US Market Open: NQ outperforms following Palantir earnings; Precious metals rebound with gold nearing USD 5k/oz

03 Feb 2026, 11:27 by Newsquawk Desk

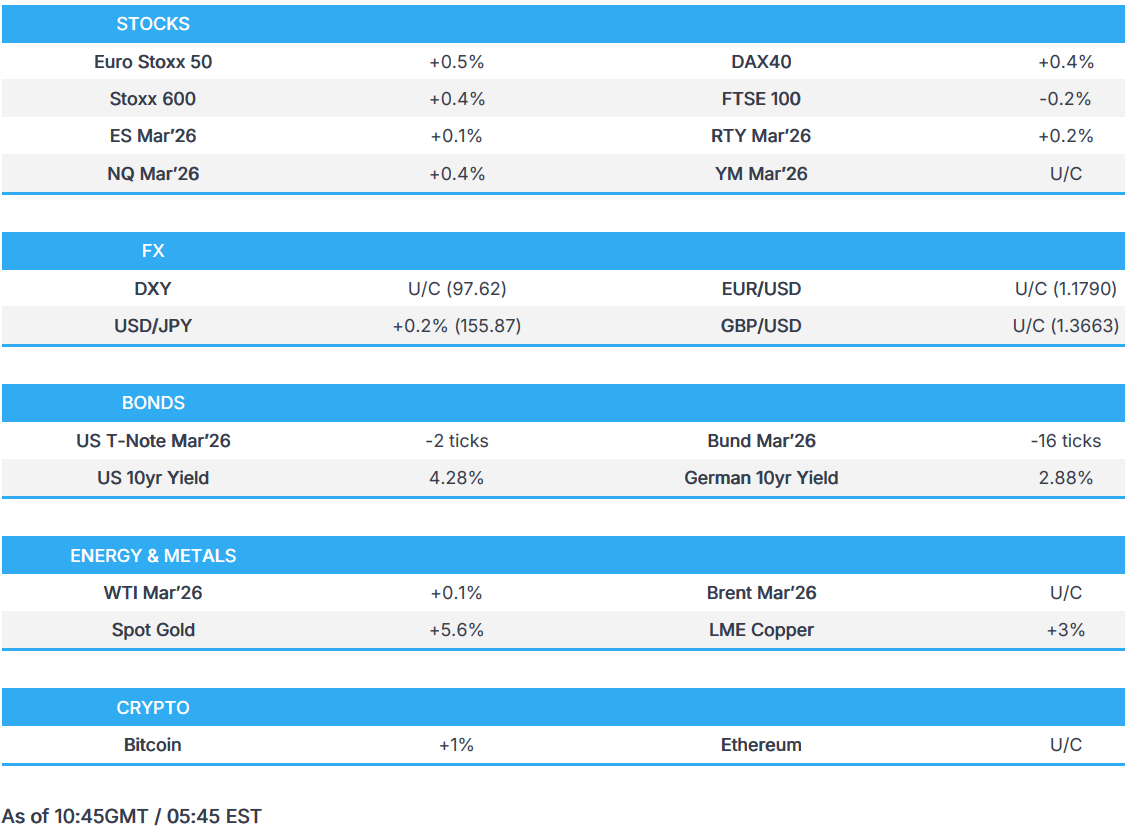

- European bourses opened stronger, but sentiment has dipped off best levels; US equity futures are modestly firmer, with mild outperformance is seen in the NQ.

- DXY is flat, Antipodeans benefit from a rebound in metals prices with outperformance in the Aussie after the RBA hiked rates by 25bps (as expected), whilst the SoMP noted that underlying inflation is higher than expected.

- Fixed income on the backfoot with supply in focus in a shutdown-thinned US docket.

- Crude prices initially lower but now flat; India to stop importing Russian oil as part of the trade deal with the US. Metals rebound with spot gold returning above USD 4900/oz.

- Looking ahead, highlights include US RCM/TIPP (Feb), New Zealand Unemployment (Q4), Australian S&P PMIs Final (Jan), Speakers including Fed’s Bowman, Barkin & ECB's Lagarde.

- December JOLTS has been postponed, on account of the US government shutdown.

- Earnings from AMD, Supermicro, Amgen, Amcor, PayPal, PepsiCo, Pfizer, Merck.

EQUITIES

- European bourses (+0.4%) opened entirely in the green, but sentiment has since waned a touch off best levels, with a couple of indices now slightly in the red.

- European sectors opened with a positive bias but are now mixed. Basic Resources outperform, led higher by strength in underlying metals prices. Media lags, pressured by losses in Publicis (-7.4%) and ProSiebenSat.1 Media (-2.2%) post-earnings.

- US equity futures (ES +0.2% NQ +0.5% RTY +0.2%) are modestly firmer across the board, with slight outperformance in the tech-heavy NQ, as Palantir (+10%) rises pre-market after strong Q4 metrics. Moreover for the tech sector, overnight the likes of Samsung Electronics (+7%) and SK Hynix (+9.2%) rebounded following recent losses.

- NXP Semiconductors NV (NXPI) Q4 2025 (USD): Adj. EPS 3.35 (exp. 3.31), Revenue 3.34bln (exp. 3.31bln). Q1 Guidance:. EPS 2.77-3.17 (exp. 2.99). Revenue 3.05-3.15bln (exp. 3.09bln).

- OpenAI has determined it needs alternatives to NVIDIA’s (NVDA) latest AI chips in some cases, has sought alternatives since last year. OpenAI is unsatisfied with the speed at which NVIDIA’s hardware can spit out answers to ChatGPT users for complex problems.

- Palantir Technologies Inc. (PLTR) Q4 2025 (USD): Adj. EPS 0.25 EPS (exp. 0.23), Revenue 1.41bln (exp. 1.34bln). Said sales to US businesses in 2026 are expected to grow at least 115% to more than USD 3.14bln.Outlook:. FY revenue 7.182-7.198bln (exp. 6.3bln). FY adj. operating income 4.126-4.142bln (exp. 3.14bln). Q1 adj. operating income 870-874mln (exp. 641mln). Q1 revenue 1.532-1.536bln (exp. 1.33bln).

- Click for the sessions European pre-market equity newsflow

- Click for the additional news

FX

- DXY resumed trade overnight on a softer footing following yesterday's post-ISM recovery (which printed its first expansion in 12 months and at the fastest pace since 2022). The index gradually pared those losses as the morning progressed, to now trade flat, and at the upper end of a 97.34-97.62 range. On the data front, it was also announced that the BLS has delayed the December JOLTS report due today and the January NFP report that was scheduled for Friday owing to the partial government shutdown. With a House vote expected as early as today, the data could be published next week if the vote passes, ING posits.

- Antipodeans are firmer with outperformance in the AUD amid the rebound in risk appetite and metal prices, while further upside was seen after the RBA meeting, where the central bank hiked the Cash Rate by 25bps to 3.85%, as expected, and stated inflation is likely to remain above target for some time. Governor Bullock declined to provide any forward guidance on the future path of interest rates. AUD/USD has come off best levels amid the aforementioned recovery in the DXY but still holds onto most of its gains in a 0.6945-0.7050 current daily range.

- Other G10s are flat/lower against the USD, with EUR & GBP flat whilst the JPY lags a touch. For the latter, there was some commentary via Japanese Finance Minister Katayama who reiterated that PM’s Takaichi latest commentary on a weak JPY was a general fact and didn't specifically emphasise merits in a weak JPY. Focus now on the Japanese snap election, where discussions regarding an LDP "supermajority" is getting more attention. Elsewhere, EUR digested a cooler-than-expected prelim French HICP report which had little impact on the single currency.

- Click for NY OpEx Details

FIXED INCOME

- JGBs spent the overnight session under modest pressure, with losses of just under 15 ticks at most in a narrow 131.41-60 band. Specifics for Japan are a little light as markets count down to Sunday's election, and the narrative is increasingly pointing to a convincing LDP victory, with a 'super majority' featuring more in discussions around the potential outcome.

- USTs are under modest pressure after contained APAC trade. Pressure that is most pronounced at the short end, with yields bid across the curve and flattening as things stand, in a marginal extension on the post-ISM flattener. Today's docket has been trimmed by the US shutdown, as the BLS will not be updating until there is a resolution and as such, JOLTS will not print. While a funding deal should pass very shortly, Friday's NFP will also be pushed until at least next week. Currently, USTs trade at the low-end of 111-15 to 111-20+ parameters, at a WTD low, taking out last week's trough by half a tick but clear of the 111-09 YTD base.

- Bunds came under pressure early doors, directionally in-fitting with the above, but with magnitudes a little more pronounced in limited newsflow and light volumes. A move that was perhaps a function of the constructive European risk tone at the time. Bunds as low as 127.74 at the time and currently hold a handful of ticks above that trough with losses of c. 15 ticks on the session. Data-wise, French prelim. HICP came in cooler-than-expected across the board, lifting EGBs generally at the time. A series that works to offset some of the hawkish impulses from the prelim. Thereafter, a 2035 Green Bund auction had little impact on the benchmark.

- Gilts gapped lower by 12 ticks, acknowledging the above. UK specifics are very light aside from a well received 2035 auction, which garnered a b/c above the 3x mark. Focus now turns to the BoE on Thursday, where rates are expected to be kept unchanged.

- UK sold GBP 4.25bln 4.75% 2035 Gilt: b/c 3.63x (prev. 3.26x), average yield 4.585% (prev. 4.456%), tail 0.2bps (prev. 0.3bps).

- Germany sells EUR 1.35bln vs exp. EUR 1.5bln 2.50% 2035 Green Bund: b/c 2.01x (prev. 2.2x), average yield 2.79% (prev. 2.52%), retention 10.0% (prev. 4.2%)

- Ireland's NTMA raises EUR 5bln from the sale of its new 10 year benchmark bond.

- South Korea is to sell 3-year and 5-year USD-denominated bonds.

- Italy's Tesoro opens book to sell new 15-year BTP bond via syndication, with guidance seen +10bps to 2040 BTP.

- Japan sold JPY 1.99tln 10yr JGBs, b/c 3.20x (prev. 3.30x), average yield 2.249% (prev. 2.095%). Lowest accepted price 98.74 vs prev. 99.99. Average accepted price 98.79 vs prev. 100.04. Tail in price 0.05 vs prev. 0.05.

COMMODITIES

- Crude benchmarks continued to extend on Monday's losses, with WTI and Brent nearing USD 61/bbl and USD 65/bbl, respectively. Oil prices traded muted throughout the APAC session but were pressured following comments by Russia's Deputy PM Novak, saying they have a surplus in fuel supplies. Since, benchmarks have edged a little higher to now trade flat on the session.

- Nat Gas futures continue to fall, with Dutch TTF returning to EUR 32/MWh as concerns over the Arctic storm affecting gas production ease.

- Precious metals have brushed off the recent tarnish following the aggressive selloff in recent sessions. Spot gold has regained the USD 4900/oz handle as being as low as USD 4400/oz in Monday's session. Investors have been highlighting that the selloff is just a correction and that underlying drivers for gold, mainly central bank buying and ETF inflows, remain strong.

- 3M LME Copper continues to rebound, alongside precious metals, as the red metal extends to a session high of USD 13.48k/t. The bounce from the recent selloff comes amid a broader reversal of the risk tone and reports that China could expand its strategic copper reserves. China maintains stockpiles of major base metals such as copper and cobalt to stabilise commodity prices and ease raw material cost pressures. The expansion of the reserves comes amid the recent volatility of metals prices.

- Russian Deputy PM Novak said oil demand and supply are in balance.

- Kuwait Petroleum Corp. intends to invite global oil firms to assist Kuwait Oil in the development of offshore fields, Bloomberg reported.

- China raises its gas and diesel prices by CNY 205 and 195 respectively, effective February 4th.

- Russia's Deputy PM Novak said they have a surplus in fuel supplies, adding that domestic diesel and gas supplies are sufficient.

- Shanghai Gold Exchange to adjust margin rations to 17% (prev. 16%) for some gold and silver contracts, and widen the daily price limit to 16% (prev. 15%) as of the 4th February settlement.

- China could expand its strategic copper reserves and explore a commercial reserve system with state-owned firms.

TRADE/TARIFFS

- Kremlin's Spokesperson said Russia have not heard any statement from India about halting Russian oil purchases, adding that they intend to continue developing their relations with India.

NOTABLE EUROPEAN HEADLINES

- French Finance Minister said the G7 needs to agree on a joint instrument to address global macroeconomic imbalances. Joint instruments can have a sectoral focus, such as rare earths.

- French Finance Minister Lescure said that the 2026 budget will reduce the deficit to 5.0% from 5.4%, GDP growth of 1% so far in 2026 is a good start.

NOTABLE EUROPEAN DATA RECAP

- UK Grocery Inflation +4.0% Y/Y, Sales +3.8% Y/Y in the 4 weeks to January 25, via Worldpanel.

- French HICP Jan: 0.4% Y/Y (exp. 0.6%, prev. 0.7%); -0.4% M/M (exp. -0.2%, prev. 0.1%).

- French Inflation Rate MoM Prel (Jan) M/M -0.3% vs. Exp. -0.1% (Prev. 0.1%).

- French Inflation Rate YoY Prel (Jan) Y/Y 0.3% vs. Exp. 0.6% (Prev. 0.8%).

- French Budget Balance (Dec) -124.7B (Prev. -155.4B, Rev. From -155.4B).

CENTRAL BANKS

- RBA hikes the Cash Rate by 25bps to 3.85%, as expected, with the decision unanimous, while it stated that inflation is likely to remain above target for some time. A wide range of data confirms inflation has picked up materially. Broad measures of wage growth continue to be strong. Uncertainty in the global economy remains significant but has so far not affected Australia. Job market conditions are a little tight. Capacity pressures are greater than previously assessed. Private-sector demand is growing faster than expected. There are uncertainties about the outlook for domestic economic activity and inflation and the extent to which monetary policy is restrictive. Quarterly Statement on Monetary Policy:. Underlying inflation is higher than expected. Underlying inflation rose to 3.4% over the year to the December quarter, which was higher than expected three months ago and substantially higher than expected in the August Statement. GDP growth has continued to pick up, with private demand growth surprisingly strong. GDP grew by 2.1% over the year to the September quarter, which was around our estimate of the economy’s potential growth rate. Labour market conditions have been stable. The unemployment rate has been broadly stable at around 4.25% in recent quarters.

- RBA Governor Bullock said does not know if this will be a tightening cycle and cannot rule anything out or in.

- RBA Governor Bullock said pulse of inflation is too strong and that high inflation hurts all Australians. said:. Board thinks inflation will take longer to return to the target. We cannot allow inflation to get away from us. Will not give forward guidance and the board will remain focused on data. Did not discuss a 50bps rate increase.

- US President Trump said Fed chair nominee will do good and that investigation into Fed Chair Powell should be taken to the end.

- ECB Bank Lending Survey (Q4) : Overall credit terms and conditions tightened for loans to firms and consumer credit, while they eased for housing loans.

- BOK Minutes suggests one board member said further rate cuts should only be considered after risks related to FX and housing markets ease.

- ECB Bank Lending Survey (Jan): Banks tightened credit standards for firms, citing higher perceived risks amid lower risk tolerance; Credit standards eased slightly for housing loans, but tightened further for consumer credit.

NOTABLE US HEADLINES

- US President Trump said he is seeking USD 1bln of damages from Harvard.

- US House Rules panel advances the Senate funding package.

- US President Trump said announcing the creation of US strategic critical minerals reserve. We are launching Project Vault today. USD 2bln from the private sector. USD 10bln funding from US Exim Bank.

GEOPOLITICS

RUSSIA-UKRAINE

- Russian Deputy PM Novak said oil demand and supply are in balance.

- Kremlin's Spokesperson said Russia have not heard any statement from India about halting Russian oil purchases, adding that they intend to continue developing their relations with India.

- Russia's Deputy Foreign Minister Ryabkov said the modernisation of their nuclear triad is at a very advanced stage.

- Russia's Deputy PM Novak said they have a surplus in fuel supplies, adding that domestic diesel and gas supplies are sufficient.

- Russia and China held new round of stability talks to support multilateralism.

- Ukraine agrees multi-tier plan for enforcing any ceasefire with Russia, according to FT.

- reported note that witnesses say loud explosions heard in Ukraine's capital of Kyiv.

- US President Trump said doing very well with Ukraine and Russia and think we'll have some good news. said:. Putin agreed to no missiles going into Kyiv. We are talking with Iran and we'll see how that goes.

MIDDLE EAST

- Iran's Vice President said a new chapter of Iran's nuclear achievements will be unveiled.

- Iranian official said that a US aircraft carrier has retreated and is now near Yemen.

OTHERS

- Russia and China held new round of stability talks to support multilateralism.

- Venezuela's Interim President Rodriguez met with US Envoy Loro Dogu.

CRYPTO

- Bitcoin is a little firmer and trades around USD 78k; Ethereum is flat and holds around USD 2.2k.

APAC TRADE

- APAC stocks were mostly higher with several bourses firmly recovering from the prior day's sell-off, as the region took impetus from the positive handover from Wall Street, where markets rallied after a strong ISM Manufacturing report.

- ASX 200 climbed higher with tech and miners leading the advances, although further upside was capped as the focus turned to the RBA which hiked rates for the first time in over two years and sounded hawkish on inflation.

- Nikkei 225 surged following recent currency weakness and gained a firm footing above 54,000 to hit a record intraday high.

- KOSPI outperformed in a turnaround from the prior day's bloodbath with the Korea Exchange activating a sidecar earlier in the session to briefly halt program trading after a sharp rise in the local benchmark.

- Hang Seng and Shanghai Comp initially lagged with early pressure seen across tech stocks, despite no immediate obvious catalysts, and with some attributing it to VAT hike concerns, while the Hang Seng TECH Index briefly re-entered bear market territory after dropping more than 20% from its October high. However, Chinese markets then pared their losses alongside the broad rally in Asia.

NOTABLE ASIA-PAC HEADLINES

- China's No1/central document includes plans to improve and consolidate soybean production. Intend to stabilise food and oil output. To diversify agricultural product imports.

- Earthquake of magnitude 5.0 hits near the east coast of Honshu, Japan.

- Japanese Finance Minister Katayama continues to refrain from commenting on intervention data and said PM Takaichi talked about FX benefits as a general fact, and didn't specifically emphasise merits in a weak yen.

- Nintendo (7974 JT) President said memory price rises not having a major impact on earnings.

- Nintendo (7974 JT) - Q3 (JPY): Operating income 155.21bln (exp. 180.7bln), 9M switch sales -66% Y/Y; sees FY net sales 2.25tln (exp. 2.37tln).

NOTABLE APAC DATA RECAP

- Korea (Republic of) 30-Year KTB Auction 3.565% (Prev. 3.250%).

- Australian Building Permits MoM Prel (Dec) M/M -14.9% vs. Exp. -5.7% (Prev. 15.2%, Low. -9%, High. 0.5%).

- Australian Private House Approvals MoM Prel (Dec) M/M 0.4% (Prev. 1.3%).

- Australian Building Permits YoY Prel (Dec) Y/Y 0.4% (Prev. 20.2%).

- Japanese Monetary Base YoY Y/Y -9.5% (Prev. -9.8%).

- New Zealand Building Permits MoM (Dec) M/M -4.6% (Prev. 2.7%, Rev. From 2.8%).