- Click here for a detailed summary.

TARIFFS/TRADE

- US President Trump said they will either let the USMCA expire or maybe work out another deal with Mexico and Canada.

- US halted plans to sanction the Chinese spy agency to maintain the trade truce, and the Trump administration will also not enact any major new export controls against China, while the Trump admin is preparing to hold a high-level meeting to decide whether to provide licenses to allow NVIDIA (NVDA) to export the H200 to China, according to FT.

- NVIDIA (NVDA) CEO Huang said he met with US President Trump and discussed export controls generally in the meeting, while he supports export controls. Furthermore, Huang said they can't degrade chips that they sell to China, and he does not know if China would accept H200 chips.

NOTABLE HEADLINES

- US President Trump proposed to drastically slash fuel economy requirements through 2031, with the US proposing to require 34.5mpg average fuel economy by 2031, down from 50.4mpg under Biden rules, while it was separately reported that President Trump said they will have a big percentage of the chip market very soon.

- US President Trump's aides and allies were reportedly discussing the possibility of Treasury Secretary Bessent also leading the National Economic Council, according to Bloomberg.

- US President Trump's administration ordered an enhanced vetting of H-1B visa applicants, with new H-1B visa screening based on any involvement in censorship or free speech, according to the State Department memo.

- US Senate Democrats are expected to offer a three-year clean extension of Obamacare subsidies for next week’s health care vote in the Senate, which would align them with House Democrats who are pushing the same plan, according to sources cited by Punchbowl.

- Bond investors reportedly warned the US Treasury over picking NEC Director Hassett as Fed chair, according to FT. Some market participants were worried the candidate for the top central bank job would be swayed by President Trump on interest rates and were worried that Hassett could agitate for indiscriminate rate cuts even if inflation continues to run above the Fed’s 2% target, according to three people familiar with the conversations.

APAC TRADE

EQUITIES

- APAC stocks were mostly higher following the positive momentum from Wall Street, where all major indices rose amid a weaker dollar and softer yield environment, but with some of the gains in the region capped amid a quiet calendar and lack of major fresh macro catalysts.

- ASX 200 edged higher in rangebound trade with strength in materials and resources offsetting the losses in the real estate and consumer sectors, while the mining industry was among the outperformers aside from the gold-related stocks.

- Nikkei 225 rallied above the 50k level as the tech-related momentum in Japan continued, despite higher yields and bets for a December BoJ rate hike.

- Hang Seng and Shanghai Comp were mixed amid weakness in auto names and after another liquidity drain by the PBoC, while PBoC Governor Pan noted in an Op-Ed that China must maintain prudent monetary policy and should avoid excessive policy adjustments.

- US equity futures paused overnight after climbing throughout most of the US trading session.

- European equity futures indicate a positive cash market open with Euro Stoxx 50 futures up 0.6% after the cash market closed with gains of 0.2% on Wednesday.

FX

- DXY found some mild respite after suffering yesterday amid the prospect of a more dovish Fed Chair in 2026 and following the mixed data releases in which ADP printed at a surprise contraction but ISM Services PMI beat on the headline, while there are more data releases scheduled ahead including US Challenger Layoffs, Jobless Claims, Revelio Public Labor Statistics, Chicago Fed Labour Market Indicators, Durable Goods and Factory Orders.

- EUR/USD was rangebound but held on to most of the prior day's spoils after benefitting from the recent dollar weakness, while the latest comments from ECB officials did little to shift the dial, including Lagarde who stated growth in economic activity should benefit from increased household spending and a resilient, more inclusive labour market, as well as noted they are not pre-committing to a particular rate path.

- GBP/USD slightly eased back after outperforming yesterday amid strength in cyclical currencies and firm UK Services PMI.

- USD/JPY initially rebounded from a trough near the 155.00 level, with the recovery helped by the outperformance in Japan. The pair later pared gains after hawkish BoJ sources suggested the central bank is likely to raise interest rates in December.

- Antipodeans were contained amid a lack of tier-1 data and with headwinds in CNH after the PBoC set a weaker-than-expected yuan fix.

- PBoC set USD/CNY mid-point at 7.0733 vs exp. 7.0554 (Prev. 7.0754)

FIXED INCOME

- 10yr UST futures traded subdued after recent oscillations, which coincided with mixed US data releases and expectations of a more dovish Fed Chair next year, while it was reported that some bond investors warned the US Treasury over picking NEC Director Hassett for the top Fed job.

- Bund futures struggled for direction amid a lack of pertinent catalysts and ahead of Eurozone Retail Sales data.

- 10yr JGB futures retreated amid increased bets of a BoJ December rate hike, with money markets pricing a 66% chance of a 25bps hike later this month, while the 20yr JGB yield rose to its highest since June 1999, and the 30yr JGB yield was at a record high. Some of the moves were then later pared with support seen in JGBs after a 30yr auction, although this was only brief, and JGBs then resumed their downward trend.

COMMODITIES

- Crude futures were kept afloat, although the upside was capped following yesterday's choppy performance as remarks from US and Russian officials regarding their recent meeting were positive but suggested a lack of solid breakthrough, while US envoys are set to meet with Ukrainian representatives later today.

- Spot gold initially eked out mild gains with early support seen around the USD 4,200/oz level, but then faded the gains with price action rangebound after the prior day's indecisive performance and as the dollar got some respite from the recent selling.

- Copper futures added on to yesterday's spoils, which were facilitated by the constructive mood stateside, while Shanghai's most active copper contract climbed to a record high.

CRYPTO

- Bitcoin took a breather following its recent rebound and was stalled by resistance at the USD 94,000 level.

NOTABLE ASIA-PAC HEADLINES

- Chinese President Xi said in a meeting with French President Macron that China and France are far-sighted, responsible and independent major countries, while he added that China and France should uphold multilateralism and that China is willing to eliminate interferences and stick to equal dialogues with France. Xi also commented that both countries should support each other on core interests and agreed to expand practical cooperation, as well as consolidate cooperation on airspace and nuclear energy. Furthermore, he said both countries aim to expand two-way investment and that China will expand domestic demand in the 15th five-year plan and will also expand market access and opening-up.

- PBoC Governor Pan said in a People's Daily op-ed that China must maintain prudent monetary policy and should avoid excessive policy adjustments, while he also suggested preventing overreach from leading to long-term side effects of policies.

- BoJ Governor Ueda reiterated that they can only estimate the neutral rate with a wide range thus far, while he added they cannot specify a terminal rate and are working on narrowing the estimate on the neutral interest rate with the findings to be disclosed if successful. Furthermore, he said for now, they have to work with the current estimate set in a fairly wide range and there is uncertainty on how far interest rates can eventually be raised.

- BoJ is likely to raise interest rates in December, a decision Japan's government will likely tolerate, according to sources cited by Reuters.

DATA RECAP

- Australian Balance on Goods (Oct) 4.4B vs. Exp. 4.2B (Prev. 3.9B)

- Australian Goods/Services Exports (Oct) 3.4% (Prev. 7.9%)

- Australian Goods/Services Imports (Oct) 2.0% (Prev. 1.1%)

- Australian Household Spending MM (Oct) 1.3% vs Exp. 0.6% (Prev. 0.2%, Rev. 0.3%)

- Australian Household Spending YY (Oct) 5.6% vs Exp. 4.6% (Prev. 5.1%)

GEOPOLITICS

MIDDLE EAST

- Israeli PM's office said Lebanon's ceasefire monitoring committee meeting saw agreement on formulating ideas to promote economic cooperation between Lebanon and Israel. Israel said it clarified that Hezbollah disarmament is obligatory, with no connection to promoting cooperation on economic issues, while parties agreed on holding a follow-up discussion.

- Israel identified the body of the hostage received from Gaza as Thai national Sontisek Rintalk and said the body of the last Israeli hostage, Ran Gvili, remains in Gaza.

RUSSIA-UKRAINE

- US President Trump said the meeting between Russian President Putin, Special Envoy Witkoff and Kushner was a reasonably good meeting and "we'll see what happens", while he added that Russian President Putin wants to end the war.

- White House official said the US and Russia had a thorough and productive meeting, while Witkoff and Kusher briefed Trump after the meeting with Putin on Tuesday and are to meet Ukrainian representatives in Miami on Thursday.

OTHER

- Venezuela's President Maduro said he had a conversation with US President Trump about 10 days ago, while he added that steps are being taken towards a respectful dialogue between both countries.

EU/UK

NOTABLE HEADLINES

- Spain's Economy Minister said they will only use about 25% of loans available from EU recovery funds, and that Spain has not seen any significant impact at a macro level from US tariffs, while Spain is confident that the EU-Mercosur trade deal can be signed by year-end.