US Market Open: US equity futures lag European bourses; Yen outperforms following BoJ sources

04 Dec 2025, 11:29 by Newsquawk Desk

- European equities opened higher, reflecting positive APAC momentum, though European news flow has been light.

- Central bank updates included hawkish BoJ sources alongside concerns about Hassett as Fed Chair.

- The BoJ is likely to raise interest rates in December in a government-approved move, according to Reuters and Bloomberg sources.

- DXY is trading near the lower end of its 98.798–99.029 intraday range, pressured by JPY strength

- Fixed income benchmarks are lower following the hawkish BoJ reports, though the associated softening in risk sentiment has provided a modest haven bid as the morning unfolded.

- Looking ahead, highlights include US Challenger Layoffs (Nov), Jobless Claims (w/e 29 Nov), Revelio Public Labor Statistics, Chicago Fed Labour Market Indicators (Final), Durable Goods (Sep), Factory Orders (Sep), Atlanta Fed GDP. Speakers include BoE’s Mann, ECB’s Lane, Cipollone & de Guindos, Fed’s Bowman. Earnings from Kroger & Dollar General.

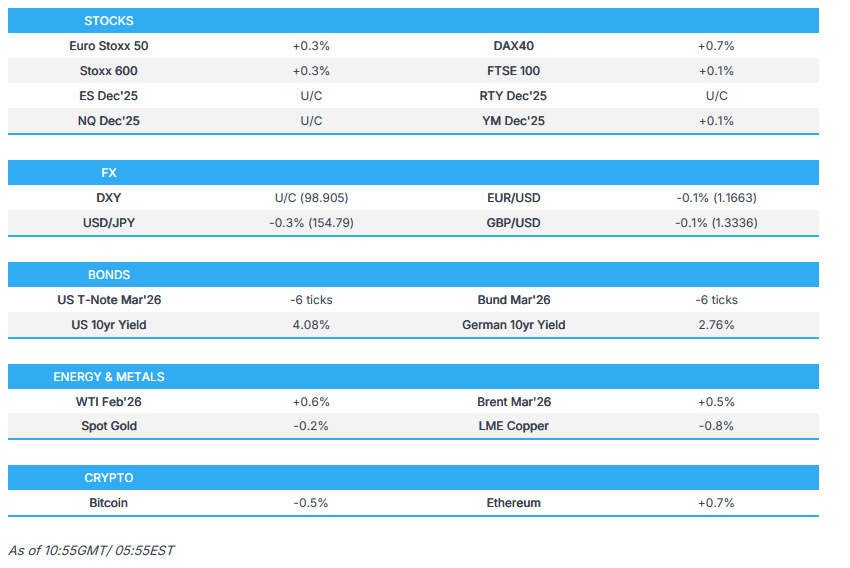

SNAPSHOT

TARIFFS/TRADE

- US President Trump said they will either let the USMCA expire or maybe work out another deal with Mexico and Canada.

- US halted plans to sanction the Chinese spy agency to maintain the trade truce, and the Trump administration will also not enact any major new export controls against China, while the Trump admin is preparing to hold a high-level meeting to decide whether to provide licenses to allow NVIDIA (NVDA) to export the H200 to China, according to FT.

- Chinese Commerce Ministry, on rare earth export controls, said as long are export license applications are for civilian use, they will be approved.

- Chinese President Xi said in a meeting with French President Macron that China and France are far-sighted, responsible and independent major countries, while he added that China and France should uphold multilateralism and that China is willing to eliminate interferences and stick to equal dialogues with France. Xi also commented that both countries should support each other on core interests and agreed to expand practical cooperation, as well as consolidate cooperation on airspace and nuclear energy. Furthermore, he said both countries aim to expand two-way investment and that China will expand domestic demand in the 15th five-year plan and will also expand market access and opening-up.

- India's Trade Minister said exports of autos, electronic goods, textiles and machinery to Russia are expected to increase. India also aims to expand and diversify exports to Russia to address the trade imbalances. India has secured a USD 2bln submarine deal, Bloomberg reported during the visit of Russian President Putin.

NOTABLE US HEADLINES

- US President Trump's aides and allies were reportedly discussing the possibility of Treasury Secretary Bessent also leading the National Economic Council, according to Bloomberg.

- US President Trump's administration ordered an enhanced vetting of H-1B visa applicants, with new H-1B visa screening based on any involvement in censorship or free speech, according to the State Department memo.

- The EU investigation into Meta's (META) use of AI in WhatsApp could come on Thursday, according to Reuters sources.

- Palantir (PLTR) launched a chain reaction to build AI infrastructure in the US, with founding partners including CenterPoint Energy (CNP) and NVIDIA (NVDA).

BOJ

- BoJ is likely to raise interest rates in December, a decision Japan's government will likely tolerate, according to sources cited by Reuters.

- Key members of Japanese PM Takaichi's government would not try to prevent a BoJ hike in December, Bloomberg reports, citing sources.

- BoJ is carrying out an assessment of the level of neutral interest rate, according to Jiji.

- BoJ Governor Ueda reiterated that they can only estimate the neutral rate with a wide range thus far, while he added they cannot specify a terminal rate and are working on narrowing the estimate on the neutral interest rate, with the findings to be disclosed if successful. Furthermore, he said for now, they have to work with the current estimate set in a fairly wide range, and there is uncertainty on how far interest rates can eventually be raised.

EUROPEAN TRADE

EQUITIES

- European equities opened higher, reflecting positive APAC momentum, though morning news flow has been light. Markets expect Kevin Hassett to be named the next Fed Chair, with some concerns that he could be influenced by President Trump on rates. Meanwhile, Reuters and Bloomberg reported hawkish signals suggesting the BoJ is likely to raise rates in December with government approval.

- Sectors are mixed with a positive tilt: Autos, Industrial Goods & Services and Technology lead. At the bottom: Utilities, Basic Resources and Health Care.

- US equity futures are marginally higher: ES (+0.1%), NQ (+0.1%), YM (+0.1%), while RTY is flat. Focus now shifts to US data—Initial Jobless Claims, Factory Orders, the Atlanta Fed GDP estimate—and comments from Fed’s Bowman.

- Click for the sessions European pre-market equity newsflow

- Click for the additional news

FX

- DXY is trading near the lower end of its 98.798–99.029 intraday range, pressured by JPY strength after Reuters and Bloomberg reported the BoJ is likely to hike rates in December with government approval. Money markets were already pricing a 66% chance of a hike following Governor Ueda’s recent hawkish remarks. USD/JPY slipped from 155.54 to a 154.77 low, with next support at the 1 December trough of 154.66.

- AUD is firmer amid continued hawkish repricing of RBA expectations.

- G10 FX is otherwise mostly flat and taking its cue from the USD, with few fresh drivers. EUR and GBP were little moved by Construction PMI releases.

- PBoC set USD/CNY mid-point at 7.0733 vs exp. 7.0554 (Prev. 7.0754)

- Chinese State-owned banks reportedly bought USD on the onshore spot market this week in a bid to rein in CNY strength, according to Reuters sources.

- RBI to tolerate a weaker rupee as dollar inflows diminish, according to Reuters sources.

- Click for NY OpEx Details

FIXED INCOME

- Fixed income benchmarks are lower following the hawkish BoJ reports, though the associated softening in risk sentiment has provided a modest haven bid as the morning has unfolded.

- JGBs underperformed, falling as much as 42 ticks to a new contract low of 134.08. The move pushed the 20yr yield to its highest since June 1999 and the 30yr yield to a record high, with selling driven by reports that boosted December BoJ hike odds to above 65%.

- The bearish tone extended into USTs and Bunds (now trading the Mar’25 contract), which hit lows of 112-27 and 128.46, down eight and 16 ticks respectively. European newsflow was limited; French and Spanish supply saw no major reaction, with Spain’s auction strong and France’s slightly softer versus prior.

- For USTs, focus beyond the BoJ remains on the Fed Chair narrative. The FT noted bond investors have expressed concern to the Treasury over Hassett’s potential appointment due to his perceived alignment with the President. Kalshi odds for Hassett have slipped to ~75% from above 80% earlier in the week.

- Spain sells EUR 2.88bln vs exp. EUR 2.5-3.5bln 2.70% 2030, 0.85% 2037 Bono and EUR 0.481mln vs exp. EUR 0.25-0.75bln 1.15% 2036 I/L.

- France sells EUR 5.06bln vs exp. EUR 3.5-5.5bln 4.75% 2035, 0.50% 2040, 4.50% 2041, 3.25% 2055 OAT.

- UK sells GBP 1bln 4.25% 2039 Gilt via tender: b/c 3.88x, average yield 4.813%.

COMMODITIES

- Crude benchmarks were firmer through the APAC session despite constructive comments from US and Russian officials after their recent Moscow meeting. Both benchmarks climbed to highs of USD 59.42/bbl (WTI) and USD 63.08/bbl (Brent) before easing to USD 59.11/bbl and USD 62.74/bbl as risk sentiment softened following the hawkish BoJ reports.

- XAU posts modest gains early in APAC, reaching USD 4,217/oz before sliding to USD 4,176/oz and remaining below USD 4.2k/oz. Despite a recent soft ADP print and mixed services PMI, gold has unwound its data-driven uptick as broader risk sentiment improves.

- 3M LME copper traded within a USD 11.43k–11.53k/t range in APAC before retreating from Wednesday’s all-time high of USD 11.54k/t, now at session lows around USD 11.35k/t. The pullback follows Rio Tinto’s raised 2025 copper production guidance and Goldman Sachs’ scepticism over the recent rally.

NOTABLE DATA RECAP

- EZ Retail Sales YY (Oct) 1.5% vs. Exp. 1.3% (Prev. 1.0%, Rev. 1.2%)

- EZ Retail Sales MM (Oct) 0.0% (Prev. -0.1%)

- EZ HCOB Construction PMI (Nov) 45.4 (Prev. 44)

- German HCOB Construction PMI (Nov) 45.2 (Prev. 42.8)

- French HCOB Construction PMI (Nov) 43.6 (Prev. 39.8)

- Italian HCOB Construction PMI (Nov) 48.2 (Prev. 50.7)

- UK S&P Global PMI: Composite (Nov) 50.1 (Prev. 51.4)

- UK S&P Global Construction PMI (Nov) 39.4 (Prev. 44.1)

- Swiss Manufacturing PMI (Nov) 49.7 vs. Exp. 48.5 (Prev. 48.2)

- Swiss Unemployment Rate Adj (Nov) 3.0% vs. Exp. 3.0% (Prev. 3.0%)

- Swedish CPIF Excluding Energy Flash YY (Nov) 2.4% vs. Exp. 2.7% (Prev. 2.80%)

- Swedish CPIF Flash YY (Nov) 2.3% vs. Exp. 2.5% (Prev. 3.10%)

NOTABLE EUROPEAN HEADLINES

- BoE Decision Maker Panel Survey (Nov): Expectations for year-ahead CPI inflation remained unchanged at 3.4%; Expected year-ahead wage growth rose slightly, by 0.1ppt to 3.8% in the three months to November

GEOPOLITICS

MIDDLE EAST

- Israel identified the body of the hostage received from Gaza as Thai national Sontisek Rintalk and said the body of the last Israeli hostage, Ran Gvili, remains in Gaza.

- Iraq has decided to freeze the money of "terrorists", including Hezbollah and the Houthis, via the Official Gazette

RUSSIA-UKRAINE

- US President Trump said the meeting between Russian President Putin, Special Envoy Witkoff and Kushner was a reasonably good meeting and "we'll see what happens", while he added that Russian President Putin wants to end the war.

- White House official said the US and Russia had a thorough and productive meeting, while Witkoff and Kusher briefed Trump after the meeting with Putin on Tuesday and are to meet Ukrainian representatives in Miami on Thursday.

- Russian President Putin said the meeting with US' Witkoff and Kushner was necessary and very useful, but it is "too early to say"; said Russia will take control of Donbas and Novorossiya by military means or otherwise.

- Russian Foreign Ministry Spokesperson said the attacks on tankers in the Black Sea and CPC are aimed at disrupting the peace talks in Ukraine.

- A Ukrainian official has reportedly cautioned that Thursday's meeting between Ukraine's Umerov and US' Witkoff is a "debrief" by the US and not "a negotiating session...", FT reported.

OTHER

- Venezuela's President Maduro said he had a conversation with US President Trump about 10 days ago, while he added that steps are being taken towards a respectful dialogue between both countries.

- China is said to be gathering military ships across East Asia in a show of maritime force, according to Reuters sources

CRYPTO

- Bitcoin resides in a narrow range under USD 94,000, whilst Ethereum trades on either side of USD 3,200.

APAC TRADE

- APAC stocks were mostly higher following the positive momentum from Wall St, where all major indices rose amid a weaker dollar and softer yield environment, but with some of the gains in the region capped amid a quiet calendar and lack of major fresh macro catalysts.

- ASX 200 edged higher in rangebound trade with strength in materials and resources offsetting the losses in the real estate and consumer sectors, while the mining industry was among the outperformers aside from the gold-related stocks.

- Nikkei 225 rallied above the 50k level as the tech-related momentum in Japan continued, despite higher yields and bets for a December BoJ rate hike.

- Hang Seng and Shanghai Comp were mixed amid weakness in auto names and after another liquidity drain by the PBoC, while PBoC Governor Pan noted in an Op-Ed that China must maintain prudent monetary policy and should avoid excessive policy adjustments.

NOTABLE ASIA-PAC HEADLINES

- PBoC Governor Pan said in a People's Daily op-ed that China must maintain prudent monetary policy and should avoid excessive policy adjustments, while he also suggested preventing overreach from leading to long-term side effects of policies.

DATA RECAP

- Australian Balance on Goods (Oct) 4.4B vs. Exp. 4.2B (Prev. 3.9B)

- Australian Goods/Services Exports (Oct) 3.4% (Prev. 7.9%)

- Australian Goods/Services Imports (Oct) 2.0% (Prev. 1.1%)

- Australian Household Spending MM (Oct) 1.3% vs Exp. 0.6% (Prev. 0.2%, Rev. 0.3%)

- Australian Household Spending YY (Oct) 5.6% vs Exp. 4.6% (Prev. 5.1%)

GLOBAL

- Hapag Lloyd (HLAG GY) CEO said global shipping demand could increase by 15-20% by 2030.